rgultig · June 9, 2026

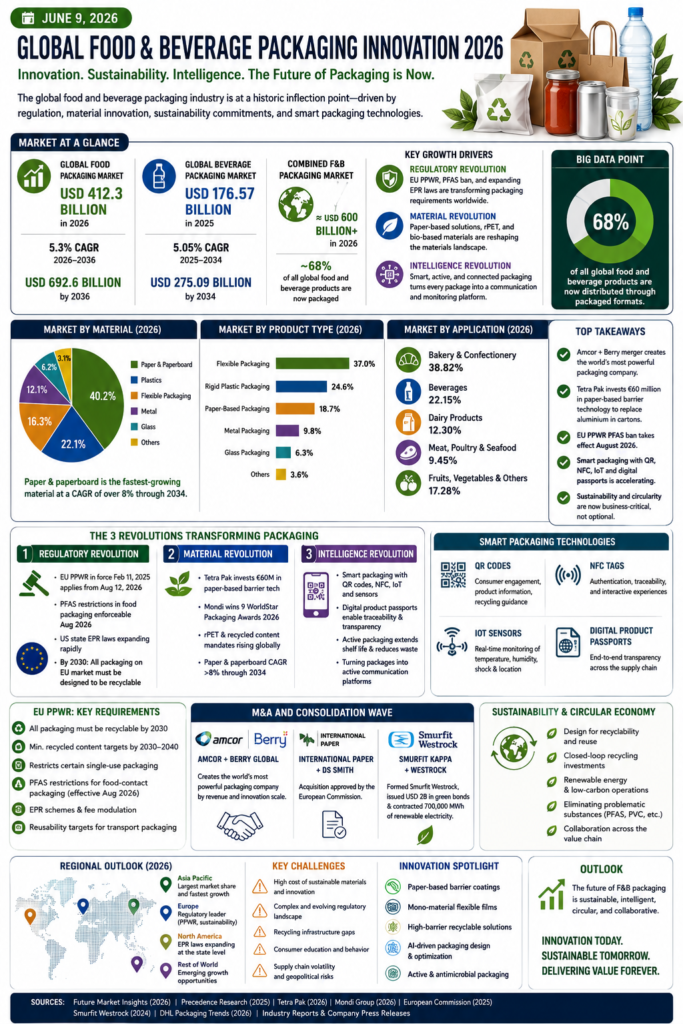

The global food packaging market is valued at USD 412.3 billion in 2026, projected to grow at a 5.3% CAGR to USD 692.6 billion by 2036. The beverage packaging market is estimated at USD 176.57 billion in 2025, growing at a CAGR of 5.05% toward USD 275.09 billion by 2034. The combined global food and beverage packaging market — encompassing all materials, formats, and technologies used to contain, protect, preserve, and communicate about food and beverage products — represents one of the largest and most fundamentally consequential industries in the global economy, with approximately 68% of all global food and beverage products now distributed through packaged formats.

The packaging industry in 2026 is navigating the most significant regulatory, material, and technology transition in its history. Three forces are simultaneously and irreversibly reshaping the category. First, the regulatory revolution: the EU’s Packaging and Packaging Waste Regulation (PPWR) entered into force on 11 February 2025 and will apply from 12 August 2026, with PFAS restrictions in food packaging becoming enforceable at that date. PPWR mandates that by 2030 all packaging on the EU market must be designed to be recyclable. Simultaneously, a patchwork of US state Extended Producer Responsibility (EPR) laws are rapidly expanding. Second, the material revolution: paper-based packaging is emerging as the decade’s defining material transition story, with Tetra Pak announcing a €60 million investment to develop paper-based barrier technologies to replace aluminium layers in aseptic cartons, and Mondi Group winning nine WorldStar Packaging Awards 2026 for sustainable paper innovations. Third, the intelligence revolution: smart packaging — integrating QR codes, NFC tags, IoT sensors, and digital product passports — is transforming packaging from a passive container into an active communication and monitoring device.

The commercial consolidation wave underscores the industry’s strategic intensity. The Amcor and Berry Global merger created a packaging powerhouse of unprecedented scale. International Paper’s acquisition of DS Smith was approved by the European Commission. And Smurfit Kappa’s merger with WestRock formed Smurfit Westrock — issuing USD 2 billion in green bonds and contracting 700,000 MWh of renewable electricity. The industry is simultaneously consolidating for scale and innovating at speed.

This report provides the most comprehensive publicly available analysis of global food and beverage packaging innovation in 2026 — covering market scale, material innovation, sustainable packaging, smart and active packaging, regulatory landscape, circular economy, e-commerce packaging, the Amcor-Berry merger, regional dynamics, key challenges, strategic outlook, and leading companies.

Executive Summary: The 2026 F&B Packaging Innovation Landscape

The global food and beverage packaging industry in 2026 is at the most consequential inflection point in its modern history — simultaneously confronting the most demanding regulatory environment ever imposed on packaging materials, the most significant material transition since the plastics revolution of the mid-20th century, and the most commercially exciting wave of smart packaging technology innovation in the industry’s history.

Key Takeaways for Stakeholders:

The global food packaging market is valued at USD 412.3 billion in 2026, growing at 5.3% CAGR to USD 692.6 billion by 2036. Beverage packaging adds USD 176.57 billion, creating a combined market approaching USD 600 billion.

The Amcor and Berry Global merger creates the world’s most powerful packaging company by revenue, specifically enabling the scale needed to fund the R&D required for PPWR compliance and sustainable packaging innovation.

Tetra Pak invested €60 million to establish a pilot plant in Lund, Sweden, dedicated to developing paper-based barrier technologies to replace the aluminium layer in aseptic beverage cartons — reducing carbon footprint of carton packaging by up to one-third.

The EU PPWR PFAS ban comes into force August 2026 — the first major PPWR compliance deadline affecting food packaging materials globally, requiring immediate removal of “forever chemicals” from food-contact packaging.

Paper and paperboard is the fastest-growing packaging material at a CAGR of over 8% through 2034, driven by the material transition away from plastic and the extraordinary innovation in paper-based barrier coatings.

Smart packaging is rising — DHL predicts 2026 will see a significant rise in smart packaging with QR codes and NFC tags. Danone is showcasing smart packaging technology enabling responsible disposal guidance. The smart packaging market is integrating IoT sensors, digital product passports, and blockchain traceability.

Flexible packaging leads by product type, supported by innovation and lightweight benefits. Bakery and confectionery holds the largest application share at 38.82% in 2026.

Smurfit Westrock won 106 packaging awards in 2024 including sustainable alternatives in the multipack beverage segment, cementing its position as the packaging industry’s sustainability innovation leader.

Table of Contents

1. Market Overview: Scale, Structure and Scope

Defining F&B Packaging

Food and beverage packaging encompasses every material, format, and technology system used to contain, protect, preserve, transport, communicate about, and enable the consumption of food and beverage products. It includes:

Primary packaging — the material in direct contact with the food or beverage product (cans, bottles, cartons, pouches, wraps, trays, jars, tubes).

Secondary packaging — the packaging that groups primary packages for retail display and distribution (cardboard cases, shrink wraps, multipack rings, shelf-ready packaging).

Tertiary/transit packaging — the packaging used to move products through the supply chain (pallets, stretch wrap, corrugated boxes, crates).

Active packaging — packaging that actively interacts with the food product or its environment to extend shelf life (oxygen scavengers, moisture absorbers, antimicrobial films, CO2 emitters).

Intelligent/smart packaging — packaging that monitors and communicates information about product conditions (temperature indicators, freshness sensors, QR codes, NFC/RFID tags, digital product passports).

Global Market Valuation

Future Market Insights projects the global food packaging market at USD 412.3 billion in 2026, growing to USD 692.6 billion by 2036 at a 5.3% CAGR. The beverage packaging market is valued at USD 176.57 billion in 2025, projected to reach USD 275.09 billion by 2034 at a 5.05% CAGR. The sustainable foodservice packaging market is valued at USD 69.7 billion in 2026, growing to USD 93.43 billion by 2031 at a 6.04% CAGR. The food packaging technology and equipment market is projected to expand from USD 48.04 billion in 2025 to USD 89.33 billion by 2035 at a CAGR of 6.4%.

Approximately 68% of all global food and beverage products are now distributed through packaged formats, highlighting the sector’s importance in modern retail and logistics systems. With over 2.5 billion metric tons of packaged food consumed globally in 2024, the packaging industry’s scale is matched only by its environmental responsibility.

Industry Structure and Consolidation

The food and beverage packaging industry is moderately concentrated at the top, with the Amcor-Berry Global merger, Smurfit WestRock combination, and International Paper-DS Smith acquisition creating three dominant multi-billion-dollar packaging platforms. The sustainable foodservice packaging market appears moderately fragmented, with a mix of large multinational corporations and smaller, specialised firms. This structure allows for diverse offerings and competitive pricing. Leading companies include Amcor, Ball Corporation, Crown Holdings, Tetra Pak, Sealed Air, Berry Global, Mondi Group, Smurfit Westrock, DS Smith/International Paper, Graphic Packaging International, and Huhtamaki.

2. The Defining M&A: The Amcor-Berry Global Merger

The Transaction and Strategic Logic

The pending all-stock combination of Amcor and Berry Global is the defining M&A event in the packaging industry in 2026. The combination creates the world’s most powerful packaging company by revenue — a global packaging platform with the scale to fund the R&D required for PPWR compliance, the sustainable materials transition, and the smart packaging technology investment that the regulatory and commercial environment demands.

The sustainable foodservice packaging market has been shaped by this intensifying consolidation — exemplified by the pending all-stock combination of Amcor and Berry Global, which signals a scaling race aimed at lowering the still-high price premium of eco-friendly formats through R&D synergies and purchasing leverage.

For food and beverage manufacturers navigating the PPWR transition, the creation of a larger, better-capitalised Amcor-Berry Global entity with deeper R&D capability, broader material expertise, and stronger regulatory intelligence is commercially valuable — providing a packaging supplier partner with the scale to invest in the sustainable material innovations that regulatory deadlines demand.

Amcor’s leadership in sustainability is recognised by inclusion in the Dow Jones Sustainability Indices Australia Index, placing the company in the top 12% of the market on sustainability performance — a credential that will be critical to maintaining customer relationships as ESG-aligned procurement becomes a commercial standard.

3. Sustainable Packaging: The Material Revolution

Paper-Based Packaging: The Decade’s Defining Material Transition

Paper and paperboard is the fastest-growing packaging material at a CAGR of over 8% through 2034 — the most significant material transition in packaging in decades. The drivers are regulatory (EU PPWR’s recyclability requirements favour paper over multi-layer plastics), consumer (preference for materials perceived as natural and recyclable), and technological (advances in barrier coatings that are expanding paper’s applicability beyond dry goods into moist, fatty, and liquid food categories).

In January 2026, Tetra Pak announced a €60 million investment to establish a pilot plant in Lund, Sweden, dedicated to developing paper-based barrier technologies. This strategic investment aims to replace the thin aluminium layer currently used in aseptic beverage cartons with a fibre-based alternative, significantly reducing the carbon footprint of the carton. Tetra Pak, in collaboration with Lactogal, has already unveiled an aseptic beverage carton featuring a paper-based barrier that reduces the carbon footprint of milk packaging by one-third.

Mondi Group was recognised with nine WorldStar Packaging Awards 2026 for its sustainable innovations, including the FreshFood BOX — a new paper-based solution designed to replace expanded polystyrene (EPS) boxes for chilled grocery deliveries, offering a fully recyclable, temperature-controlled alternative that aligns with the growing demand for sustainable e-commerce food packaging.

Smurfit Westrock produces paper-based punnets for fresh produce that are 100% recyclable, renewable, and biodegradable, optimising the supply chain while allowing consumers to efficiently recycle at home. The company’s paper innovation has been recognised with 106 industry awards and its Design2Market and SupplySmart platforms are helping food customers optimise packaging performance while reducing carbon.

As a major trend right now, according to Tetra Pak, there is continued focus on decarbonising the global food systems — with accelerated material paperisation, rising demand for verifiable carbon reductions, and greater pressure to deliver circular outcomes at scale being the three packaging dynamics defining 2026.

rPET and Recycled Content Mandates

Recycled PET (rPET) — PET plastic incorporating post-consumer recycled content — is the central material of the recycled plastics mandate that EU PPWR and US state EPR laws are creating. Most PET food and drink packaging must contain at least 30% recycled content by 2030 under PPWR; for all plastic bottles this rises to 65% by 2040. PepsiCo aims for more than 40% recycled content in primary plastic packaging by 2035, covering over 80% of its 2024 global footprint.

The first PET bottle-to-bottle recycling facility in the Western Cape of South Africa became operational in September 2024, demonstrating the global expansion of rPET infrastructure beyond the European and North American markets where it has been most advanced.

Mono-Material Packaging

Mono-material packaging — products made from a single material rather than multiple layers of different polymers — is a central strategic priority for packaging manufacturers responding to PPWR recyclability requirements. Multi-layer flexible packaging (the dominant format for snacks, confectionery, coffee, and many processed food categories) is extremely difficult to recycle because the different polymer layers cannot be separated cost-effectively.

Amcor offers a comprehensive portfolio of mono-material solutions: Mono-PE and mono-PP material for food, coffee, and home and personal care applications; mono-PP retort solutions for wet pet food, ready meals, and baby nutrition; and recycle-ready high-barrier paper solutions for confectionery products. The arrival of CEN’s Design for Recycling standards for plastic packaging in early 2026 — replacing over 20 national guidelines with one universal EU standard — is creating the standardised recyclability assessment framework that PPWR compliance requires.

In November 2024, Zotefoams launched ReZorce — a recyclable beverage carton using a mono-material design with advanced barrier technology, reducing environmental impact compared to traditional multi-layer cartons. Unlike conventional beverage cartons that combine paper, plastic, and aluminium layers (requiring specialised recycling infrastructure), ReZorce’s mono-material construction enables recycling through standard paper recycling streams.

Bio-Based and Compostable Packaging

Bio-based polymers — including polylactic acid (PLA) from cornstarch, polyhydroxyalkanoates (PHA) from microbial fermentation, and thermoplastic starch — are emerging as commercially viable alternatives to fossil-fuel-derived plastics for applications where recyclability alone does not address the end-of-life challenge. DHL predicts a rise in bio-based materials in 2026 including PLA and mushroom-based packaging grown from mycelium — materials that can break down in compost conditions within a few months.

Amcor has developed dual-end-of-life paper packaging that meets the criteria to be both recyclable and compostable at its end of life — addressing the consumer confusion around whether packaging should be placed in recycling or compost bins by making the format suitable for both waste streams. SEE (formerly Sealed Air) launched the CRYOVAC compostable overwrap tray — a USDA-certified biobased solution that reduces environmental impact without compromising strength or compatibility with existing processing lines.

Specialty food brands have moved beyond corporate commitments: “Our crisp packets are made from compostable, plant-based materials, printed with biodegradable inks and glues. After use, they can be collected, shredded, and fed into our AD process, breaking down naturally” — exemplifying the fully closed-loop, zero-waste packaging model that the most ambitious sustainable food brands are deploying.

4. Smart Packaging: Intelligence in Every Pack

What is Smart Packaging?

Smart packaging integrates active and intelligent functionalities to improve product preservation, safety, and consumer interaction. Recent advancements in food packaging have transitioned from passive containment toward innovative smart systems that integrate active and intelligent functionalities. Intelligent packaging does not act directly on food but monitors the condition of the packaged product, while active packaging acts on the environment surrounding food to increase shelf life. Smart packaging combines both — sensing and acting simultaneously.

QR Codes, NFC and Digital Product Passports

DHL says that in 2026 there will be a rise in smart packaging, which can help customers learn how to responsibly dispose of materials using QR codes and NFC tags. Danone is showcasing this technology — enabling consumers to scan packaging to receive personalised recycling guidance based on their local authority’s specific recycling capabilities.

The EU PPWR requires digital product passport capabilities for packaging — machine-readable information about packaging composition, recyclability, and lifecycle data that enables sorting infrastructure to make correct recycling decisions and enables brand owners to prove packaging compliance. QR codes and NFC tags are the primary implementation technology for digital product passports, transforming every piece of food packaging into a data carrier capable of communicating with recycling infrastructure, supply chain management systems, and consumer recycling guidance platforms.

The smart packaging market is integrating IoT sensors, digital product passports, and blockchain traceability — creating an information layer on top of the physical packaging that enables real-time monitoring of food conditions, contamination risk, and provenance verification.

Active Packaging: Extending Shelf Life

Active packaging incorporates components including oxygen scavengers, moisture absorbers, antimicrobial agents, CO2 emitters, and ethylene absorbers to enhance product quality and prolong shelf life. Battery-free, stretchable, and autonomous smart packaging is emerging from research into commercial applications — enabling continuous monitoring of food quality without the cost and complexity of battery-powered electronic components.

The development of embedded sensing systems — including chemical, temperature, and humidity sensors — enables the continuous monitoring of food quality and environmental conditions, supporting extended shelf life and early contamination detection. Advanced food packaging research is focused on biodegradable polymers and nanomaterial-enhanced substrates that combine environmental sustainability with superior barrier and antimicrobial performance.

Essential oils incorporated into edible films create active edible films with antimicrobial and antioxidant properties — a bio-based active packaging technology that extends shelf life while contributing to clean-label and sustainability positioning. Temperature-indicating labels — which change colour to signal if a product has been exposed to temperatures outside its safe range — are gaining commercial traction in the chilled and frozen food categories where cold chain compliance documentation is both a food safety requirement and a consumer trust signal.

Intelligent Packaging Indicators

Freshness indicators — chemical sensors integrated into food packaging that react to spoilage-indicating metabolites (such as biogenic amines from protein degradation) and produce a visible colour change visible to consumers and retail staff — represent the most commercially immediate application of intelligent packaging in reducing food waste. A consumer who can see that the salad dressing is still fresh, or that the chicken package has maintained safe temperature throughout its supply chain journey, makes more confident purchase decisions and wastes less food at home.

RFID-based intelligent packaging — tracking individual packages through the supply chain with unique identifiers readable without line-of-sight contact — is advancing in cold chain and premium protein applications where the investment in tracking infrastructure is justified by the value of the product and the regulatory and commercial consequences of cold chain failure.

5. The EU PPWR: The Regulatory Architecture Reshaping Global Packaging

What Is PPWR?

The EU’s Packaging and Packaging Waste Regulation (PPWR) entered into force on 11 February 2025 and will apply from 12 August 2026. PPWR is the most comprehensive and demanding packaging regulatory framework ever enacted — imposing strict recyclability standards, compositional restrictions, digital product passport requirements, and eco-modulated Extended Producer Responsibility (EPR) fees that reward more sustainable packaging through lower financial obligations.

PPWR seeks to facilitate the efficiency of the internal market by harmonising national measures on packaging and packaging waste while preventing adverse effects on the environment. It represents the replacement of over 20 national packaging guidelines across EU member states with a single, consistent EU-wide standard — creating a larger, simpler market for compliant packaging while imposing significant reformulation requirements on packaging that meets national standards but fails the EU-wide PPWR requirements.

Key PPWR Requirements and Timelines

August 2026: PFAS restrictions in food packaging come into force. PFAS (per- and polyfluoroalkyl substances) — “forever chemicals” previously used in food contact packaging for grease resistance, particularly in fast food paper packaging — must be eliminated from food-contact packaging.

2030: All packaging on the EU market must be designed to be recyclable (recycle-ready), with a few exceptions for healthcare and infant/baby nutrition packaging (2035 deadline). PET food and drink packaging must contain at least 30% recycled content.

2040: All plastic bottles must contain 65% recycled content.

PPWR provides rewards for more sustainable packaging through eco-modulated EPR schemes, with the regulation suggesting lower fees based on recyclability — creating a direct financial incentive for brands to invest in packaging recyclability beyond pure regulatory compliance motivation.

Global Regulatory Convergence

The regulatory pressure on packaging extends well beyond the EU. In the US, a patchwork of state-level Extended Producer Responsibility (EPR) laws are rapidly expanding, mandating producer responsibility for end-of-life packaging costs and requiring detailed reporting of material usage and recyclability. The Gulf Cooperation Council (GCC), Japan, and several Asian economies are implementing explicit bans on single-use plastics and setting their own recycled-content standards.

PFAS bans are expanding across North America and Europe simultaneously — with US states including California and Maine implementing food packaging PFAS restrictions that are creating de facto national standards as the most restrictive jurisdictions set the compliance floor.

6. Packaging Formats: Innovation Across Every Category

Flexible Packaging

Flexible packaging — pouches, films, wraps, bags, and sachets — leads the food packaging market by product type, supported by its extraordinary range of innovation and lightweight benefits. The flexible packaging sector is simultaneously the most challenged by PPWR (multi-layer flexible films are difficult to recycle) and the most actively innovating in response — developing mono-material flexible formats, paper-based flexible alternatives, and recyclable high-barrier flexible films that maintain food protection performance while enabling end-of-life recyclability.

Rigid Packaging: Cans, Bottles and Jars

Metal cans — aluminium and steel — are experiencing a commercial renaissance driven by their unimpeachable sustainability credentials. Aluminium is infinitely recyclable without quality degradation; steel is recycled at high rates globally. In a regulatory and consumer environment that is intensely hostile to single-use plastic, the metal can’s recyclability is a genuine commercial differentiator that food and beverage brands are increasingly using for premium positioning.

Glass bottles and jars are experiencing renewed premium positioning — particularly in the craft spirits, premium condiments, and artisan sauce categories — where glass’s aesthetic quality, inert food safety profile, and recyclability credentials align with premium brand positioning and clean-label consumer expectations.

Aseptic and Carton Packaging

The aseptic carton — Tetra Pak’s flagship product format, used for long-life milk, plant-based beverages, soups, and sauces globally — represents the most commercially significant packaging format undergoing fundamental material innovation in 2026. Tetra Pak’s €60 million pilot plant investment in paper-based barrier technology aims to replace the aluminium barrier layer with a fibre-based alternative — a transition that would reduce the carbon footprint of the carton format significantly while maintaining the extraordinary shelf-life extension that aseptic technology enables.

Aseptic cartons facilitate food security by enabling shelf-stable distribution without refrigeration in markets where cold chain infrastructure is limited. Aseptic packaging plays a key role in extending shelf life without preservatives and improves food access, while supporting recyclable, low-carbon cartons and circular systems.

Modified Atmosphere Packaging (MAP) and Vacuum Packaging

Modified atmosphere packaging — replacing the air inside food packaging with a protective gas mixture (typically nitrogen, CO2, and oxygen in ratios calibrated to the specific food product’s preservation requirements) — is one of the most commercially significant shelf-life extension technologies in the food industry. MAP extends the shelf life of fresh meat, poultry, fish, salads, and prepared foods without any artificial preservatives — aligning with the clean-label trend while delivering the commercial benefits of extended shelf life.

Sealed Air’s CRYOVAC brand — the world’s most recognised vacuum and MAP packaging system — is advancing materials innovation toward compostable and recyclable alternatives while maintaining the barrier and seal performance that food safety requires.

7. E-Commerce and Last-Mile Packaging Innovation

The Online Grocery Packaging Challenge

The rise of online grocery shopping and meal delivery services creates fundamentally different packaging requirements from conventional retail. The packaging must survive not just the controlled environment of a distribution centre but the variable conditions of last-mile delivery — including vehicle transit vibration, stacking under other packages, temperature fluctuation, and the absence of shelf-ready secondary packaging requirements.

Future Market Insights notes that e-commerce grocery, direct-to-consumer food brands, and food delivery platforms are amplifying the need for durable, leak-resistant, and thermally stable packaging solutions. The frozen food packaging market is projected to reach USD 79.59 billion by 2034, growing from USD 47.94 billion in 2025, driven by cold-chain logistics growth and smart, sustainable packaging innovations.

Sustainable E-Commerce Food Packaging

Mondi Group’s FreshFood BOX — recognised with a WorldStar Packaging Award 2026 — directly addresses the e-commerce food packaging challenge by replacing expanded polystyrene (EPS) boxes for chilled grocery deliveries with a fully recyclable, temperature-controlled paper-based alternative. This innovation is commercially significant because EPS has been one of the most environmentally problematic packaging materials in food distribution and is facing regulatory restriction in multiple markets.

The meal kit sector — HelloFresh, Daily Harvest, and their growing ecosystem of DTC food subscription services — has driven significant innovation in sustainable chilled packaging, as the DTC subscription model creates direct consumer relationships where packaging sustainability is a visible brand attribute that influences subscription retention.

8. Sustainability: Circularity as the Strategic Imperative

The Circular Economy and EPR

Circular economy initiatives are driving sustainable packaging innovations across the entire F&B packaging value chain. Extended Producer Responsibility (EPR) schemes — which make packaging producers financially responsible for the end-of-life cost of their packaging — are creating direct financial incentives for packaging sustainability that are as commercially powerful as any consumer trend.

DRS (Deposit Return Schemes) and EPR schemes expanded globally in 2025, creating the collection infrastructure that enables the closed-loop recycling systems that mono-material and rPET packaging requires. The expansion of DRS to new markets — creating deposit-refund systems where consumers receive a financial incentive for returning bottles and cans — is driving dramatic improvements in collection rates for beverage containers.

Smurfit Westrock’s investment model — USD 2 billion in green bonds and nearly 700,000 MWh of contracted renewable electricity — represents the scale of capital investment that packaging sustainability requires and is only commercially viable at the scale of the world’s largest packaging companies.

PFAS: The “Forever Chemical” Reckoning

PFAS (per- and polyfluoroalkyl substances) — fluorinated chemicals previously used in food packaging for grease and moisture resistance, particularly in fast food packaging, microwave popcorn bags, and paper food trays — have been found to be persistent environmental contaminants that bioaccumulate in human tissue and have been associated with a range of health concerns. The EU PPWR’s PFAS ban from August 2026 is the most immediate compliance challenge for food packaging manufacturers in 2026 — requiring the identification and replacement of PFAS-based barrier coatings across a significant portion of food-contact packaging currently on the market.

The PPWR will prohibit brand owners from placing food-contact packaging on the EU market if it contains PFAS above certain thresholds — creating an immediate compliance requirement that is driving investment in PFAS-free barrier coating alternatives across the paper, carton, and flexible packaging sectors.

Greenwashing Risk and Regulatory Scrutiny

Greenwashing lawsuits and NGO scrutiny exposed gaps between sustainability claims and reality across the packaging industry in 2025. The expansion of green claims regulations — the EU Green Claims Directive and equivalent national legislation requiring substantiation of environmental marketing claims — is creating a new compliance burden for packaging brands that have relied on unsubstantiated sustainability messaging.

9. Regional Dynamics

Europe: The Regulatory Vanguard

Europe leads the global packaging sustainability transition through the PPWR framework, the most comprehensive and demanding packaging regulatory architecture in the world. The arrival of CEN’s Design for Recycling standards for plastic packaging in early 2026 — replacing over 20 national guidelines with one universal EU standard — is creating the standardised recyclability framework that transforms PPWR compliance from aspiration to measurable, verifiable commitment.

European packaging innovation is concentrated in paper and fibre-based materials — with Mondi (UK), Smurfit Westrock (Ireland), Tetra Pak (Sweden), and DS Smith/International Paper (UK) all headquartered in Europe and driving the paper-based barrier innovation that PPWR requires.

Germany is the dominant European market by consumer and industrial packaging demand, and its historically high packaging recycling rates (approaching 90% for glass and metals) provide the infrastructure foundation that circular economy packaging models depend on. The UK market is simultaneously navigating post-Brexit regulatory divergence from EU PPWR while implementing its own Plastic Packaging Tax (PPT) and DRS expansion.

North America: EPR Expansion and State-Level Leadership

The United States packaging market is being reshaped by the rapid expansion of state-level EPR laws — with California, Maine, Oregon, Colorado, and a growing number of states implementing producer responsibility frameworks that create a de facto national EPR standard even in the absence of federal packaging legislation. These state laws are creating significant compliance complexity for food and beverage brands operating nationally.

The North American industrial automation in food and beverage packaging market is valued at USD 12.5 billion in 2024, growing at 6.4% CAGR — reflecting the scale of capital investment in packaging machinery and technology that food producers are deploying to handle the new material formats that sustainability requirements demand.

Asia-Pacific: Growth, Volume, and Emerging Sustainability

Asia-Pacific leads by packaging volume — driven by China’s extraordinary food production and packaged food consumption scale, India’s rapidly expanding retail sector (expected to reach USD 2 trillion by 2032), and Japan’s sophisticated packaging culture that combines premium presentation with advanced sustainability technology.

China is the major consumer of food packaging driven by frozen food demand and retail growth. India’s retail sector boom is fuelling packaging needs. The first PET bottle-to-bottle recycling facility in the Western Cape of South Africa becoming operational in September 2024 signals the global expansion of circular packaging infrastructure into emerging markets.

10. Critical Risks and Challenges

Regulatory Complexity and Compliance Cost

The fragmented global regulatory environment — with EU PPWR, US state EPR laws, GCC single-use plastic bans, and Japan’s packaging standards all creating different requirements — is generating significant compliance complexity and cost for food and beverage manufacturers operating globally. Multiple mandatory deadlines, different national definitions of recyclability, and different requirements for recycled content are creating a compliance management challenge that requires significant investment in regulatory intelligence and packaging engineering capability.

The Price Premium Challenge for Sustainable Materials

The still-high price premium of eco-friendly packaging formats relative to conventional plastics is one of the most significant commercial barriers to the sustainable packaging transition. Bio-based materials, compostable packaging, and recycled content packaging all currently carry cost premiums that food manufacturers must either absorb through margin compression or pass through to consumers who may resist higher prices.

The Amcor-Berry merger explicitly targets lowering this premium through R&D synergies and purchasing leverage — recognising that scale is the primary commercial lever for making sustainable packaging economically competitive with conventional alternatives.

Performance Gaps in Paper-Based Alternatives

While paper and paperboard are growing fastest, paper-based alternatives to plastic packaging face genuine performance challenges in moisture, oxygen, and grease barrier applications. Advances in barrier technologies are expanding the capabilities of paper packaging — with coatings derived from PLA, silica, aluminium oxide, and bio-based alternatives enabling paper to protect moisture-sensitive and fat-containing food products that were previously exclusively within the domain of plastic packaging. But the performance parity required for all food applications — particularly the most demanding moist, fatty, and acidic food categories — remains a technical frontier that paper-based barrier innovation is approaching but has not yet completely crossed.

Supply Chain Disruption for New Materials

The transition to new sustainable packaging materials — rPET, bio-based polymers, paper-based formats — requires significant changes to food manufacturers’ packaging supply chains, from sourcing and procurement through filling and sealing equipment compatibility to retailer shelf requirements and consumer acceptance. Tariffs on imported automation systems and packaging materials are adding cost pressure to the transition, particularly in Asia-Pacific and North America.

11. Strategic Outlook for Stakeholders

Actionable Recommendations

Begin PPWR Compliance Assessment Immediately: The PPWR PFAS ban applies from August 2026 — a non-negotiable compliance deadline that applies to all food packaging placed on the EU market. Food and beverage brands serving EU markets must audit their current food-contact packaging for PFAS content and have confirmed alternatives in supply chain by this date. Brands that wait for enforcement risk market access withdrawal.

Invest in Packaging Life Cycle Assessment (LCA) Capability: The most strategically valuable capability in the sustainable packaging transition is the ability to quantify and compare the lifecycle environmental impact of different packaging choices — not just material weight or recyclability label, but full cradle-to-grave carbon, water, and waste impact. Amcor’s sustainability team explicitly recommends basing packaging decisions on LCA comparison rather than assuming paper is always better. LCA capability enables evidence-based packaging decisions that withstand regulatory scrutiny and consumer challenge.

Build Smart Packaging Into New Product Launches as Standard: QR codes and NFC tags cost pennies to add to packaging and deliver multiple commercial benefits: consumer recycling guidance, product authentication, supply chain traceability, and the digital product passport compliance that PPWR requires. New product launches that do not incorporate smart packaging are missing both regulatory preparation and commercial differentiation opportunities.

Partner With Scale Packaging Suppliers for R&D Access: The Amcor-Berry merger, Smurfit Westrock formation, and International Paper-DS Smith combination are creating packaging partners with the R&D scale to continuously innovate sustainable material alternatives. Food and beverage brands that build strategic partnerships with these scale packaging companies gain early access to material innovations that can deliver competitive sustainable packaging advantages ahead of regulatory deadlines.

Strategic Summary: The 2026 F&B Packaging Model

| Strategic Priority | Traditional Approach | 2026 Competitive Standard |

|---|---|---|

| Material Strategy | Performance-first, cost-optimised | Regulatory-ready, sustainable-first, LCA-validated |

| PFAS and Chemicals | Legacy coating materials | PFAS-free alternatives in all food-contact packaging |

| Recyclability | Claim-based sustainability | Verified recycle-ready design per CEN Design for Recycling |

| Smart Packaging | Optional QR codes | Digital product passports + NFC + sensor integration standard |

| Consumer Communication | Label-based disposal guidance | Smart packaging with personalised local recycling guidance |

| Supply Chain Transparency | Proprietary traceability | Blockchain-verified farm-to-shelf digital documentation |

12. Leading Industry Companies

| Company | Region | Strategic Focus |

|---|---|---|

| Amcor plc (merging with Berry Global) | Australia/USA/Global | World’s most comprehensive sustainable packaging portfolio — mono-PE, mono-PP, recycle-ready paper, dual end-of-life paper/compostable solutions. PPWR regulatory leadership. Dow Jones Sustainability Index top 12%. The combined Amcor-Berry entity will be the world’s largest packaging company by revenue. |

| Smurfit Westrock | Ireland/USA/Global | Global leader in paper-based sustainable packaging. USD 2 billion in green bonds. 700,000 MWh renewable electricity contracted. 106 industry awards including Innovation and Sustainability of the Year. FreshFood BOX and paper produce punnets for sustainable e-commerce and fresh food. Design2Market and SupplySmart customer platforms. |

| Tetra Pak International | Switzerland/Global | Aseptic carton market leader. €60 million pilot plant investment in paper-based barrier technology (January 2026). Paper-based barrier carton reducing carbon footprint by one-third co-developed with Lactogal. Focused on decarbonising global food systems through paperisation. |

| Mondi Group | UK/Global | Nine WorldStar Packaging Awards 2026. FreshFood BOX replacing EPS for chilled e-commerce delivery. Barrier coating innovation supporting circular economy transition. Strong in paper-based and sustainable flexible packaging. |

| International Paper / DS Smith | USA/UK/Global | Combined global corrugated and paper packaging leader following EC-approved acquisition. Strong in sustainable secondary packaging and e-commerce packaging solutions for food. |

| Ball Corporation | USA/Global | World’s leading aluminium beverage can manufacturer. Aluminium’s infinite recyclability is its core sustainability proposition. Lightweight can design reducing metal content per unit. |

| Crown Holdings | USA/Global | Global metal can and glass container leader. Strong in food cans, aerosols, and beverage cans. Sustainability investment in lightweight design and recycled material content. |

| Sealed Air (SEE) | USA/Global | CRYOVAC brand — world’s leading vacuum and MAP packaging. CRYOVAC compostable overwrap tray (USDA certified biobased). Innovation in sustainable protective packaging for food manufacturers. |

| Huhtamaki | Finland/Global | Fibre-based and flexible food packaging specialist. Strong in food-to-go and foodservice sustainable packaging. Leading in moulded fibre food packaging as plastic alternative. |

| Syntegon | Germany/Global | Food packaging technology and equipment. AIM9 high-speed inspection platform launched February 2026 with high-resolution cameras for automated visual inspection. CS VS600 and Homogenizer 250 for protein beverage packaging. |

Related: As the industry accelerates toward higher automation and sustainable material compatibility, packaging lines are undergoing a major technological transformation. Explore the advancements in high-speed machinery and smart systems driving efficiency in our Food & Beverage Packaging Equipment Industry Report 2026.

Frequently Asked Questions (FAQ)

What is the global food and beverage packaging market size in 2026?

The global food packaging market is valued at USD 412.3 billion in 2026, projected to grow at a 5.3% CAGR to USD 692.6 billion by 2036. The beverage packaging market is valued at USD 176.57 billion in 2025, growing at a 5.05% CAGR toward USD 275.09 billion by 2034. The sustainable foodservice packaging market adds USD 69.7 billion in 2026, growing to USD 93.43 billion by 2031. The food packaging technology and equipment market is projected to grow from USD 48.04 billion in 2025 to USD 89.33 billion by 2035. The combined global food and beverage packaging market approaches USD 600 billion in 2026, making it one of the largest manufacturing industries globally. Approximately 68% of all global food and beverage products are distributed through packaged formats, with over 2.5 billion metric tons of packaged food consumed globally in 2024.

What is the EU PPWR and what does it mean for food packaging?

The EU Packaging and Packaging Waste Regulation (PPWR) entered into force on 11 February 2025 and will apply from 12 August 2026. It is the most comprehensive packaging regulatory framework ever enacted globally, imposing strict recyclability standards, compositional restrictions (including a PFAS ban from August 2026), digital product passport requirements, and eco-modulated EPR fees that reward more sustainable packaging through lower financial obligations. By 2030, all packaging on the EU market must be designed to be recyclable, with most PET food and drink packaging required to contain at least 30% recycled content; by 2040, all plastic bottles must contain 65% recycled content. PPWR provides a roadmap for packaging circularity and creates direct financial incentives for recyclability investment through lower EPR fees for compliant packaging. For food and beverage manufacturers, PPWR requires immediate action on PFAS removal, medium-term investment in recycle-ready packaging design, and long-term commitment to recycled content targets.

What is smart packaging and how is it changing the food industry?

Smart packaging integrates active and intelligent functionalities to improve product preservation, safety, and consumer interaction. Active packaging incorporates components — oxygen scavengers, moisture absorbers, antimicrobial films, temperature indicators — that actively extend shelf life by modifying the environment inside the package. Intelligent packaging uses sensors, indicators, QR codes, NFC tags, and RFID to monitor and communicate information about product conditions. Smart packaging is changing the food industry across four dimensions: shelf life extension through active components that maintain optimal storage conditions throughout distribution; food safety through temperature indicators that signal cold chain breaches and freshness sensors that detect spoilage metabolites; consumer engagement through QR codes and NFC tags providing recycling guidance, product information, and authentication; and supply chain traceability through digital product passports and blockchain-integrated data carriers that provide verifiable farm-to-fork provenance. DHL predicts a rise in smart packaging in 2026 as QR and NFC technology becomes standard on food packaging. Danone is showcasing smart packaging that enables responsible disposal guidance based on local recycling capabilities.

What is the Amcor-Berry Global merger and why does it matter?

The pending all-stock combination of Amcor and Berry Global creates the world’s most powerful packaging company by revenue — combining Amcor’s global leadership in flexible packaging, healthcare packaging, and sustainability innovation with Berry Global’s broad product portfolio across rigid, flexible, and protective packaging. The deal matters for the food and beverage industry because it signals a scaling race in packaging sustainability — the rationale explicitly includes lowering the still-high price premium of eco-friendly packaging formats through R&D synergies and purchasing leverage. For food manufacturers navigating the PPWR transition, the combined entity provides a packaging supplier with the scale to fund continuous sustainable material innovation, maintain the world’s most comprehensive regulatory compliance expertise, and deliver the recycle-ready, PFAS-free, and bio-based packaging alternatives that regulatory deadlines demand. Amcor is already recognised in the Dow Jones Sustainability Indices, placing it in the top 12% of the market on sustainability performance.

What is replacing plastic in food packaging?

Several materials and technologies are replacing plastic in food packaging in 2026. Paper and paperboard — growing at the fastest CAGR of over 8% — is the primary material transition driver, with innovations in barrier coatings (bio-based, mineral, and aluminium-oxide coatings) enabling paper to perform in moisture, grease, and oxygen-sensitive applications previously exclusive to plastic. Mono-material recycled PET (rPET) replaces conventional multi-layer flexible packaging with a single recyclable material. Bio-based polymers — PLA from cornstarch and PHA from microbial fermentation — provide compostable alternatives for applications where recyclability alone is insufficient. Metal cans (aluminium and steel) are experiencing commercial renaissance driven by infinite recyclability. Tetra Pak’s paper-based barrier technology is replacing the aluminium layer in aseptic cartons. However, paper-based alternatives still face genuine performance challenges in the most demanding food applications — moisture, fatty, and acidic food categories — that barrier technology innovation is progressively addressing.

Who are the leading food and beverage packaging companies in 2026?

The global food and beverage packaging market is led by a combination of material-specific specialists and diversified packaging platforms. Amcor (merging with Berry Global) is the world’s leading flexible and consumer packaging company. Smurfit Westrock is the global leader in paper-based sustainable packaging, recognised with 106 industry awards in 2024. Tetra Pak leads aseptic carton packaging for beverages and dairy. Ball Corporation and Crown Holdings lead in aluminium and metal packaging. Mondi Group leads in paper-based sustainable packaging innovation, winning nine WorldStar Packaging Awards 2026. International Paper (combined with DS Smith) leads in corrugated and paper secondary packaging. Sealed Air (SEE) leads in vacuum and MAP food protection packaging. Huhtamaki leads in fibre-based foodservice packaging. In packaging equipment and technology, Syntegon and Tetra Pak are the leading food packaging system providers.

What are PFAS and why are they being banned from food packaging?

PFAS (per- and polyfluoroalkyl substances) are a class of fluorinated chemicals previously widely used in food packaging for their grease and moisture resistance properties — particularly in fast food wrappers, microwave popcorn bags, pizza boxes, and paper food trays. They are called “forever chemicals” because they do not break down naturally in the environment or in the human body, accumulating over time in water, soil, wildlife, and human tissue. Research has associated exposure to certain PFAS with a range of health concerns. The EU PPWR’s PFAS ban from August 2026 prohibits food-contact packaging on the EU market from containing PFAS above specified thresholds. US states including California and Maine are implementing equivalent bans. Food packaging manufacturers are replacing PFAS-based barrier coatings with alternatives including bio-based coatings, silica-based coatings, and fluorine-free polymers that achieve equivalent grease and moisture resistance without the environmental persistence and health concerns of PFAS compounds.

Sources and Additional References

- Future Market Insights: Food Packaging Market Size, Share & Forecast to 2036 — https://www.futuremarketinsights.com/reports/food-packaging-market

- Global Market Insights: Beverage Packaging Market Size & Share 2026–2035 — https://www.gminsights.com/industry-analysis/beverage-packaging-market

- Towards Packaging: Beverage Packaging Market Trends and Size 2026–35 — https://www.towardspackaging.com/insights/beverage-packaging-market-sizing

- Towards Packaging: Food Packaging Market Size and Trends 2026–2035 — https://www.towardspackaging.com/insights/food-packaging-market

- Towards Packaging: Food Packaging Technology and Equipment Market Trends & Size 2026–2035 — https://www.towardspackaging.com/insights/food-packaging-technology-and-equipment-market-size

- Fortune Business Insights: Food Packaging Market Size, Share, Trends & Growth 2034 — https://www.fortunebusinessinsights.com/industry-reports/food-packaging-market-101941

- Mordor Intelligence: Sustainable Foodservice Packaging Market Growth, Size & Companies — https://www.mordorintelligence.com/industry-reports/sustainable-foodservice-packaging-market

- MarketsandMarkets: Food Packaging Market Size Set for Strong Growth Through 2030 — https://www.marketsandmarkets.com/blog/FB/food-packaging-market

- Amcor: Packaging and Packaging Waste Regulation Top 6 Things to Know — https://www.amcor.com/insights/blogs/packaging-and-packaging-waste-regulation

- Amcor: Packaging Sustainability Regulation in Europe 2026 — https://www.amcor.com/insights/blogs/eu-regulatory-outlook-2026

- Packaging Insights: Tetra Pak — Balancing Packaging Decarbonization and Food Security — https://www.packaginginsights.com/news/tetra-pak-sustainability-packaging-food-security.html

- Packaging Insights: 2025 in Review — Tougher Regulations, Tariff Uncertainty and Greenwashing Lawsuits — https://www.packaginginsights.com/news/packaging-2025-regulation-tariffs-greenwashing-352271.html

- Speciality Food Magazine: Meet the Packaging Heroes — Sustainable Champions 2026 — https://www.specialityfoodmagazine.com/news/sustainable-champions-2026-meet-the-packaging-heroes

- Millionpack: Food Packaging Trends 2026 — From Sustainability to Smart Solutions — https://millionpack.com/food-packaging-trends/

- FifthRow: Accelerating Sustainable Packaging Innovation in Food and Beverage Through Regulatory and Risk Intelligence — https://www.fifthrow.com/blog/Accelerating-sustainable-packaging-innovation-in-food-beverage-through-regulatory-risk-intelligence

- DHL / Sustainability Magazine: What Is the Future of Sustainable Packaging? — https://sustainabilitymag.com/news/dhl-what-is-the-future-of-sustainable-packaging

- Market Research Future: Sustainable Foodservice Packaging Market Size, Share 2035 — https://www.marketresearchfuture.com/reports/sustainable-foodservice-packaging-market-29717

- NIH / NCBI: Latest Advances in Active Materials for Food Packaging and Their Application — https://www.ncbi.nlm.nih.gov/pmc/articles/PMC10670037/

- NIH / NCBI: Advances and Challenges in Smart Packaging Technologies for the Food Industry — https://www.ncbi.nlm.nih.gov/pmc/articles/PMC12733193/

- arxiv.org: Battery-free, Stretchable, and Autonomous Smart Packaging — https://arxiv.org/pdf/2501.14764

- 360 Research Reports: Food and Beverage Packaging Market 2026–2035 — https://www.360researchreports.com/market-reports/food-and-beverage-packaging-market-201413

- Technavio: Food and Beverage Packaging Machinery Market Growth Analysis 2026–2030 — https://www.technavio.com/report/food-and-beverage-packaging-machinery-market-industry-analysis