June 9, 2026

Every food and beverage product that reaches a consumer — from a bottle of mineral water to a frozen ready meal, from a can of energy drink to a bag of coffee — passes through the packaging and equipment value chain first. In 2026 The Food And Beverage Packaging and Equipment Industry sits at the intersection of five of the most powerful forces reshaping global commerce simultaneously: sustainability regulation, artificial intelligence, food safety imperatives, e-commerce growth, and emerging market industrialisation.

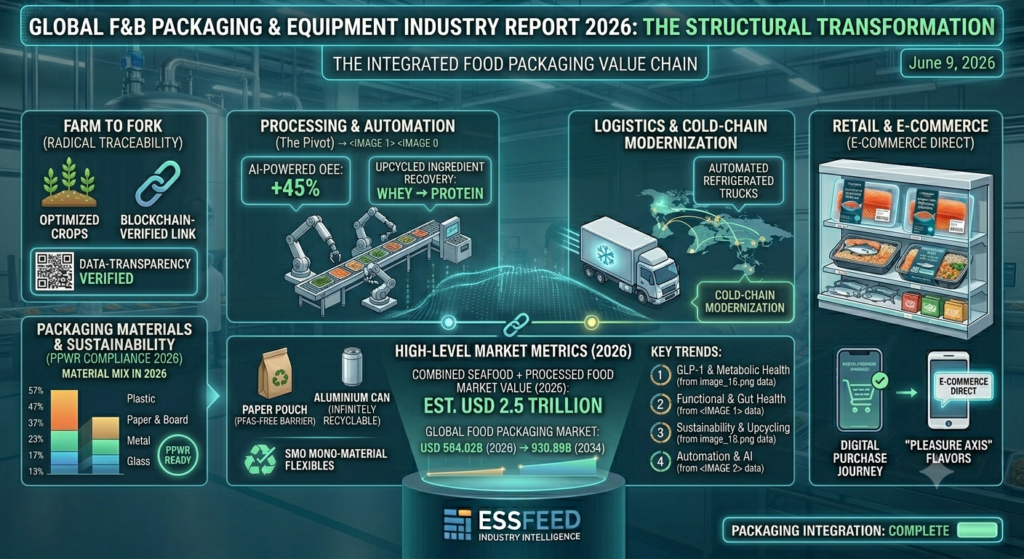

The global food packaging market size was valued at $533.22 billion in 2025 and is projected to grow from $564.02 billion in 2026 to $930.89 billion by 2034. When combined with the beverage packaging segment and the processing and packaging equipment market, the combined sector represents one of the largest and most strategically critical industries in the global food and beverage value chain. The food processing and packaging equipment market alone grew from USD 110.10 billion in 2025 to USD 118.80 billion in 2026, with expectations to reach USD 189.66 billion by 2032 at a CAGR of 8.07%.

This report provides the most comprehensive publicly available analysis of the global food and beverage packaging and equipment industry in 2026 — covering market size, material trends, sustainability regulation, smart and active packaging, processing equipment, regional dynamics, key challenges, technology innovation, strategic outlook, leading companies, and an FAQ section for industry professionals and investors.

Executive Summary: The 2026 Food And Beverage Packaging and Equipment Industry Landscape

The food and beverage packaging and equipment industry in 2026 is defined by a single overarching imperative: do more with less, and prove it. Consumers, retailers, and regulators are demanding packaging that is sustainable, traceable, functional, and cost-efficient — simultaneously. Equipment operators are being asked to automate, digitise, and decarbonise while maintaining throughput and managing input cost volatility.

Key Takeaways for Stakeholders:

Sustainability has moved from voluntary to mandatory: The EU’s Packaging and Packaging Waste Regulation (PPWR) is here to stay. The arrival of CEN’s Design for Recycling standards for plastic packaging in early 2026 marks a turning point, replacing over 20 national guidelines with one universal EU standard. By 2030, recycled content must account for 35% of plastic in non-contact-sensitive packaging, and 10% in contact-sensitive packaging.

Smart packaging is scaling rapidly: The global active and intelligent packaging market was valued at USD 16.2 billion in 2026 and is projected to reach USD 41.4 billion by 2035, at a CAGR of 11%. The package is transitioning from a passive container into an active participant in food safety, supply chain visibility, and consumer engagement.

Automation is now a survival strategy: The food and beverage processing equipment market expanded from USD 71.85 billion in 2025 to USD 76.16 billion in 2026, projected to reach USD 113.06 billion by 2032 at a CAGR of 6.69%. Labour shortages, food safety requirements, and margin pressure are converging to make automation the default operational strategy for every scale of manufacturer.

The Amcor-Berry Global merger redefined the competitive landscape: In April 2025, Amcor completed its USD 8.4 billion all-stock combination with Berry Global, creating one of the world’s largest packaging companies. This consolidation signals the scale of investment required to lead in a market increasingly defined by R&D-intensive sustainability and technology capability.

Paper is making a structural comeback: In January 2026, Tetra Pak announced a €60 million investment to establish a pilot plant in Lund, Sweden, dedicated to developing paper-based barrier technologies. Paper and fibre-based packaging is experiencing the most significant structural demand shift in decades as PFAS restrictions, plastic taxes, and consumer preference converge.

Table of Contents

1. Market Overview: Scale, Structure and Growth

Combined Market Valuation

The global food and beverage packaging and equipment sector is a multi-trillion-dollar complex spanning primary packaging materials, secondary and tertiary packaging formats, smart and active packaging technologies, processing equipment, filling and sealing systems, labelling, inspection, and end-of-line automation.

The food and beverage packaging market is worth USD 525.27 billion in 2025, growing at a 4.24% CAGR and forecast to hit USD 646.47 billion by 2030. Major companies operating in the market include Mondi plc, Amcor Plc, Berry Global Inc, DS Smith and Tetra Pak International S.A.

The global beverage packaging market progressed from USD 142.7 billion in 2025 to an estimated USD 149.7 billion in 2026, with analysts predicting USD 241.5 billion by 2036 at an implied 4.9% CAGR. Expansion is less about cyclical volume and more about policy-driven mix shifts, as regulatory “compliance gates” are pulling forward capital expenditure on recycled-content capability and pushing procurement toward post-consumer recycled inputs across bottling operations.

Material Mix in 2026

Approximately 47% of packaging materials in the food and beverage industry comprise plastic-based formats, followed by 23% paper and cardboard, 17% metal, and 13% glass. Flexible packaging solutions account for 41% of total consumption, while rigid packaging maintains a 37% share.

The plastics segment dominated the food packaging market, accounting for 46.84% of market share in 2026. Bakery and confectionery held the largest application share at 38.82% in 2026. However, the relative dominance of plastics is under the most significant structural challenge in the industry’s history, as regulatory pressure, consumer sentiment, and material science innovation all point in the same direction: reduction, replacement, and recyclability.

Processing Equipment Market

The global food and beverage processing equipment market is estimated to be valued at USD 76.39 billion in 2026 and is expected to reach USD 107.74 billion by 2033, exhibiting a CAGR of 5.9%. Processing equipment encompasses the full spectrum of food and beverage manufacturing technology — from mixing, blending, and thermal processing systems through to filling, capping, labelling, inspection, and end-of-line automation. Digitisation and sustainability are at the core of decision-making, making strategic equipment investment key to competitive advantage in this sector.

2. Packaging Material Categories: Deep Dives

Plastics: Reformulation Under Pressure

Plastic packaging remains the dominant material in food and beverage packaging by volume, valued for its barrier properties, light weight, cost efficiency, and design flexibility. However, the regulatory, consumer, and environmental pressures on single-use and non-recyclable plastic formats are the most significant structural challenge facing the industry in 2026.

The EU’s PPWR provides a clear roadmap for packaging circularity. By 2030, recycled content must account for 35% of plastic in non-contact-sensitive packaging. This is driving innovation in recycled polyolefins and alternative substrates, particularly for contact-sensitive applications outside PET.

The industry response has been decisive. Major consumer goods firms now exceed legislation by pledging 25–50% post-consumer recycled content portfolio-wide by 2030. Amcor’s supply of 1,000 tons of recycled plastic for Cadbury wrappers exemplifies voluntary targets setting de facto industry baselines.

Paper and Fibre: The Structural Renaissance

Paper and fibre-based packaging is experiencing a renaissance in 2026 — not from nostalgia, but from structural regulatory and consumer drivers. The EU’s restriction on per- and polyfluoroalkyl substances (PFAS) in food-contact materials has eliminated a broad class of performance coatings used in traditional paper-based packaging, driving intensive R&D investment into alternative barrier technologies.

Tetra Pak announced a €60 million investment to establish a pilot plant in Lund, Sweden, dedicated to developing paper-based barrier technologies, designed to replace expanded polystyrene boxes for chilled grocery deliveries and offering a fully recyclable, temperature-controlled alternative.

Western Europe accounted for 45% of food and beverage packaging tracked to have eco-friendly claims between 2021 and 2025, with paper-based formats representing the largest share of those claims as brands transition from plastic to paper across categories ranging from snack packaging to beverage cartons to e-commerce shipping solutions.

Metal: Recyclability as a Competitive Advantage

Aluminium cans and steel packaging are experiencing a resurgence driven by their unimpeachable recyclability credentials. Aluminium is infinitely recyclable without quality degradation — a characteristic that gives it a unique advantage in an era of mandatory recycled content requirements. The beverage can is arguably the most sustainable high-volume packaging format in the market, and major soft drink, energy drink, and water brands are actively shifting volume from PET bottles to cans as sustainability commitments and consumer preference align.

Glass: Premium, Sustainable, but Capital-Intensive

Glass packaging maintains its premium positioning and benefits from strong sustainability credentials — it is 100% recyclable and chemically inert. However, its weight disadvantage (which increases logistics carbon footprint), higher energy requirements in production, and significant capital intensity in both manufacturing and return-refill systems limit its scalability relative to alternative sustainable formats.

Flexible Packaging: Innovation at the Leading Edge

The flexible packaging market for food and beverages is projected to account for over 25% of the global flexible packaging market share by 2026. Flexible packaging — pouches, bags, wraps, films, and sachets — offers the most design flexibility, the lowest material-to-product weight ratio, and the most active innovation pipeline of any packaging format.

In 2024, over 48% of new product launches across the food and beverage sector incorporated sustainable packaging materials such as plant-based polymers and recycled paper. Smart packaging, which includes freshness sensors and tamper indicators, has grown by 19% in application across beverage and dairy categories.

The primary challenge with flexible packaging has historically been recyclability — multilayer flexible structures combining different polymers are difficult or impossible to recycle in conventional streams. The industry’s response in 2026 has been a major push toward mono-material flexible packaging — structures made from a single polymer type that can be recycled in standard streams — without sacrificing the barrier performance required for food safety.

3. Smart and Active Packaging: The Intelligent Package Revolution

Market Scale and Growth

The global active and intelligent packaging market was valued at USD 14.9 billion in 2025, growing to USD 16.2 billion in 2026, and projected to reach USD 41.4 billion by 2035 at a CAGR of 11%. The intelligent packaging segment is expected to grow at a CAGR of 12.8% through the forecast period, supported by rising use of RFID tags, freshness indicators, QR codes, and real-time condition monitoring solutions.

The global smart packaging market was valued at approximately $26.06 billion in 2025 and is projected to grow to around $27.55 billion in 2026, reaching roughly $42.40 billion by 2034 at a CAGR of approximately 5.54%.

Active Packaging: Extending Shelf Life, Reducing Waste

Active packaging goes beyond passive barrier protection to actively interact with the product environment — absorbing oxygen, emitting antimicrobial agents, regulating moisture, or providing controlled temperature management. In 2026, the most commercially significant applications include:

Oxygen scavengers embedded in packaging films or sachets extend shelf life of meat, bakery products, and fresh produce by removing residual oxygen from the pack headspace — a critical driver of spoilage and rancidity.

Modified atmosphere packaging (MAP) replaces the internal gas environment of a package with a controlled mixture of nitrogen, carbon dioxide, and residual oxygen optimised for the specific product — standard practice across fresh meat, poultry, cheese, and salad categories.

Antimicrobial packaging incorporating silver nanoparticles, natural plant extracts, or bacteriophage-based coatings is moving toward commercial scale, particularly for high-risk perishable categories.

Intelligent Packaging: The Data-Generating Package

IoT-enabled packaging systems utilise various sensors — including humidity, temperature, and microbial detectors — to monitor food conditions throughout the supply chain. These sensors use wireless connections like Wi-Fi, Bluetooth, 5G, and near-field communication (NFC) to share real-time data with stakeholders. Perishable foods such as dairy products and seafood packed in IoT sensor-based packaging can send alerts to food distributors to manage temperature excursions during the supply chain.

Track and trace systems are reducing recall management costs by 40%. The focus on hygienic equipment design and clean-in-place systems remains critical, particularly for machinery handling sensitive food products.

QR codes have become one of the most common forms of smart packaging. Many food brands now use QR codes on packaging to provide consumers with additional information, such as product origin, ingredient sourcing, or sustainability initiatives.

Smart Packaging 4.0: The Blockchain-Connected Package

The integration of IoT and RFID technologies across supply chain nodes — from manufacturers and processors to distributors and retailers — enables unprecedented levels of end-to-end visibility. This connectivity allows the supply chain to transition from a reactive “detect-and-fix” approach to a proactive “predict-and-prevent” model. The package functions not merely as a container but as a traceable resource unit that maintains a digital identity, ensuring data integrity through distributed ledgers like blockchain to resolve the “trust gap” in global food trade.

4. Sustainability: The Industry’s Defining Transformation

The Regulatory Landscape in 2026

The sustainability transformation of food and beverage packaging is no longer voluntary. In 2026, the regulatory framework is crystallising rapidly across all major markets, creating both compliance obligations and commercial opportunities for operators who move proactively.

The EU’s Packaging and Packaging Waste Regulation provides a roadmap for packaging circularity. The arrival of CEN’s Design for Recycling standards for plastic packaging in early 2026 replaces over 20 national guidelines with one universal EU standard, creating the basis for PPWR recyclability assessments. By 2030, recycled content must account for 35% of plastic in non-contact-sensitive packaging.

Amcor’s VP Sustainability Operations and Advocacy, Alejandro Beltran, highlights the PPWR’s ambitious targets for recycled content and recyclability as a major industry focus for 2026. “Particularly for contact-sensitive applications outside PET, this will drive innovation in recycled polyolefins and alternative substrates.”

The Overcapacity Challenge in Paper and Board

Driven largely by massive investments in Asia, the global containerboard market is facing an overcapacity of approximately 23 million tonnes in 2026. The cartonboard market is not far behind, with a surplus of around 10 million tonnes. While overcapacity should theoretically lower prices, other factors — including high energy costs and potential mill closures — can keep floors under pricing. For F&B manufacturers transitioning from plastics to paper-based packaging, this overcapacity dynamic is creating a buyer’s market in paper substrates — a material cost tailwind that makes the sustainability transition more financially viable.

Consumer Sustainability Expectations

According to a 2025 global packaging consumer survey of approximately 11,000 consumers across 11 countries, the top sustainability attribute shoppers look for is recyclability, followed by reusability and inclusion of recycled content. In all geographies surveyed, at least 40% of consumers said they would pay a little more for sustainable packaging. The commercial opportunity is clear: premium pricing for credibly sustainable packaging is achievable across all major consumer markets, but requires the verifiable sustainability credentials that are increasingly only deliverable through smart packaging traceability technology.

5. Food and Beverage Processing Equipment

Market Dynamics

The food and beverage processing equipment market expanded from USD 71.85 billion in 2025 to USD 76.16 billion in 2026, projected to continue at a CAGR of 6.69% to reach USD 113.06 billion by 2032. This period of consistent growth reflects a surge in automation adoption, adherence to advancing food safety and environmental standards, and ongoing evolution in supply chain strategies.

Processing equipment encompasses the full technology stack of food and beverage manufacturing — from raw material intake and primary processing (mixing, blending, thermal treatment, homogenisation, pasteurisation) through to secondary processing, filling, sealing, labelling, inspection, palletising, and distribution-ready end-of-line systems.

The Automation Imperative

Procurement approaches are adapting to uncertain supply chains and tariff risk, increasing interest in flexible, modular equipment and local supplier networks as companies seek to reduce exposure to international disruptions. The adoption of user-friendly automation systems responds to labour shortages and shifting skills requirements, calling for intuitive equipment interfaces and impactful operator training initiatives.

The primary packaging equipment segment accounted for the largest market revenue share in 2025, as it is directly involved in filling, sealing, wrapping, and protecting food products before distribution. Demand is shifting toward automated systems that enable higher throughput, reduced material waste, improved hygiene, and greater format flexibility.

Key Equipment Categories

Filling and capping systems are at the centre of beverage and liquid food processing investment, with volumetric, gravity, and piston-fill systems each suited to specific product viscosities and throughput requirements. The shift to sustainable packaging formats — particularly the transition from PET bottles to aluminium cans and from rigid containers to flexible pouches — is driving significant investment in new filling line configurations.

Labelling and inspection systems are experiencing accelerating investment driven by both regulatory traceability requirements and the smart packaging trend. Vision inspection systems — using high-resolution cameras and AI-driven defect recognition — are being deployed across primary, secondary, and tertiary packaging lines to detect contamination, seal failures, label errors, and fill level deviations in real time.

Clean-in-place (CIP) and sterilisation-in-place (SIP) systems are essential for dairy, beverage, and high-care food processing environments, ensuring hygienic production between runs without equipment disassembly. In February 2026, Tetra Pak announced the launch of its integrated protein and value-added dairy solutions at the 50th Dairy Industry Conference in Hyderabad, featuring the CS VS600 Bag Tipping Unit and Homogenizer 250, designed to streamline the processing and packaging of high-growth protein beverages.

Robotic palletising and end-of-line automation are being deployed at an accelerating rate across ambient, chilled, and frozen food distribution centres. Collaborative robots (cobots) are making automation accessible to mid-sized food manufacturers who cannot justify the capital expenditure of traditional industrial robotics, with payback periods in many applications now under 18 months given rising labour costs.

6. Regional Dynamics

Asia-Pacific: The Growth Engine

Asia Pacific dominated the food packaging market with a market share of 33.25% in 2025. China is a major consumer driven by frozen food demand and retail growth. India’s retail sector boom — expected to reach USD 2 trillion by 2032 — fuels packaging needs.

The APAC region is simultaneously the world’s largest packaging consumer market and its most dynamic growth market, driven by the convergence of population scale, rising incomes, rapid urbanisation, growing organised retail penetration, and accelerating food delivery infrastructure. The transition from traditional wet markets and unpackaged food consumption toward modern packaged food retail is generating structural, long-term demand for every packaging format.

Asia Pacific is expected to remain highly attractive for processing equipment due to expanding food manufacturing capacity, urbanisation, rising packaged food consumption, and investments in modern processing plants.

Europe: Regulatory Leadership and Sustainable Innovation

Europe is the global standard-setter for packaging sustainability regulation and sustainable packaging innovation. The EU’s PPWR, PFAS restrictions, Extended Producer Responsibility schemes, and deposit return systems are collectively creating the most demanding regulatory environment for packaging in the world — and driving the fastest commercial-scale adoption of sustainable packaging alternatives.

The European sustainable packaging market is set to grow from USD 87.95 billion in 2026 to USD 216.02 billion by 2035 at a 10.5% CAGR, showing strong regulatory and consumer-driven momentum. Europe’s regulatory leadership is not only transforming its domestic packaging market but is also setting the de facto global standards for multinationals who must comply with EU requirements across their entire product portfolio to maintain EU market access.

North America: Technology and Automation Leadership

North America leads globally in the adoption of advanced processing and packaging automation, AI-driven quality inspection systems, and digital traceability infrastructure. The US food industry’s investment in automation has been accelerated by persistent labour market tightness, rising minimum wages, and the ongoing impact of food safety liability concerns. North America occupies 28.1% share of the global smart packaging market in 2025, driven by high technological maturity and strong regulatory enforcement.

7. Critical Risks and Challenges

Regulatory Fragmentation and Compliance Complexity

The global packaging regulatory landscape in 2026 is characterised by increasing ambition but significant fragmentation. The EU’s PPWR sets one standard; the UK’s Plastic Packaging Tax another; US state-level Extended Producer Responsibility schemes each have different material scope and recycled content requirements; and Asian markets from Japan to India to Australia have varying and evolving packaging waste frameworks. For multinationals operating across all major markets, the compliance burden of managing packaging specifications against 20+ distinct regulatory frameworks is a significant operational cost and resource drain.

Material Transition Risk

The structural shift from conventional plastics toward recycled content, mono-material flexible structures, paper-based alternatives, and aluminium involves significant technical, operational, and commercial complexity. Not all food and beverage categories can transition packaging materials without compromising food safety — moisture barriers, oxygen transmission rates, migration thresholds, and seal integrity requirements that conventional multilayer plastics deliver reliably can be difficult to replicate in alternative materials at the same cost and performance level.

Input Cost Volatility

Raw material costs — resins, aluminium, pulp, glass cullet, and the energy required to process them — remain highly volatile. While containerboard overcapacity should theoretically lower prices, high energy costs and potential mill closures can keep floors under pricing. For packaging manufacturers operating on thin margins with long-term supply contracts, the inability to pass through rapid raw material cost increases creates significant earnings volatility.

Food Waste: The Sustainability Paradox

One of the most nuanced challenges in sustainable packaging policy is the food waste paradox: packaging that extends shelf life and reduces food waste is often more material-intensive and less recyclable than minimal packaging alternatives. Food waste generates 8–10% of global greenhouse gas emissions — a figure that in most categories significantly exceeds the emissions associated with producing and disposing of the packaging itself. Policy frameworks that prioritise packaging reduction without adequately accounting for food waste implications risk creating net negative environmental outcomes.

8. Technology and Innovation

AI-Powered Quality Inspection

Artificial intelligence is transforming packaging line quality assurance from a statistical sampling discipline to a 100% inspection capability. AI-powered vision systems deployed on high-speed packaging lines can inspect every unit for seal integrity, fill level accuracy, label placement, print quality, and foreign object contamination at production speeds impossible for human or conventional machine vision inspection. In February 2026, Syntegon announced the launch of the AIM9 high-speed inspection platform at the Pharmapack exhibition in Paris — a new modular system utilising high-resolution cameras and advanced sensors for automated visual inspection and leak detection in liquid containers, designed to maximise output while ensuring high levels of product safety and quality control.

Digital Twins and Predictive Maintenance

Digital twin technology — creating a virtual replica of physical processing and packaging equipment — is enabling food manufacturers to optimise line performance, simulate format changes, and predict maintenance requirements before equipment failure occurs. Predictive maintenance powered by IoT sensor data and machine learning is reducing unplanned downtime, extending equipment life, and lowering total cost of ownership across capital-intensive processing environments.

Biodegradable and Compostable Materials

B’Zeos raised EUR 5 million to scale seaweed-based compostable films, partnering with Nestlé on pilot applications. Biodegradable and compostable packaging materials — from PLA (polylactic acid) derived from corn starch to seaweed-based films to mycelium (fungal root) packaging — are scaling from experimental to commercial applications. The commercial challenge remains cost parity with conventional materials and the availability of adequate composting infrastructure to ensure genuine end-of-life biodegradation rather than landfill disposal.

E-Commerce Packaging Optimisation

The explosive growth of direct-to-consumer food and beverage delivery — from meal kit subscriptions to premium direct-to-door wine and spirits — is creating a distinct packaging innovation frontier. E-commerce food packaging must simultaneously deliver cold chain performance, damage protection through multiple handling stages, unboxing experience, and sustainability credentials. The intersection of these requirements is driving significant investment in insulated shipping solutions, paper-based cold chain packaging, and right-sized automated fulfilment systems that minimise void fill and packaging waste.

9. Strategic Outlook for Stakeholders

Actionable Recommendations

Design for Recyclability From Day One: As we move into 2026, the food packaging industry is entering a pivotal transition from voluntary sustainability initiatives to mandatory regulatory compliance. The key to success lies in viewing packaging not as a cost centre but as a strategic branding tool that communicates trust, transparency, and convenience to a more discerning consumer base. Companies that wait for regulatory deadlines to force packaging redesign will face compressed timelines, supply shortages of compliant materials, and premium costs for last-minute transitions.

Invest in Smart Packaging Infrastructure as a Commercial Asset: Smart packaging technology is no longer exclusively a food safety cost centre — it is a marketing, consumer engagement, and supply chain optimisation asset. QR-code-enabled consumer transparency, blockchain provenance verification, and IoT cold chain monitoring all generate data that has commercial value well beyond regulatory compliance.

Prioritise Automation Investment Now: The labour market dynamics driving packaging and processing automation investment — persistent shortages, rising minimum wages, food safety liability — are structural, not cyclical. The payback period on well-specified automation investments continues to compress as labour costs rise. Equipment operators who defer automation investment are accepting a widening competitive cost disadvantage.

Leverage the Paper Overcapacity Window: The current containerboard and cartonboard overcapacity creates a buyer’s market in paper packaging substrates. Companies accelerating their plastic-to-paper transitions in 2026 can lock in advantageous pricing and supplier terms that may not be available once capacity tightens as demand for sustainable substrates accelerates through the late 2020s.

Strategic Summary: The 2026 Packaging and Equipment Business Model

| Strategic Focus | Traditional Approach | 2026 Competitive Reality |

|---|---|---|

| Material Strategy | Optimise for cost and performance | Design for recyclability and recycled content |

| Packaging Function | Protect, contain, communicate | Protect, contain, communicate, trace and engage |

| Equipment Investment | Maximise throughput, minimise capex | Automate, digitise, and build flexibility |

| Sustainability | Annual CSR report | Regulatory compliance, consumer expectation and commercial differentiator |

| Data Strategy | Line efficiency metrics | End-to-end supply chain digital twin |

| Growth Markets | North America and Europe | Asia-Pacific and emerging market industrialisation |

10. Leading Industry Companies

| Company | Region | Strategic Focus |

|---|---|---|

| Amcor plc + Berry Global | Switzerland/USA | Following the USD 8.4 billion merger, one of the world’s largest packaging companies. Amcor operates across 212 sites in 40 countries, delivering high-performance, eco-friendly packaging across food, beverages, healthcare, and personal care. USDA Allocating USD 180 million annually to sustainability-focused R&D. |

| Tetra Pak International | Switzerland | Renowned for leadership in paper-based packaging, blending renewable resources with state-of-the-art barrier technologies. The company’s investments in bio-based materials and digital traceability mark it as a key driver of innovation and transparency in sustainable packaging. sec |

| Sealed Air Corporation | USA | Leads in high-performance protective packaging, merging advanced material science with sustainability targets. Known for innovations in lightweight, recyclable, and resource-efficient packaging, with ongoing investment in digital tracking and waste reduction. sec |

| Mondi Group | UK/Global | Leading developer of paper-based and sustainable flexible packaging solutions. Pioneer in mono-material films replacing traditional multilayer structures for food and dairy. |

| Smurfit WestRock | Ireland/USA | World’s largest paper-based packaging company following merger. Dominant in corrugated and consumer packaging across e-commerce, food, and beverage. |

| Alfa Laval | Sweden | Leading processing equipment supplier with a robust portfolio covering heat transfer, separation, and fluid handling for dairy, beverage, and food processing. |

| Tetra Laval / Sidel | Switzerland | Comprehensive beverage processing and packaging equipment. Market leader in aseptic filling systems and PET blow-moulding and filling lines. |

| Syntegon Technology | Germany | Advanced packaging and processing technology across food, confectionery, and pharma. Innovating in AI-powered inspection and hygienic system design. |

| Coesia Group | Italy | Portfolio of high-speed packaging automation companies serving tobacco, food, pharmaceutical, and consumer goods. |

| Multivac | Germany | Global leader in thermoforming packaging machines, tray sealers, and labelling systems for fresh food, meat, and dairy. |

11. Conclusion: The Path Forward

The global food and beverage packaging and equipment industry in 2026 is in the midst of the most consequential transformation in its history. The packaging formats, materials, and equipment technologies that will define the decade ahead are being shaped simultaneously by regulatory mandates, consumer demand, material science breakthroughs, and the digitalisation of the supply chain.

Sustainability is not a trend — it is the new operating context. Smart packaging is not a premium feature — it is the emerging baseline for food safety and consumer transparency. Automation is not a cost-saving option — it is the operational prerequisite for remaining competitive in a world of structural labour scarcity.

The companies that will define global food and beverage packaging through 2030 are those that design for circularity from the earliest stages of product development, invest in the digital infrastructure that transforms a passive package into an active data point, and build the processing and packaging equipment capability to operate efficiently at the intersection of sustainability compliance, food safety excellence, and consumer experience leadership.

The package is no longer just a container. In 2026, it is the most powerful touchpoint in the entire food and beverage value chain.

Related:

With rising input costs and the constant need for operational agility, investment in next-generation processing technology is now a primary driver of competitive advantage. We analyze the market landscape, capital trends, and performance benchmarks in the Global Food & Beverage Processing Equipment Industry Report 2026.

With consumer demand for transparency and functionality at an all-time high, brands are leveraging packaging as a key differentiator. We break down the emerging technologies, material advancements, and design trends defining the future of the shelf in the Global Food & Beverage Packaging Innovation Report 2026.

With producers facing mounting pressure to optimize throughput and mitigate labor challenges, the adoption of AI and robotics has moved from an operational advantage to a competitive necessity. We analyze the investment landscape, key technological hurdles, and industry-wide adoption trends in the Global AI & Robotics in the Food & Beverage Industry Report 2026.

Frequently Asked Questions (FAQ)

What is the global food and beverage packaging market size in 2026?

The global food and beverage packaging market is valued at approximately USD 525–565 billion in 2026 depending on scope, with the food packaging segment alone valued at USD 564 billion and projected to reach USD 930 billion by 2034 at a CAGR of 6.46%. The beverage packaging sub-segment is valued at approximately USD 149.7 billion in 2026. When combined with the food and beverage processing and packaging equipment market — valued at USD 118.8 billion in 2026 — the combined sector represents well over USD 700 billion in annual market value, making it one of the largest and most strategically critical industries in the global food value chain.

What is the EU Packaging and Packaging Waste Regulation (PPWR) and how does it affect the industry?

The EU’s Packaging and Packaging Waste Regulation is the most significant packaging legislation in European history and is setting the de facto global standard for sustainable packaging design. Key requirements include: all packaging sold in the EU must be recyclable by 2030; recycled content must account for 35% of plastic in non-contact-sensitive packaging by 2030; and 10% of plastic in contact-sensitive packaging. CEN’s Design for Recycling standards for plastic packaging, introduced in early 2026, have replaced over 20 national guidelines with one universal EU framework. Multinational food and beverage companies must comply across their entire EU portfolio or risk losing market access — making PPWR compliance one of the most pressing strategic priorities in the global packaging industry regardless of a company’s home market.

What is smart packaging and why is it growing so fast?

Smart packaging refers to packaging systems that go beyond passive protection and containment to actively interact with the product or communicate with stakeholders. It encompasses three broad categories: active packaging (which reacts to environmental conditions such as temperature, oxygen, or moisture), intelligent packaging (which monitors and communicates product condition through sensors, RFID tags, and freshness indicators), and connected packaging (which links the physical product to the digital world through QR codes, NFC chips, and blockchain traceability). The global active and intelligent packaging market is valued at USD 16.2 billion in 2026 and growing at a CAGR of 11%, driven by food safety imperatives, regulatory traceability requirements, cold chain management demands, and the commercial opportunity to engage consumers digitally at the point of use.

What are the most significant packaging material trends in 2026?

Four material trends are defining 2026. First, the transition from conventional multilayer plastic to mono-material flexible packaging and paper-based alternatives driven by PPWR recyclability requirements. Second, the rapid growth of aluminium cans across beverage categories as brands seek a packaging format with unimpeachable recyclability credentials. Third, the paper and fibre renaissance — driven by PFAS restrictions on paper coatings and consumer preference for natural materials. Fourth, the scaling of post-consumer recycled (PCR) content across rigid plastic formats, particularly PET bottles and HDPE containers, as mandatory recycled content requirements begin to bite in the EU and other markets.

Why is automation investment accelerating in food and beverage packaging and processing?

structural forces are driving automation investment simultaneously: labour market tightness (food manufacturing and distribution workforces are facing persistent shortages at every skill level across developed markets, driving wage inflation and unreliable throughput), food safety liability (automated systems eliminate the human contamination risk that drives the most costly and reputationally damaging food recalls), and sustainability requirements (automated systems enable tighter control of packaging material usage, reducing waste and ensuring compliance with increasingly precise recycled content and recyclability specifications). The food and beverage processing equipment market is growing at a CAGR of 6.69% through 2032, reflecting this structural investment acceleration.

Which companies lead the global food and beverage packaging market in 2026?

The global packaging market is increasingly consolidated. Following the landmark USD 8.4 billion merger of Amcor and Berry Global completed in April 2025, the combined entity is one of the world’s largest packaging companies, operating across 212 sites in 40 countries. Other major players include Tetra Pak International (leader in paper-based carton packaging for dairy and beverages), Sealed Air Corporation (protective and food safety packaging), Mondi Group (paper-based and sustainable flexible packaging), Smurfit WestRock (world’s largest paper-based packaging company), and DS Smith. In equipment, the dominant players include Tetra Laval/Sidel, Alfa Laval, Syntegon, Multivac, and Coesia Group.

What is the food waste paradox in sustainable packaging?

The food waste paradox is one of the most important and frequently overlooked dimensions of the sustainable packaging debate. Packaging that extends shelf life — oxygen barriers, MAP gas atmospheres, antimicrobial films, and hermetic seals — typically requires more material, more layers, and more complex formats that are harder to recycle. However, food waste generates 8–10% of global greenhouse gas emissions — a figure that in most food categories significantly exceeds the lifecycle emissions of even non-recyclable packaging. Policy frameworks that mandate packaging reduction without accounting for the consequent food waste increase risk creating net negative environmental outcomes. The industry’s response is to invest in smart, active packaging technologies that extend shelf life through means other than additional material — such as freshness sensors, controlled-atmosphere systems, and antimicrobial coatings — while simultaneously improving recyclability.

What is the biggest growth opportunity in food and beverage packaging over the next five years?

Three growth opportunities stand out as the most commercially significant for the 2026–2031 period. First, sustainable packaging materials and design — the transition from conventional to recyclable, recycled-content, and bio-based packaging is a structural multi-decade shift that will generate sustained investment across every material category. Second, smart and active packaging — the intelligent package market is growing at 11% CAGR, and the commercialisation of cost-effective IoT sensors, blockchain traceability, and connected packaging formats will extend smart packaging well beyond premium and high-value categories into everyday food and beverage. Third, Asia-Pacific manufacturing and processing equipment investment — the ongoing industrialisation of food manufacturing in China, India, Vietnam, Indonesia, and other rapidly growing APAC markets will generate sustained high-volume demand for processing and packaging equipment from every major global equipment supplier.

Sources and References

- Future Market Insights: Global Food Packaging Market Size & Forecast 2026–2036 — https://www.futuremarketinsights.com/reports/food-packaging-market

- Fortune Business Insights: Food Packaging Market Size, Share & Industry Report 2026–2034 — https://www.fortunebusinessinsights.com/industry-reports/food-packaging-market-101941

- Mordor Intelligence: Food and Beverage Packaging Market Size & Share 2025–2030 — https://www.mordorintelligence.com/industry-reports/food-and-beverage-packaging-market

- Future Market Insights: Global Beverage Packaging Market 2026–2036 — https://www.futuremarketinsights.com/reports/global-beverage-packaging-market

- Research and Markets: Food Processing & Packaging Equipment Market Global Forecast 2026–2032 — https://www.researchandmarkets.com/reports/5666100/food-processing-and-packaging-equipment-market

- Research and Markets: Food & Beverage Processing Equipment Market Size & Trends — https://www.researchandmarkets.com/report/food-and-beverage-processing

- Coherent Market Insights: Food and Beverage Processing Equipment Market 2026–2033 — https://www.coherentmarketinsights.com/industry-reports/food-and-beverage-processing-equipment-market

- Grand View Research: Food Packaging Equipment Market 2026–2033 — https://www.grandviewresearch.com/industry-analysis/food-packaging-equipment-market

- Global Market Insights: Active & Intelligent Packaging Market 2026–2035 — https://www.gminsights.com/industry-analysis/active-and-intelligent-packaging-market

- Fortune Business Insights: Smart Packaging Market 2026–2034 — https://www.fortunebusinessinsights.com/smart-packaging-market

- Mordor Intelligence: Sustainable Packaging Market 2026–2031 — https://www.mordorintelligence.com/industry-reports/sustainable-packaging-market

- Amcor: EU Regulatory Outlook and PPWR Packaging Sustainability 2026 — https://www.amcor.com/insights/blogs/eu-regulatory-outlook-2026

- Packaging Insights: Sustainable Packaging Trends 2026 — https://www.packaginginsights.com/news/sustainable-packaging-trends-2026-trust.html

- Fastmarkets: Global Overcapacity Transforming the Food and Beverage Packaging Market 2026 — https://www.fastmarkets.com/insights/global-overcapacity-is-transforming-the-food-and-beverage-packaging-market-chart-of-the-month/

- Virtue Market Research: Food and Beverage Packaging Market 2026–2030 — https://virtuemarketresearch.com/report/food-and-beverage-packaging-market

- Towards Packaging: Food Packaging Technology and Equipment Market 2026–2035 — https://www.towardspackaging.com/insights/food-packaging-technology-and-equipment-market-size

- Towards Packaging: Food Packaging Trends 2026 — https://millionpack.com/food-packaging-trends/

- Frontiers in Food Science: Smart and AI-Based Food Packaging Review, January 2026 — https://www.frontiersin.org/journals/food-science-and-technology/articles/10.3389/frfst.2025.1665055/full

- MarketsandMarkets: Leading Companies in Food Packaging Market — https://www.marketsandmarkets.com/ResearchInsight/food-packaging-market.asp

- Technavio: Food and Beverage Packaging Machinery Market Growth Analysis 2026–2030 — https://www.technavio.com/report/food-and-beverage-packaging-machinery-market-industry-analysis