A Comprehensive Farm-to-Fork Analysis Across All GLOBAL PROTEIN INDUSTRY 2026 Sectors

ESSFeed Intelligence Report

Poultry • Beef & Red Meat • Pork • Dairy • Seafood & Aquaculture • Plant-Based • Cultivated Meat • Precision Fermentation

Executive Summary

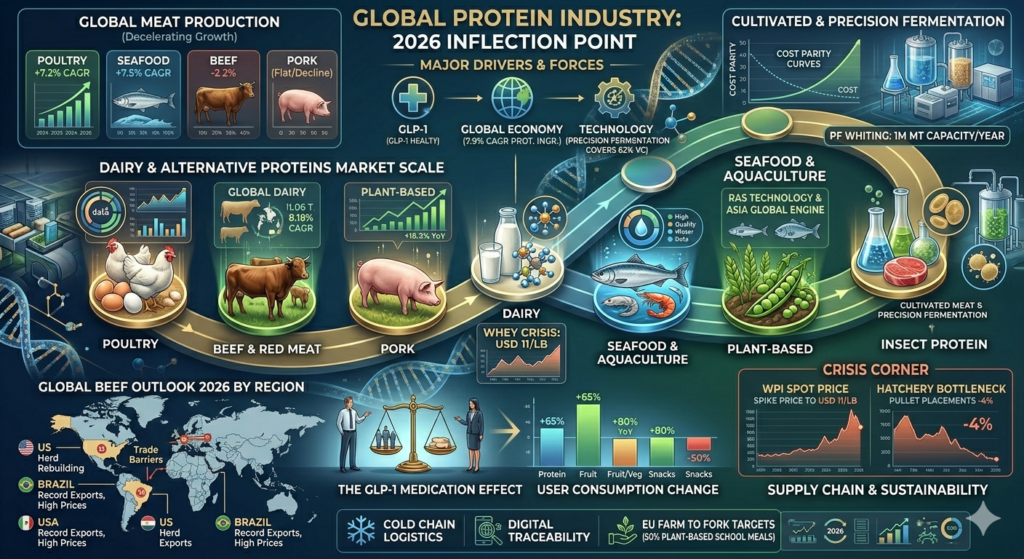

The global protein industry stands at an unprecedented inflection point in 2026. Three forces — a pharmaceutical revolution driven by GLP-1 weight-loss medications, a structural supply crisis in whey protein, and a fundamental shift in what consumers expect protein to do for them — are converging simultaneously, reshaping a sector worth well over USD 133 billion. This report delivers a comprehensive farm-to-fork analysis of every major protein category, from conventional livestock and dairy to the frontier technologies of precision fermentation and cultivated meat.

Global animal protein production growth is decelerating in 2026. Seafood and poultry will lead growth, while pork and beef production will contract. Meanwhile, the plant-based sector is recalibrating after years of over-hyped expectations, and precision fermentation is rapidly moving from laboratory curiosity to investable commercial platform. Across all segments, sustainability pressure, geopolitical trade disruption, technological integration, and demographic shifts in Asia are rewriting the rules of competition.

Key 2026 Market Figures at a Glance:

| Segment | 2026 Value | Growth Trajectory |

|---|---|---|

| Global Protein Ingredients Market | USD 56.7 billion | → USD 112.9B by 2035 (7.9% CAGR) |

| Global Dairy Foods Market | USD 1.06 trillion | → USD 1.99T by 2034 (8.18% CAGR) |

| Global Seafood Market | USD 406 billion | → USD 724B by 2034 (7.5% CAGR) |

| Plant-Based Protein Market | USD 75.78 billion | 18.3% YoY growth |

| Global Aquaculture Market | USD 344.97 billion | → USD 626B by 2035 (6.85% CAGR) |

| US Adults on GLP-1 Drugs | 12.4% | Projected 30M+ users by 2030 |

| Whey Protein Isolate Spot Price | USD 11/lb | Record high — processing crisis |

| Global Beef Production Change | -2.2% | First decline in six years |

Table of Contents

1. The Global Protein Landscape in 2026

1.1 Market Drivers and Structural Forces

Protein dominates consumer wellness trends in 2026 and is in high demand worldwide. It symbolises wealth, with consumption rising alongside economic growth, especially animal protein, valued for its essential amino acid profile. Protein is an enduring wellness powerhouse, with 80% of consumers saying they pay attention to protein in their diet.

The global protein market size is expected to grow from USD 27.81 billion in 2025 to USD 28.32 billion in 2026, with key drivers including the 2024 FDA GRAS status for precision-fermentation whey, the rising popularity of plant-based diets among Asia’s burgeoning middle class, and a strategic reformulation in aquafeeds replacing traditional fishmeal with insect and algae proteins.

The global protein ingredients market size was valued at USD 52.8 billion in 2025 and is expected to grow at a CAGR of 7.9% between 2026 and 2035, driven by increasing demand for plant-based alternatives. Archer Daniels Midland led with over 5.4% market share in 2025, with the top six players — including ADM, Cargill, Roquette Frères, Glanbia Nutritionals, and Kerry Group — collectively holding 18.1% market share.

Three forces that have never converged before are colliding simultaneously in 2026: a pharmaceutical revolution with GLP-1 medications now used by 12% of the US population, a once-in-a-generation supply crisis with WPI spot prices at USD 11/lb — levels never before recorded by USDA — and a fundamental rewiring of what consumers globally expect protein to do for them.

1.2 Macro Trade Environment

Geopolitical tension and trade policy are materially disrupting protein flows in 2026. In 2026, meat imports will decline significantly due to new trade barriers and weak domestic consumption. The US Department of Agriculture expects China’s beef purchases to decline to 3.5 million tons due to the implementation of safeguard measures, including quotas and high tariffs on imported products. Meanwhile, pork imports will decline to 1,100,000 tonnes under pressure from oversupply in the domestic market and anti-dumping duties imposed on meat from the European Union.

The EU-Mercosur free trade agreement took effect on May 1, 2026, reshaping long-term beef trade flows, though short-term impacts remain minimal. Beef production declined by 2.5% year-on-year in the first quarter of 2026 and is forecast to fall by 2.2% over the full year.

With global GDP growth projected to slow in 2026, consumers will remain price-sensitive and shift consumption patterns. Price dynamics within animal protein categories will vary, with price pressures leading some consumers to trade down within categories or switch between proteins.

1.3 The GLP-1 Effect on Protein Demand

No trend has more fundamentally altered the near-term trajectory of the food and protein industry than the mass adoption of GLP-1 receptor agonist medications. The number of Americans taking semaglutide or tirzepatide drugs for weight loss more than doubled in the past year and a half, with 12.4% of respondents taking the medications compared to 5.8% in February 2024.

GLP-1 drug use results in a measurable shift in users’ consumption behaviour. Respondents claimed their consumption of foods across different snack categories dropped by between 40% and 60%, while their consumption of specialty and health foods climbed by nearly 50%. Proteins increased even more, by 65%, and fruits and vegetables by nearly 80%.

By 2030, more than 30 million Americans could be on a GLP-1 treatment, up from 10 million in 2026, based on J.P. Morgan estimates. For restaurants and food and beverage companies, whether it is labelling as GLP-1 friendly, decreasing the serving size, emphasising protein content, or shifting to beverages, a number of players are starting to react.

Large manufacturers have already begun to adapt. Nestlé has launched ready-to-eat meals specifically targeted at people on GLP-1 drugs, while Danone and Coca-Cola are emphasising high-protein, low-sugar ranges in their portfolios. Nestlé has introduced its first new brand in nearly 30 years designed for GLP-1 consumers, and General Mills and Danone are marketing high-fibre, high-protein products explicitly around satiety and metabolic health.

2. The Poultry Sector: Growth Under Biological Pressure

2.1 Market Overview

Poultry remains the global animal protein growth leader in 2026. The global poultry market size is projected to grow from USD 521.95 billion in 2026 to USD 910.24 billion by 2034, at a CAGR of 7.20% during the forecast period. The expansion of frozen foods, ready-to-cook meals, and quick-service restaurant chains is driving demand for processed poultry, while technological advancements in cold chain logistics, automated processing lines, and packaging technologies are improving shelf life and product quality.

According to Rabobank, the US poultry industry is on track for another good year, driven by smaller beef supplies and favourable feed costs. Feed costs are helping to offset higher labour, chick and grower costs following a challenging Q4 2025 for margins. Though highly pathogenic avian influenza has been costly for the poultry industry, HPAI is less disruptive for broilers. Though bird weights are expected to stabilise in 2026, there is an industry-wide long-term shift toward heavier weight birds.

2.2 HPAI and Hatchery Constraints

The spectre of Highly Pathogenic Avian Influenza (HPAI) H5N1 continues to haunt global poultry supply chains. Between 2022 and 2024, the World Organisation for Animal Health (WOAH) reported that HPAI H5N1 caused an unprecedented global pandemic, leading to the death or culling of over 633 million poultry worldwide, with a peak of 146 million in 2022 alone.

The USDA’s February 2026 WASDE report revealed a notable downward revision for broiler production in the first half of the year, pointing to “recent production and hatchery data” showing that the expected expansion of the national flock has failed to materialise as quickly as analysts projected in late 2025. Pullet placements — the birds intended to produce future chicks — plummeted by 4% in the most recent counts, signalling a looming bottleneck in the production pipeline that could stifle supply well into the summer months.

The US poultry industry produced more than 9 billion broilers last year, which means 12 billion eggs were needed to meet capacity. It would require 15 billion eggs to hatch 9 billion viable broiler chicks if fertility rates continue to fall. “Fertility rates have been an issue, and avian influenza outbreaks are a threat that compounds the potential impact in a way that consumers would notice.”

2.3 Technology and Value Chain Integration

An important prediction for 2026 is that poultry will be increasingly managed as an integrated value chain, rather than as separate silos of hatchery, farm and processing plant. With antimicrobial resistance (AMR) and Avian Influenza a critical global challenge, poultry producers are under pressure to maintain strict biosecurity measures while reducing antibiotic use. Precision vaccination technologies offer a solution and will emerge as a cornerstone of flock health in 2026.

This new era of data-integrated poultry production — where sensor arrays in broiler houses transmit real-time welfare, mortality, and growth data to central management systems — is enabling dynamic feed formulation adjustments and early disease detection. The result is stronger, healthier flocks with fewer losses, improved welfare outcomes, and greater resilience across the supply chain.

3. Beef and Red Meat: The Tightest Cycle in Six Years

3.1 Global Production Decline

The global animal protein industry is set to experience a slowdown in production growth in 2026, according to RaboResearch. The decline will be driven by cyclical factors, like shifts in North American and Brazilian cattle markets, as well as structural factors, such as China’s efforts to rebalance its pork market. This marks the first reduction in global meat production in six years.

Global beef production will decline in 2026. Herd rebuilding in North America and Brazil, combined with structural adjustments in China, will tighten supply and keep prices firm across major markets. Beef cattle numbers in the US and Canada fell for six straight years in 2020–25, but stronger profitability is slowing liquidation and supporting herd rebuilding. US beef cow slaughter dropped by 19% on the year in 2025, with the culling rate projected at 8.5% for 2026, below the long-term average.

Brazilian beef production will likely fall by 5–6% in 2026 to 10.5 million tonnes because producers may retain cattle to rebuild herds. But exports will likely hit a record 4.4 million tonnes because of strong global demand, a weak Brazilian real and reduced competition from other suppliers, despite lower output. Domestic consumption will likely drop by up to 9% because high prices are pushing consumers toward cheaper proteins.

2026 Global Beef Outlook by Country:

| Country / Region | 2026 Outlook |

|---|---|

| United States | Herd rebuilding underway; feedlot inventory -3% YoY; imports to rise 6% on robust lean trimmings demand |

| Brazil | Production -5–6% to 10.5mn t; exports at record ~4.4mn t; weak BRL compensates for lower output |

| Australia | Production -1%; exports -0.9% to 2.2mn t; second-highest export total on record |

| China | Beef imports -13% on tariff safeguards; self-sufficiency pivot accelerating |

| Argentina | Production steady at 3.23mn t; exports at second-highest on record ~880,000t driven by China and US demand |

| European Union | Production -1% on high input costs and regulatory pressure; EU-Mercosur FTA reshaping long-term flows |

3.2 Sustainability Pressures and Greenwashing Scrutiny

New research released in 2026 finds that the majority of the sustainability claims and commitments made by meat and dairy companies can be considered greenwashing. The production of meat for human and animal consumption is responsible for 57% of total global food production emissions, while the global dairy sector alone contributes to 4% of global emissions. The world’s top five emitting companies — JBS, Marfrig, Tyson, Minerva, and Cargill — were responsible for an estimated 496 million tonnes of greenhouse gases in 2023.

This intensifying scrutiny is forcing a reckoning across major processors, who must now demonstrate credible, verified emissions reduction pathways rather than headline pledges. The US Roundtable for Sustainable Beef (USRSB) framework — built around six high-priority indicators covering GHG emissions, land use, water stewardship, and worker welfare — is providing the industry’s most rigorous voluntary standard. Traceability investments, including blockchain-enabled supply chain platforms, are accelerating, particularly among producers targeting EU and UK markets where supply chain due diligence requirements are becoming mandatory.

4. Pork: Navigating Disease, Oversupply, and Trade Friction

4.1 Global Supply Dynamics

Global pork production is navigating a complex intersection of disease pressure, overcapacity correction, and trade policy upheaval in 2026. China’s government direction to reduce the sow herd to rebalance supply and demand is expected to show towards the end of Q2 or early Q3. While a moderate decline in production is forecast in 2026, imports are expected to remain flat due to an efficient supply amid several trade frictions.

In Europe, RaboResearch expects EU pork production to top year-ago levels in the first half of the year, but contract in H2, driven by the ASF outbreak in Spain. In addition to the ongoing disease challenge, China’s anti-dumping tariffs are putting pressure on EU exports. Higher shipments to the Philippines, South Korea and the UK kept shipments stable in 2025.

4.2 North America and Trade

Canada forecasts a modest expansion in the Canadian sow herd, due to high costs and ongoing disease challenges. Pork exports continue to face competition from Brazil, while live hog exports to the US rebounded towards the end of 2025, due to sharply higher feeder pig exports rising 16.5% year-on-year. Southeast Asia: Vietnamese pork production is expected to drop in the first half of 2026 due to herd rebuilding, but likely to recover in the second half.

With official data through November available, shipments of pork have been 6% higher to the largest export market, Mexico. Strong feeder cattle prices have been a significant factor in prolonging the herd’s current decline. In 2025, feeder cattle prices for 750 to 800 pound calves averaged USD 322 per cwt, up from the 2024 average of USD 252.

5. Dairy: The Protein Pay Driver and the Whey Crisis

5.1 Market Scale and Growth

The global dairy foods market size was valued at USD 1,005.84 billion in 2025 and is projected to grow from USD 1,063.47 billion in 2026 to USD 1,995.47 billion by 2034, exhibiting a CAGR of 8.18% during the forecast period. Asia Pacific dominated the dairy foods market with a market share of 41.09% in 2025.

Two trends are moving to the forefront of dairy’s future: protein and AI. Companies’ investments in protein-led product innovation and manufacturing are positioning them well for both current and future growth. Sixty-four percent of executives at dairy processors express concern about the farming industry’s demographic trends and succession gaps, with the number of farmers declining faster than milk volumes — a signal of structural fragility beneath near-term production stability.

5.2 The Whey Supply Crisis

The processing bottleneck is the defining feature of 2026’s dairy landscape. Global dairy milk supply is stable. Cheese manufacturing — the process that generates liquid whey as a byproduct — continues at normal output. The crisis is entirely a processing infrastructure crisis: converting liquid whey into WPC and WPI powder requires specialised filtration and membrane equipment that took years to build and cannot be fast-tracked. The USD 11 billion in announced US capacity investment will not deliver meaningful relief before Q3 2027. US WPC and WPI volumes are largely forward-contracted into 2026, forcing global buyers to shift sourcing from the US to Europe, then to regional alternatives as availability tightens across markets.

5.3 Innovation and Consumer Trends

IFF’s Dairy Trends Report 2026 identifies five key trends that will drive market changes and product innovation, with “considered consumption” emerging as the dominant theme. “We’re witnessing the end of the ‘health versus happiness’ trade-off in the dairy aisle. The consumer’s desire for holistic well-being now extends beyond personal health to that of the planet.” As artificial intelligence becomes more integrated into product development, the dairy industry is navigating a delicate balance between technological efficiency and human authenticity.

US markets are currently facing a butterfat oversupply, driving milk prices down. While butterfat has been driving milk checks for many years, it is expected that protein will be the leading pay driver in 2026. Protein remains extremely valuable as the dairy proteins segment, such as ready-to-drink shakes, is quickly growing due to high consumer demand. Genomics will continue to drive protein gains as it remains the fastest and most reliable route to high components.

2026 Dairy Impact Assessment:

| Issue | Assessment |

|---|---|

| Butterfat Oversupply | US markets face oversupply, driving milk prices down; protein expected to become lead pay driver |

| Protein Premiumisation | RTD protein shakes, high-protein yogurt growing rapidly; protein pay component rising |

| Whey Processing Crisis | WPI at USD 11/lb record; USD 11bn US capacity investment will not deliver relief before Q3 2027 |

| AI Integration | Manufacturers deploying AI for nutritional profiling, supply chain optimisation, and demand forecasting |

| Farmer Demographics | Numbers declining faster than milk volumes; succession gaps creating long-term supply fragility |

| EU Milk Supply Pressure | Increased EU production applying downward price pressure on US dairy markets |

6. Seafood and Aquaculture: Asia Drives a Golden Decade

6.1 Market Overview

The global seafood market size was USD 386.99 billion in 2025 and is projected to grow from USD 406.10 billion in 2026 to USD 724.29 billion by 2034, at a CAGR of 7.50%. Asia Pacific dominated the seafood market with a market share of 44.17% in 2025.

Global per-capita seafood intake rose to 20.7 kilograms in 2022 as households in China, India, Vietnam, and Indonesia diversified diets toward affordable animal protein with a lighter carbon footprint. Feed manufacturers are reducing dependence on forage fish by incorporating insect meal, algae, and single-cell protein into feed formulations, thereby reducing the industry’s reliance on marine ecosystems. In 2024, the United States recorded a seafood trade deficit of USD 17 billion, prompting policymakers to promote aquaculture as a solution for food security.

The global aquaculture market is projected to grow from USD 344.97 billion in 2026 to USD 626.25 billion by 2035, at a CAGR of 6.85%. Recent advancements include AI-enabled feeding systems, IoT-based water monitoring, and recirculating aquaculture systems (RAS) that significantly reduce water usage and improve yield efficiency.

6.2 Technology in the Water

Smart aquaculture technologies are fundamentally transforming productivity and sustainability across the sector. Industry leaders such as Cermaq and Grieg Seafood are deploying AI-enabled feeding systems, real-time water quality monitoring, and precision harvesting to stabilise output and minimise environmental impact.

The aquaculture products market size is anticipated to grow from USD 227.0 billion in 2025 to USD 238.42 billion in 2026, forecast to reach USD 304.64 billion by 2031 at a 5.03% CAGR. Feed accounts for the largest spending because compound aquafeed innovation and insect protein inclusion are improving growth rates and lowering dependence on imported fishmeal.

6.3 Asia as the Global Growth Engine

An increased use of technology and AI in the value chain, a growing interest in health, nutrition and longevity, and Asia as a global growth engine are the trends predicted to shape the seafood industry throughout 2026. With the middle class projected to expand from 184 million in 2025 to more than 250 million by 2030, and current per-capita salmon consumption at only 100 grams, the market remains in an early stage with significant room for growth. Across Asia, social media platforms are changing how a new generation engages with seafood; the purchasing journey often starts on social media, with live commerce now a fully established channel.

In China, there are at least 20–25 licensed sashimi factories preparing fillet and packed salmon for ready-to-eat formats, with capacity expected to potentially double by end-2026.

7. Plant-Based Protein: Recalibration and Reinvention

7.1 Market Size and Growth

The plant-based protein market will grow from USD 64.07 billion in 2025 to USD 75.78 billion in 2026 at a CAGR of 18.3%. The growth in the historic period can be attributed to growing awareness of plant-based nutrition benefits, expansion of soy and pea protein usage, rising demand for meat substitutes, and increased availability of plant protein ingredients. Growth in the forecast period will be attributed to increasing demand for sustainable nutrition solutions, rising innovation in plant protein formulations, and expansion of personalised nutrition trends.

High production cost and price competitiveness remain the foremost challenge for the US plant-based proteins market. Despite growing consumer awareness, plant-based meat products are often priced 60–80% higher than conventional meat, making affordability a key restraint. Industry data from 2024 indicates that retail sales of plant-based meat declined by around 7% year-on-year, reaching approximately USD 1.2 billion.

7.2 Beyond Meat, Impossible Foods, and Strategic Pivots

In January 2026, Beyond Meat launched its Beyond Immerse plant-based protein beverage, signalling strategic diversification beyond meat alternatives into functional nutrition. In January 2026, Impossible Foods partnered with Equii to develop protein-enhanced plant-based meals. In May 2025, Danone acquired Kate Farms to strengthen its plant-based and specialised nutrition portfolio. In 2025, Nestlé expanded Garden Gourmet innovations, accelerating premium vegan food market growth globally.

In March 2026, Beyond Meat introduced a sparkling plant-based protein beverage called “Beyond Immerse.” The product uses pea-based protein and includes added fibre, vitamin C, and electrolytes, marking the company’s entry into the functional beverage segment.

7.3 Ingredient Innovation: Pea, Soy, and Emerging Sources

Canadian pea protein capacity expanded by 1 million metric tons in 2025–2026, with Roquette’s Manitoba facility now the anchor of North American plant-protein supply. European brands facing ESG procurement obligations are systematically replacing soy with traceable, European-grown pea protein — a sourcing shift that is structural, not trend-driven.

The European protein market size was valued at USD 6.22 billion in 2025 and estimated to grow from USD 6.52 billion in 2026 to reach USD 8.26 billion by 2031, at a CAGR of 4.85%. Growth reflects a decisive pivot away from imported soy toward domestically produced pulses, fermentation-derived ingredients, and insect biomass, a shift accelerated by Farm-to-Fork targets, Green Deal capital, and retailer carbon budgets. Raw-material volatility, notably the 23% surge in yellow-pea prices during the 2024 Canadian drought, is strengthening vertically integrated processors able to self-contract acreage.

The EU’s Farm to Fork strategy is pushing member states to source 50% of school-meal protein from plant or alternative sources by 2027.

8. Cultivated Meat: Regulatory Progress, Commercial Limitations

8.1 Regulatory Landscape

As of early 2026, five cultivated meat products have cleared the joint FDA-USDA regulatory pathway, covering chicken, salmon, pork fat, and poultry products. But clearing the regulatory hurdles has not translated into widespread availability. Cultivated meat remains largely absent from grocery stores, with most companies launching through limited restaurant partnerships to test consumer willingness to pay in real-world settings. The gap between regulatory clearance and commercial scale reflects the high production costs and limited bioreactor capacity that still constrain the industry.

By mid-2026, cultivated meat has received regulatory approval in Israel, the Netherlands, Switzerland, and Japan, with applications pending in the UK, Canada, and Australia. The industry is moving from proof-of-concept to genuine market entry, even if scale and price remain formidable obstacles.

8.2 State-Level Backlash

In 2026, Midwestern legislatures again introduced new bills to restrict, regulate or ban lab-grown or cell-cultured meats. South Dakota legislators placed a five-year prohibition on the sale, manufacturing and distribution of any cell-cultured protein. In December 2025, Ohio HB 10 was signed into law, establishing packaging and labelling requirements for cultivated-protein food products and prohibiting schools and institutions of higher education from purchasing cultivated-protein food products.

At least one company that received federal approval subsequently shut down operations in late 2025, underscoring that regulatory clearance alone does not ensure business viability. FSIS continues working toward a final labelling rule, and state legislatures are introducing new bills each session.

8.3 Technology and Investment

The cost of precision fermentation has significantly decreased over the years, from USD 1 million per kilogram in 2000 to about USD 100/kg currently, with a forecast to drop below USD 10/kg by 2030. This suggests that precision fermentation is poised to surpass livestock farming in terms of cost, capacity, speed, and volume of food production, resulting in a significant improvement in the efficiency of industrial food production.

Precision fermentation dominates the investment landscape, capturing roughly 62% of all venture capital dollars flowing into alternative proteins — USD 146 million out of USD 235 million total industry funding in Q1. Blue Horizon and Boston Consulting expect cost parity timelines of mid-2028 for fermentation milk proteins and 2029 for hybrid cultivated beef, provided public-private funding partnerships mature as anticipated.

9. Precision Fermentation: The New Protein Infrastructure

9.1 Technology Overview

Precision fermentation as an alternative to animal protein produces bioidentical proteins to the traditional ones of animal origin, having the same nutritional value and sensory properties. Unlike the analogous proteins provided by the “plant-based” industry, the proteins produced by precision fermentation offer an opportunity to respond to the growing demand for protein while addressing environmental concerns, food safety, and animal welfare issues. Since the 1980s, precision fermentation has been a proven technology commercially used for the production of human insulin, growth hormones, and enzymes such as rennet (chymosin).

Biomass fermentation uses microorganisms like yeast or fungi directly as a protein source. Precision fermentation programs microbes to produce targeted proteins, like whey, casein, and egg protein, without animals. When looking at the investment landscape, fermentation clearly stands out. According to GFI data, fermentation technologies attracted over USD 200 million in public funding in 2024.

9.2 Commercial Momentum in Europe

With the EU’s 2025 Bioeconomy Strategy, EFSA’s updated novel foods guidance, and the UK FSA’s precision fermentation business support service now in place, Europe is building the right scaffolding for faster, safer deployment. The experience for many startups in the bioeconomy sector is that capital intensity and offtake uncertainty create two valleys of death: demo to first commercial and first sale to industrial scale. Europe’s strategy answers with de-risking and demand signals.

9.3 Insect Protein

The insect protein segment projects the highest growth rates in the alternative protein landscape at 28% CAGR through 2030, though from a smaller base.

Insect proteins, though nutritionally dense and environmentally efficient, face substantial barriers related to consumer acceptance, regulatory fragmentation, and cultural resistance. The current share of proteins from insect species is the lowest compared to plant and microbial sources, highlighting a need for marginal growth through investigating new insect species as alternative protein sources.

10. The Protein Supply Chain: Cold Chain, Traceability, and Resilience

10.1 Cold Chain as Strategic Infrastructure

Food and beverage companies are navigating an increasingly complex operating environment characterised by geopolitical disruption and shifting market dynamics. In response, those companies are prioritising resilience, making greater investments in data and automation, and seeking deeper collaboration with logistics partners to enable more agile execution. Demand remains strong, with 72% reporting rising demand for refrigerated and frozen foods, underscoring the cold chain’s growing strategic importance. Technology adoption is closely tied to resilience efforts, with 60% of respondents ranking data and AI among the top forces transforming operations in 2026.

GLP-1 medications are reducing overall food consumption while increasing demand for high protein and nutrient-dense products — many of which require refrigerated storage. At the same time, GLP-1 biologics themselves require strict cold chain handling, creating new demand for pharmaceutical-grade warehousing.

10.2 Digital Traceability and Blockchain

The adoption of blockchain ensures secure and immutable records to build transparency and trust in the supply chain. IoT uses sensors and devices to monitor and report real-time data on food products. Cold-chain logistics and last-mile delivery solutions ensure that perishable goods reach consumers fresh and efficiently. Online transactions are now driving 35% of total food and beverage dollar sales growth. The global food e-commerce market was valued at approximately USD 304.7 billion in 2024 and is projected to reach USD 1,191.03 billion by 2033, growing at a CAGR of about 16.35%.

10.3 Cybersecurity and Resilience

As cold chain logistics systems become more digitised, they become attractive targets for cyberattacks. Over 80% of maritime cyber incidents originate from hostile state actors or criminal groups. To mitigate these risks, companies are investing in network segmentation and encryption to protect data streams from sensors and vehicles, and multi-factor authentication and secure protocols for accessing tracking platforms.

11. Sustainability Across the Protein Value Chain

11.1 Emissions, Land Use, and Water

The production of meat for human and animal consumption is responsible for 57% of total global food production emissions, while the global dairy sector alone contributes to 4% of global emissions. Despite these figures, the pathway to decarbonising the protein sector is neither simple nor uniform. The US Roundtable for Sustainable Beef framework is providing the industry’s most rigorous voluntary standard, covering six high-priority indicators: GHG emissions, land stewardship, water stewardship, water efficiency, employee safety and wellbeing, and animal wellbeing.

In aquaculture, sustainability progress is driven by alternative feed ingredients, closed-loop water systems, and certification programmes. Replacing fishmeal with insect protein, algae, and single-cell protein in aquafeed not only reduces marine ecosystem pressure but improves feed conversion ratios and lowers production costs over time.

11.2 The Farm to Fork Policy Framework

The EU Green Deal funding for protein diversification is driving significant advancements in the European protein market by channelling public investments into crops and technologies that expand the region’s protein base across plant, animal, and microbial sources. This initiative aligns with the Farm-to-Fork strategy and climate objectives.

For producers and processors exporting to the EU, compliance with the EU Deforestation Regulation — effective from mid-2026 — is a market access issue of the highest order. Companies supplying beef, soy, and other deforestation-linked commodities must demonstrate that their products were not produced on recently deforested land, driving investment in satellite-based land monitoring, geolocation tagging of farm parcels, and digital audit trails.

12. Strategic Outlook: The Protein Industry to 2030

The global protein industry is entering a period of permanent structural change. The convergence of pharmacological appetite modulation, precision fermentation commercialisation, geopolitical trade realignment, and escalating sustainability requirements means competitive dynamics will shift materially before the decade closes.

Protein Quality Will Outperform Protein Volume. As GLP-1 medications reduce overall caloric intake while increasing protein preference, competitive advantage shifts decisively from volume production to protein quality, bioavailability, and functional specificity. Products designed for muscle protein synthesis efficiency, satiety, or metabolic health will define the highest-growth sub-categories through 2030.

Fermentation as the Universal Protein Platform. New technologies like precision fermentation and advanced whey processing will expand the range of protein applications. The next phase of protein market trends will focus on innovation, accessibility, and products that meet health goals and changing consumer expectations. Investments made in 2026 in precision fermentation infrastructure and regulatory pathway development will determine market leadership in 2030.

Asia as the Defining Market. The centre of gravity for global protein demand continues to shift eastward. China’s middle class expansion, India’s rapid urbanisation, and the protein-hungry demographics of Southeast Asia collectively represent the most consequential demand growth opportunity in the industry’s history.

Traceability as a Licence to Trade. By 2030, digital supply chain traceability will be a prerequisite for market access in the EU, UK, and progressively in the US, Japan, and South Korea. Companies that invest now in blockchain-enabled provenance systems, satellite-monitored land use, and digital audit trails will hold a position of structural competitive advantage.

Frequently Asked Questions (FAQ)

What is the size of the global protein industry in 2026?

The global protein industry spans multiple market segments. The protein ingredients market is valued at USD 56.7 billion in 2026, growing to USD 112.9 billion by 2035. The dairy foods market stands at USD 1.06 trillion, the global seafood market at USD 406 billion, and the plant-based protein market at USD 75.78 billion. Total global animal protein and dairy value — encompassing livestock, processing, and retail — runs well in excess of USD 2 trillion when accounting for all value-chain stages from farm through retail.

What is the biggest challenge facing the protein industry in 2026?

Three simultaneous structural disruptions define the 2026 challenge landscape: the whey protein processing crisis with WPI spot prices at a record USD 11 per pound, the first contraction in global beef production in six years, and the mass adoption of GLP-1 medications fundamentally altering food consumption patterns. Beyond near-term crises, the long-term challenge is navigating the transition from an animal-protein-dominated system to a diversified protein ecosystem while maintaining food security, affordability, and environmental sustainability.

Is cultivated meat commercially available in 2026?

By mid-2026, cultivated meat has received regulatory approval in Israel, the Netherlands, Switzerland, and Japan, with applications pending in the UK, Canada, and Australia. However, commercial availability remains extremely limited, primarily to select restaurant partnerships. Widespread grocery store availability remains constrained by high production costs and insufficient bioreactor capacity. Cost parity with conventional meat is not expected before 2028–2029.

How are GLP-1 weight-loss drugs affecting the protein sector?

GLP-1 drug use results in a measurable shift in users’ consumption behaviour. Respondents claimed their consumption of foods across different snack categories dropped by between 40% and 60%, while proteins increased by 65%. With 12.4% of US adults now using GLP-1 drugs and projections of over 30 million users by 2030, this is a structural, not transitory, market force requiring adaptation across every protein brand and retailer.

What is precision fermentation and why does it matter for protein?

Precision fermentation programs microorganisms to produce specific proteins that are bioidentical to those derived from animals — including whey, casein, egg whites, and haemoglobin — without requiring the animal itself. The cost of precision fermentation has significantly decreased from USD 1 million per kilogram in 2000 to about USD 100/kg currently, with a forecast to drop below USD 10/kg by 2030.

Why is global beef production declining in 2026?

Herd rebuilding in North America and Brazil, combined with structural adjustments in China, will tighten supply and keep prices firm across major markets. US beef cow slaughter dropped by 19% in 2025, with the culling rate projected at 8.5% for 2026, below the long-term average. Per capita beef supplies will likely fall by 6% from 2020 highs, maintaining upward pressure on prices.

What is driving growth in the aquaculture sector?

The Aquaculture industry is projected to grow from USD 330.0 billion in 2025 to USD 663.9 billion by 2035, exhibiting a CAGR of 7.2%. There is a growing trend towards consumer awareness regarding the origins of seafood products, with the market responding by increasing transparency in production processes. As populations grow and dietary preferences shift towards healthier protein sources, seafood consumption is on the rise, having increased by approximately 20% over the last decade.

What is the outlook for plant-based protein in 2026?

The plant-based sector is in strategic recalibration. The consumer-facing finished-product market is contracting at the retail level, with US plant-based meat sales declining approximately 7% year-on-year. However, the ingredient-level market — pea protein, soy isolates, mycoprotein — is growing robustly, driven by sports nutrition, functional foods, aquafeed substitution, and EU policy mandates. The most successful companies are pivoting toward functional nutrition applications rather than competing directly against conventional meat.

How is the dairy industry navigating the whey crisis and market volatility?

The dairy sector is managing the WPI supply crisis through three strategies: sourcing diversification from US to European to regional alternatives, accelerating investment in precision-fermentation whey as a bioidentical supplement, and premiumising toward protein-rich dairy formats. Genomics will continue to drive protein gains as it remains the fastest and most reliable route to high components.

What does sustainability mean for the protein supply chain in 2026?

Sustainability in the 2026 protein supply chain encompasses environmental, social, and trade compliance dimensions simultaneously. Key developments include the EU Deforestation Regulation requiring verified proof of non-deforestation for beef and soy imports, mandatory supply chain due diligence in the EU and UK, MSC and ASC certification as market access prerequisites for seafood, and the EU Farm to Fork Strategy’s target of 50% plant-origin school meal protein by 2027. Blockchain-enabled traceability, satellite-based land monitoring, and digital audit platforms are transitioning from competitive differentiation tools to baseline compliance requirements.

Conclusion

The global protein industry in 2026 is defined by simultaneous convergence and divergence. Conventional protein sectors — beef, pork, dairy processing — are contracting in output while remaining essential in consumption. Aquaculture and poultry are carrying the growth mandate for animal protein. Plant-based protein is reinventing itself at the ingredient level while the consumer-facing layer recalibrates. Precision fermentation is transitioning from a niche technology to a foundational protein production infrastructure. And cultivated meat is proving that regulatory clearance is necessary but far from sufficient for commercial viability.

Across every sector, the common strategic imperatives of 2026 are clear: quality over volume, traceability as market access, Asia as the defining growth arena, GLP-1 adaptation as a product development mandate, and sustainability verification as a trade prerequisite. The organisations that will lead the global protein landscape in 2030 are those making decisive infrastructure, regulatory, and product innovation investments today — understanding that the farm-to-fork value chain is being rebuilt in real time.

Related Reports:

Global Animal Protein Industry Report 2026: Navigating Volatility and Efficiency

Global Cultivated Meat Industry Report 2026: The Scaling Pivot

Global Beef Industry Report 2026: Navigating Complexity and Carbon

Global Poultry Industry 2026: Growth, Disease, Technology and the Race to Feed the World

Global Plant-Based Protein Industry Report 2026: The Maturity Pivot

Global Seafood Industry Report 2026: The “Transformation Economy”

Global Dairy Industry Report 2026: From Volume to Resilience

Global Egg Industry Report 2026: Navigating Value and Volatility

Sources and References

© 2026 ESSFeed | essfeed.com | Intelligence for the Global Food & Beverage Value Chain