rgultig

June 18, 2026

The top 10 beef producing countries in European bovine meat sector operates within one of the most strictly regulated agricultural frameworks in the global protein supply chain. Driven by shifting Common Agricultural Policy (CAP) mandates, rigorous traceability requirements, and aggressive decarbonization goals, Europe’s processing landscape is undergoing structural transformation. Unlike traditional pasture-heavy feedlot regions globally, a substantial portion of European beef volume is intrinsically tied to its highly specialized dairy herd, creating unique multi-tier market dynamics.

For international procurement executives, retail category directors, and industrial food manufacturing groups, understanding the precise processing distribution and regulatory landscapes of Europe’s top producers is vital for establishing robust trade relationships.

For a broader look at macroeconomic trends, production volumes, and trade shifts across international borders, see our comprehensive Global Beef Industry Report 2026.

For international procurement executives, retail category directors, and industrial food manufacturing groups, understanding the precise processing distribution and regulatory landscapes of Europe’s top producers is vital for establishing robust trade relationships. If your supply chain extends into other major global protein hubs, see our parallel directories on the high-volume Top 10 Beef Producers in the United States and the cost-competitive Top 10 Beef Exporters in India.

The Top 10 Largest Beef Producing Countries in Europe

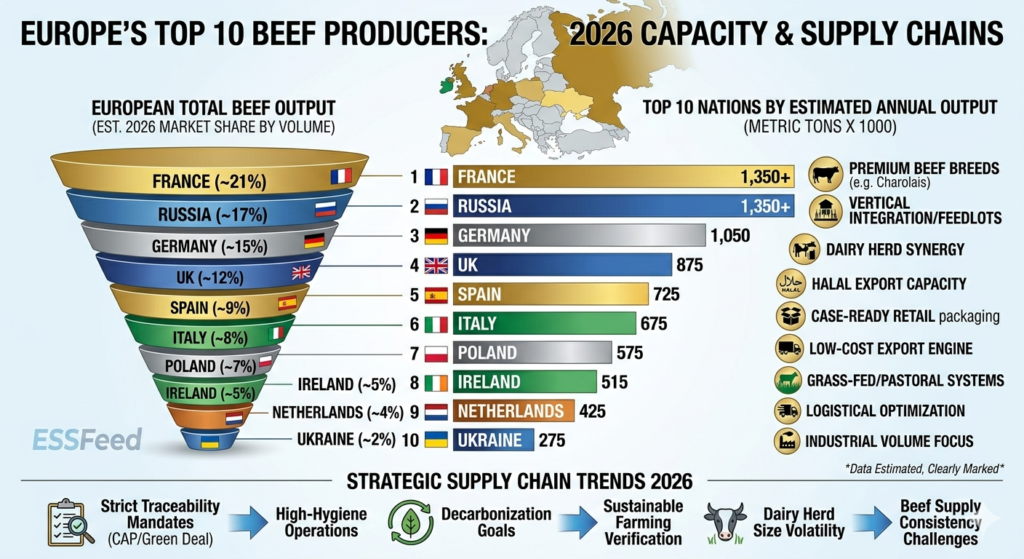

Below is the definitive breakdown of Europe’s top 10 beef producing nations, ranked by annual carcass weight output, processing infrastructure scale, and regional market footprint.

1. France

- Estimated Annual Output: ~1.3–1.4 Million Metric Tons

- Market Dynamics: France is the undisputed agricultural leader of the European Union’s beef sector, accounting for nearly 20% to 23% of total EU production volume. Driven by famous, high-yield specialized beef breeds like Charolais, Limousin, and Blonde d’Aquitaine, the French industry is highly institutionalized. Its advanced, high-hygiene processing hubs excel at delivering premium, chilled table-ready cuts to high-end European retail chains.

2. United Kingdom

- Estimated Annual Output: ~850,000–900,000 Metric Tons

- Market Dynamics: Operating outside the EU framework, the UK maintains a highly sophisticated and localized beef processing infrastructure. Its production model heavily features sustainable, grass-fed systems across Scotland, England, and Northern Ireland. Backed by rigorous domestic farm-assurance schemes, British processors focus heavily on serving premium domestic retail accounts and exporting high-value cuts to specialized European consumers.

3. Germany

- Estimated Annual Output: ~1.0–1.1 Million Metric Tons

- Market Dynamics: Germany’s massive beef output is strongly tied to its large dairy sector, with dual-purpose breeds like Fleckvieh playing a central role in the supply chain. German processing facilities are among the most technologically automated in the world, specialized in heavy-volume manufacturing trimmings, case-ready retail products, and supplying premium veal and beef lines to surrounding continental markets.

4. Russia

- Estimated Annual Output: ~1.3–1.4 Million Metric Tons (Continental Europe / CIS region)

- Market Dynamics: When examining the broader European geographic footprint, Russia stands out as a massive volume player. The Russian government has driven massive domestic investments into large-scale, vertically integrated agribusiness models (such as Miratorg) to substitute imports. By establishing Western-style commercial feedlots, they have heavily built out large-scale processing capacity to feed major urban industrial markets.

5. Spain

- Estimated Annual Output: ~700,000–750,000 Metric Tons

- Market Dynamics: Spain stands out as a key growth exception in the European landscape, actively expanding its intensive, feedlot-based fattening capacity. Backed by highly efficient grain-feeding infrastructure, Spanish processors excel at exporting both boxed beef products and live feeder cattle to North Africa and the Middle East, satisfying specific international halal and logistical requirements.

6. Italy

- Estimated Annual Output: ~650,000–700,000 Metric Tons

- Market Dynamics: Italy features a highly regionalized and quality-centric beef sector. The northern plains host highly specialized, intensive young-bull fattening farms. Italian processors excel in premium culinary differentiation, high-end charcuterie, and case-ready packaging lines tailored strictly for the domestic gourmet retail and HoReCa (Hotel/Restaurant/Café) sectors.

7. Poland

- Estimated Annual Output: ~550,000–600,000 Metric Tons

- Market Dynamics: Poland has established itself as the premier low-cost export engine of the European Union. Over 80% of Polish beef production is explicitly destined for international trade. Supported by aggressive modern plant integration and highly competitive labor structures, Polish processors are a critical supply source for industrial food manufacturers and wholesale distributors across Western Europe.

8. Ireland

- Estimated Annual Output: ~500,000–530,000 Metric Tons

- Market Dynamics: Ireland operates a world-class, export-skewed beef sector built entirely on grass-fed pastoral models. Through strict national sustainability frameworks (like Origin Green), Irish processors have achieved unmatched market access, supplying premium, grass-fed retail programs across the UK, continental Europe, and high-value Tier 1 global corridors.

9. Netherlands

- Estimated Annual Output: ~400,000–450,000 Metric Tons

- Market Dynamics: The Netherlands is a hyper-efficient logistical powerhouse. Despite its compact land area, Dutch processing facilities are elite continental hubs, acting as the EU’s single largest exporter of high-value specialized veal and processed beef products. The sector relies on extreme supply-chain optimization and advanced processing technology to maintain high-velocity distribution to neighboring Germany and France.

10. Ukraine

- Estimated Annual Output: ~250,000–300,000 Metric Tons

- Market Dynamics: Rounding out the top 10, Ukraine possesses immense raw agricultural potential with vast grain and pasture resources. Despite immense regional geopolitical and logistical constraints, independent Ukrainian processors continue to maintain essential domestic food supply lines while steadily exporting frozen beef components to Central Asia and select Middle Eastern trade channels.

The Top 10 Largest Beef Producing Countries in Europe: Strategic Market Takeaway for 2026

The European beef sector presents a highly regulated landscape where environmental compliance dictates capacity. While low-cost export integrators like Poland provide vital raw material volume for industrial manufacturing, and Western hubs like France maintain premium retail dominance, the entire continent face narrowing margins due to strict livestock emission laws. For global enterprise buyers, navigating the European supply chain successfully requires building deep partnerships with processors that demonstrate elite compliance in traceability and sustainable farming models.

Infographic: Europe’s Top 10 Beef Producers by Carcass Yield and Supply Profile

Frequently Asked Questions (FAQ)

Which country is the largest beef producer in the European Union?

France is the single largest producer of beef in the European Union, generating over 1.3 million metric tons of carcass weight annually. It is followed by Germany and Spain.

How much of European beef production is tied to the dairy industry?

A substantial percentage of European beef output—estimated between 50% and 60%—originates directly from dairy herds. This includes cull dairy cows and cross-bred dairy calves, making the entire European beef supply chain highly sensitive to dairy market economics.

What is the primary difference between Irish beef and continental European beef?

Ireland focuses almost exclusively on extensive, outdoor grass-fed pastoral production, which yields highly prized marbling and carries premium grass-fed branding. In contrast, many continental producers (like those in Germany or Italy) utilize indoor, grain-finished or crop-residue diets focusing heavily on lean meat yields from young bulls.

What major regulatory policy impacts beef processing inside Europe?

The industry is governed by the EU’s Common Agricultural Policy (CAP) and strict climate mandates under the Green Deal framework. These regulations heavily restrict environmental emissions, require total livestock electronic identification (EID) traceability, and mandate stringent animal welfare processing standards.

B2B References & Industry Sources

| Source Organization / Platform | Resource Type | Reference Link / Destination URL |

| Eurostat (European Commission) | Official Food Chain Statistics & Slaughter Trends | Inquire Eurostat Data |

| DG Agriculture and Rural Development | Live EU Beef Market Dashboards & Pricing Data | Inquire European Market Observatories |

| Bord Bia (Irish Food Board) | Grass-Fed & Sustainability Verification Frameworks | Inquire Bord Bia Insights |