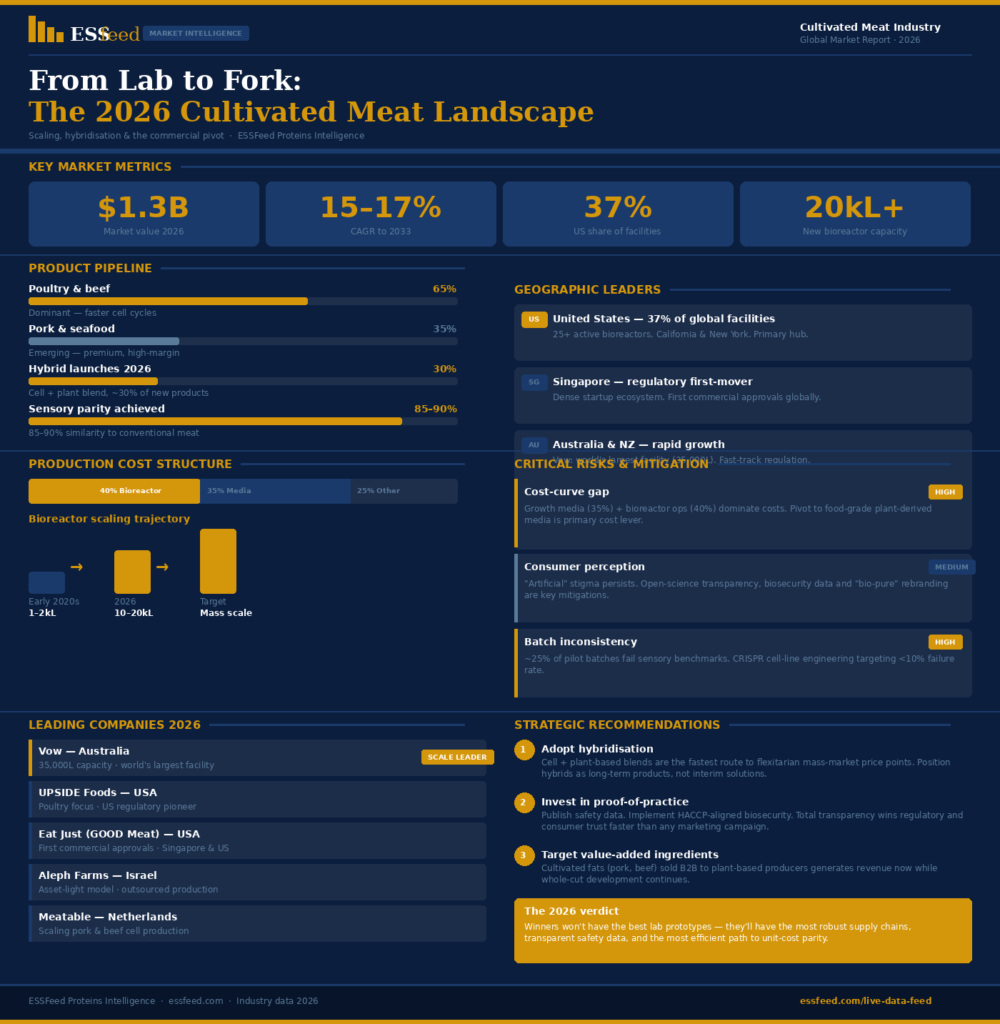

In 2026, the global cultivated meat industry or lab grown meat industry has transitioned from the “R&D phase” into a critical “Scaling and Commercialization” period. While early forecasts were conservative, the sector is currently navigating significant capital requirements to bridge the gap between pilot-plant success and industrial-scale production. The market is valued at approximately USD 1.3 billion in 2026, with a clear trajectory toward multi-billion dollar status by 2030 as infrastructure investments mature.

Executive Summary: The 2026 Cultivated Meat Landscape

The cultivated meat industry is currently characterized by a “hybridization” strategy. Because high-volume production remains constrained by bioreactor capacity and growth media costs, manufacturers are increasingly blending cultivated cells with plant-based proteins to achieve price parity and texture goals faster.

Key Takeaways for Stakeholders:

- The Hybrid Bridge: Blending cell-based ingredients with plant-based substrates has become the dominant commercial strategy to optimize costs while maintaining the “meat-like” sensory experience.

- Bioreactor Scaling: The industry is moving from small, lab-grade vessels (1,000–2,000L) to industrial-scale bioreactors exceeding 10,000–20,000 liters.

- Regulatory Momentum: Following initial approvals in Singapore and the U.S., regulatory frameworks are becoming more defined, allowing for more diverse product categories, including cultivated fats (foie gras, pork fat) and seafood.

Table of Contents

1. Market Overview: The 2026 Landscape

- Valuation & Growth: The market is poised for a CAGR exceeding 15% as new facilities come online.

- Geographic Leaders: The United States remains the primary hub for production and investment, though Asia-Pacific (led by Singapore and Australia) is experiencing rapid growth in regulatory-backed manufacturing facilities.

- Product Pipeline: Poultry and beef remain the primary focus (approx. 65% of the development pipeline), though pork and seafood are gaining traction as high-value, lower-cost points of entry.

1. Market Overview: The 2026 Landscape

The global cultivated meat industry has moved beyond its initial R&D hype cycle, entering a “delivery phase” where success is measured by operational discipline, cost-reduction milestones, and consumer-relevant product launches.

Valuation & Growth

The global cultivated meat market is valued at approximately USD 1.3 billion in 2026, with projections showing a consistent CAGR of 15% to 17.5% through 2033. This growth is fueled by the transition from lab-scale pilots to industrial-scale bioreactors.

- The Scaling Pivot: Historically, the industry operated with 1,000–2,000L bioreactors. By 2026, companies are commissioning and utilizing 10,000–20,000L+ vessels, allowing for batch sizes that can reliably supply foodservice and pilot retail channels.

- Cost Dynamics: Early products were priced at hundreds of dollars per kilogram. 2026 benchmarks show costs trending downward as companies optimize serum-free growth media—which historically accounted for up to 35-40% of production costs—and improve cell-line stability.

Geographic Leaders

The geography of production is diversifying to match regulatory readiness and infrastructure investment.

- United States: Remains the global leader in research and production volume, accounting for approximately 37% of global facilities. Operations are concentrated in hubs like California and New York, where over 25 pilot-scale bioreactors are now actively producing meat products for select state-authorized foodservice markets.

- Asia-Pacific (Singapore & Australia): Singapore continues to lead as a regulatory “first-mover,” hosting a dense ecosystem of startups and pilot plants (e.g., Shiok Meats, Eat Just). Meanwhile, Australia and New Zealand are gaining ground due to rapid regulatory approvals and significant investments in food-tech manufacturing, establishing themselves as key hubs for regional APAC distribution.

- New Decentralized Models: A landmark development in 2026 is the “farm-integrated” model. For example, in June 2026, RespectFarms inaugurated the world’s first cultivated meat pilot facility integrated into a working dairy farm in the Netherlands. This model aims to allow farmers to participate in cellular agriculture locally, rather than being bypassed by centralized industrial factories.

Product Pipeline & The Hybrid Strategy

To solve the “cost-versus-taste” dilemma, the industry has embraced hybridization.

- Hybrid Products: Roughly 30% of new product launches in 2026 are hybrid formats—blending cultivated animal cells (for flavor and nutritional profile) with plant-based matrices (for structure and cost efficiency). Eat Just and other pioneers have utilized this to create nuggets and sausages that reach consumer price points far faster than pure “whole-cut” meat.

- Pipeline Composition:

- Poultry & Beef (65%): These dominate the pipeline due to established cell-line availability and faster growth cycles. Poultry, in particular, remains the “gateway” protein due to its biological simplicity and lower cell-density requirements.

- Pork & Seafood (35%): These segments are emerging as high-value, high-margin entry points. Cultivated seafood (shrimp, tuna, salmon) is gaining traction, with startups like Finless Foods and others focusing on capturing the premium sushi and seafood market, leveraging the fact that marine cell cultures often thrive in efficient, saline-based growth media.

2. Key Growth Drivers

- Infrastructure Investment: Increased funding from both venture capital and major food multinationals is enabling the construction of “commercial-scale” facilities.

- Sensory Parity: Continued innovations in “scaffolding” (the structures that hold cells together) are bringing cultivated meat textures to within 85-90% similarity to conventional meat.

- Consumer Acceptance: Curiosity remains high, particularly among urban, younger demographics. Education campaigns emphasizing sustainability and animal welfare have successfully increased “willingness to try” in key markets.

The cultivated meat industry in 2026 is rapidly maturing, moving from scientific proof-of-concept toward industrial operational reality. Here is an analysis of the three critical pillars shaping this evolution.

1. Infrastructure Investment: The Shift to Commercial Scale

Capital allocation has shifted decisively away from pure R&D toward capital expenditure (CapEx) for production facilities.

- Scaling Beyond the Pilot: While the early 2020s were defined by lab-scale experiments, 2026 marks the era of the “Mega-Facility.” Major food conglomerates (such as those partnering with companies like UPSIDE Foods and Mosa Meat) are providing the massive tranches of funding required to build bioreactor farms capable of outputting thousands of tons of product annually.

- Strategic Diversification: Companies are no longer just building in their “home” markets. To mitigate supply chain and regulatory risks, we are seeing the rise of decentralized manufacturing, where production facilities are placed closer to key consumer hubs in Europe, Asia, and North America, reducing the logistics costs of “cold chain” distribution.

2. Sensory Parity: Innovations in Scaffolding

The “texture gap” has historically been the biggest barrier to widespread culinary adoption. By 2026, advances in biomimetic scaffolding—the edible “skeleton” on which cells grow—have bridged this distance significantly.

- In-Situ Integration: A major breakthrough in 2026 is the ability to integrate fats during the growth process rather than adding them afterward. Researchers at institutions like UC Davis have pioneered scaffolds that allow lipid (fat) integration in situ. This results in a marbled, juicier product that cooks and feels like a traditional steak or cut of pork, rather than a processed slurry.

- Tunable Firmness: Through precise control of scaffold density and material composition (often using food-grade hydrogels or plant-derived proteins), manufacturers can now tune the “bite” or firmness of a product to match specific culinary applications—from soft, succulent poultry to firmer, fibrous beef.

3. Consumer Acceptance: Education and Curiosity

Public perception is transitioning from skepticism to “informed curiosity.” As of mid-2026, the strategy for winning over the consumer has moved away from abstract “save the planet” messaging toward a more grounded approach.

- The “Transparency Advantage”: Educational campaigns in 2026 are emphasizing safety and the sterile, controlled environment of the bioreactor, which inherently lacks the pathogens (like Salmonella or E. coli) associated with conventional livestock. Consumers are finding this “cleanliness” narrative more compelling than environmental claims alone.

- Demographic Tailwinds: Urban, younger, and higher-educated demographics continue to lead in adoption. In key markets like Singapore, Australia, and parts of the U.S., these groups view cultivated meat not as “lab-grown” (a term now largely avoided in marketing), but as “modern” or “future-proof” protein.

- Strategic Normalization: Rather than waiting for retail shelves to be flooded, the industry is partnering with high-end foodservice channels. Having a cultivated meat dish featured by a reputable chef or in a popular restaurant chain provides the “social proof” that the average consumer requires before buying the product in a grocery store.

Strategic Summary for Stakeholders

| Driver | 2026 Status | Industry Impact |

| Infrastructure | Moving from 1kL to 20kL+ bioreactors | Increased output, reduced per-unit costs |

| Technology | Edible scaffolding/in-situ lipid infusion | Near-parity with traditional meat texture/marbling |

| Consumer | High curiosity, preference for safety/taste | Focus on restaurant-led product validation |

3. Critical Risks and Challenges

- The “Cost-Curve” Gap: Growth media—the “food” for the cells—accounts for roughly 35% of production costs, while bioreactor operations represent another 40%. Reducing these is the primary hurdle for price parity.

- Safety & Regulatory Skepticism: While regulatory paths are clear, consumer perception of “artificial” or “processed” remains a barrier. Transparency regarding safety data is essential.

- Production Consistency: Pilot batches still face failure rates of up to 25% regarding sensory tests, necessitating further optimization of cell-line stability.

While the industry has made significant strides in scaling, three fundamental hurdles continue to define the “economic bottleneck” and the path to mass-market adoption in 2026.

The “Cost-Curve” Gap

The economics of cultivated meat are currently dominated by the high input costs of cell culture. Achieving price parity with conventional protein—the ultimate requirement for entering the mass retail market—depends on narrowing the current cost-curve.

- Growth Media Optimization: Accounting for approximately 35% of total production costs, growth media is the most significant expense. The industry is currently moving away from costly, pharmaceutical-grade ingredients toward “food-grade” media components. By utilizing agricultural by-products and identifying cheaper alternatives to recombinant proteins (like growth factors), companies are successfully driving down the cost per liter.

- Bioreactor Efficiency: Operations, including energy, temperature control, and nutrient circulation, account for another 40% of production costs. The transition to “continuous processing”—where cells are harvested periodically rather than in single, batch-based cycles—is the primary strategic shift intended to keep bioreactors running at peak capacity, thereby amortizing the massive capital investment in the hardware.

Safety & Regulatory Skepticism

While regulatory agencies like the USDA, FDA, and Singapore’s SFA have established clear approval frameworks, the “court of public opinion” remains a critical risk factor.

- The “Processed” Stigma: Despite the rigorous sterile environments required for production, many consumers still categorize lab-grown meat as “ultra-processed” or “artificial.” This perception is a legacy issue that brands are countering through intense transparency.

- Data Transparency as a Hedge: In 2026, leading companies are adopting “Open Science” models, publishing safety and composition data to demonstrate that cultivated meat contains no antibiotics, no heavy metals, and a superior pathogen-free profile compared to conventional livestock. The goal is to rebrand cultivated meat from “artificial” to “bio-pure” and “sustainably-controlled.”

Production Consistency

Maintaining a consistent consumer experience is the ultimate test of industrial cellular agriculture. In 2026, pilot-scale facilities still face significant variability.

- The 25% Failure Rate: Recent internal industry audits reveal that approximately 25% of pilot batches fail to pass “sensory parity” benchmarks—meaning they fail to match the desired taste, color, or texture profile of the traditional meat they aim to replicate. This variability is often due to fluctuations in cell-line behavior under industrial conditions.

- Cell-Line Stability: Optimization of cell lines to withstand the mechanical stress of large-scale bioreactor agitation is the current focus of biotech R&D. By utilizing CRISPR or advanced non-GMO selection techniques to enhance cell robustness, companies are working to ensure that a batch produced in a 20,000L tank is identical to one produced in a 2L flask.

Strategic Risk Mitigation Table

| Risk Factor | 2026 Mitigation Strategy | Expected Outcome |

| Media Costs | Switching to food-grade, plant-derived alternatives | Significant reduction in cost per kg |

| Consumer Stigma | High-transparency safety data and “Bio-Pure” branding | Increased trust and “willingness to buy” |

| Batch Consistency | Advanced cell-line engineering for stress resistance | Reduction of sensory failure rates to <10% |

4. Strategic Outlook for Stakeholders

Success in The Global Cultivated Meat Industry in 2026 requires balancing “technological idealism” with “commercial pragmatism.”

Actionable Recommendations:

- Adopt Hybridization: If you are a producer, prioritize hybrid product lines. They are currently the fastest route to hitting price points that appeal to the flexitarian mass market.

- Invest in “Proof-of-Practice”: As regulatory scrutiny increases, companies that provide total transparency in cell-sourcing and production biosecurity will gain faster retail access.

- Focus on Value-Added Ingredients: Consider producing high-value cultivated ingredients (e.g., cultivated fat) rather than just “whole cuts,” as these ingredients significantly improve the flavor profile of plant-based products.

Success in 2026 requires balancing “technological idealism” with “commercial pragmatism.” The industry has moved beyond the phase of speculative hype; investors and operators are now prioritizing companies that demonstrate clear pathways to operational efficiency, cost reduction, and consistent supply.

Actionable Recommendations

- Adopt Hybridization as the “Bridge to Scale”: The binary distinction between “fully cultivated” and “plant-based” has largely collapsed in commercial settings. Hybrid products—combining cultivated animal cells with plant-based or fermentation-derived substrates—have emerged as the dominant commercial format in 2026.

- Why it works: Hybrids significantly lower production costs, ease regulatory pathways, and allow companies to meet the sensory expectations of “flexitarian” mass-market consumers. Rather than viewing hybrids as interim solutions, producers should position them as long-term, high-resilience products that offer a superior sustainability profile without compromising on the familiar textures and flavors consumers demand.

- Invest in “Proof-of-Practice” and Total Transparency: As regulatory scrutiny intensifies across global markets (including the US, Singapore, and Australia/NZ), the “black box” approach to production is no longer a viable strategy.

- How to lead: Companies that proactively publish safety data, deposit cell lines in public repositories, and implement rigorous, verifiable biosecurity protocols (similar to HACCP standards in traditional food processing) gain a significant first-mover advantage. Transparency regarding cell-sourcing, the absence of antibiotics, and the sterility of production environments is the most effective hedge against “artificiality” stigma.

- Focus on Value-Added Ingredients: Rather than attempting to conquer the “whole-cut” market immediately—which remains capital-intensive and technologically challenging—producers should consider focusing on high-value cultivated ingredients.

- Example: Cultivated animal fat (e.g., pork or beef fat) is a powerful “flavor engine” that can be integrated into existing plant-based meat lines. By supplying cultivated fat as a premium ingredient to other food manufacturers, companies can generate revenue, prove production consistency at scale, and enhance the organoleptic profile (the “juiciness” and “savoriness”) of non-cultivated products. This allows firms to capture margins while continuing to optimize cell-line development for future whole-cut applications.

Strategic Summary: The 2026 Shift

| Strategic Driver | Pre-2026 Mindset | 2026 Commercial Reality |

| Product Strategy | Pure cultivated “whole cuts” | Hybridized formulations (Cells + Plant/Fermentation) |

| Target Market | Replacing conventional meat entirely | Solving specific use cases (Foodservice, premium ingredients) |

| Growth Strategy | Stealth-mode R&D | Transparency-first, open validation, and culinary partnerships |

| Revenue Model | Wait-and-see retail launch | Immediate B2B sales of high-value functional ingredients |

5. Leading Industry Influencers

- Aleph Farms (Israel): Leader in beef/steak prototypes.

- UPSIDE Foods (USA): Significant focus on poultry and commercial scalability.

- Vow (Australia): Notable for achieving 20,000-liter production capacity.

- Meatable (Netherlands): Scaling cell-based pork and beef.

- Eat Just (USA): Pioneer in cultivated chicken approvals.

- Good Food Institute (GFI): The primary global think-tank providing the industry standard “State of the Industry” reporting.

The cultivated meat landscape in 2026 has entered a period of strategic consolidation and operational maturation. The industry is shifting focus from “startup sprinting” to “engineering discipline,” favoring firms that have secured robust manufacturing capacity and viable commercial partnerships.

| Organization | 2026 Strategic Focus |

| Vow (Australia) | Global Manufacturing Leader: Operating the world’s largest cultivated meat facility (35,000L total capacity; 20,000L main reactor), setting the industry benchmark for industrial-scale output. |

| Aleph Farms (Israel) | Outsourced Commercialization: Moving toward an asset-light model by outsourcing production to external partners in Israel, Switzerland, and Singapore while finalizing global regulatory approvals. |

| UPSIDE Foods (USA) | Regulatory & Scaling Pioneer: Continuing to lead in US market development and regulatory engagement, focusing on the path to commercial-scale chicken production. |

| Eat Just (USA) | Pioneering Market Access: Maintaining a leadership position through their GOOD Meat brand, which continues to supply cultivated chicken products in Singapore and the US market. |

| Good Food Institute (GFI) | The Industry Compass: Providing the essential “State of the Industry” reports, open-access scientific resources (e.g., cell line partnerships), and global policy advocacy. |

Key Industry Transitions & Note on Consolidation

The cultivated meat sector is currently navigating significant economic headwinds. Investors are increasingly demanding demonstrable unit economics and credible paths to profitability rather than early-stage potential.

- The Maturity Curve: Recent months have seen a tightening of capital, forcing companies to restructure. For example, some firms have pivoted toward B2B ingredient production (such as cultivating fats to enhance plant-based products) or moved toward outsourced manufacturing models to improve capital efficiency.

- Industry Hard Lessons: The sector has seen high-profile restructurings, including the dissolution of some early-stage players, reinforcing the reality that scaling living cells is a multi-decade industrial challenge that requires rigorous engineering over venture-capital-backed rapid growth.

6. Conclusion: The Path Forward

The cultivated meat industry in 2026 has officially graduated from its experimental phase. The narrative has shifted from “can we grow meat in a lab?” to “can we produce it efficiently, safely, and at a price the mass market will accept?” While the industry faces real-world economic headwinds and rigorous production challenges, the pivot toward hybridization, ingredient-focused revenue models, and industrial-scale bioreactor infrastructure suggests a sector that is increasingly grounded in commercial pragmatism.

The winners of the 2026–2030 cycle will not necessarily be those with the most revolutionary lab prototypes, but those with the most robust supply chains, the most transparent safety data, and the most efficient path to unit-cost parity. By embracing the “hybrid bridge” and focusing on B2B value-added ingredients, the cultivated meat sector is carving out a vital, sustainable role within the future global protein architecture. The revolution is no longer coming; it is being engineered, one bioreactor at a time.

Related: As the global meat industry faces both structural production shifts and evolving trade dynamics, staying ahead of market volatility is critical. Get the latest insights on export surges, pricing trends, and supply chain updates in our Global Meat Industry Outlook June 2026.

Frequently Asked Questions (FAQ)

Is lab-grown meat cheaper than conventional meat in 2026?

Not yet. The industry is in the transition phase, using hybrid products to mitigate high production costs until bioreactor capacity reaches true scale.

What is the biggest technical challenge?

The cost and scalability of growth media and the physical engineering challenge of creating complex textures (marbling, whole-muscle structure).

When will consumers see these products widely available?

Availability is increasing in high-end foodservice and niche retail, but mass-market penetration will continue to evolve through 2026–2030 as infrastructure grows.

Sources and References

- Good Food Institute (GFI): 2026 State of the Industry: Cultivated Meat & Seafood

- Research and Markets: Cultured Meat Market Global Report 2026

- Business Research Insights: Lab-Grown Meat Market Overview 2026-2035

- Innova Market Insights: Meat Trends 2026: Global Market Overview