June 9, 2026

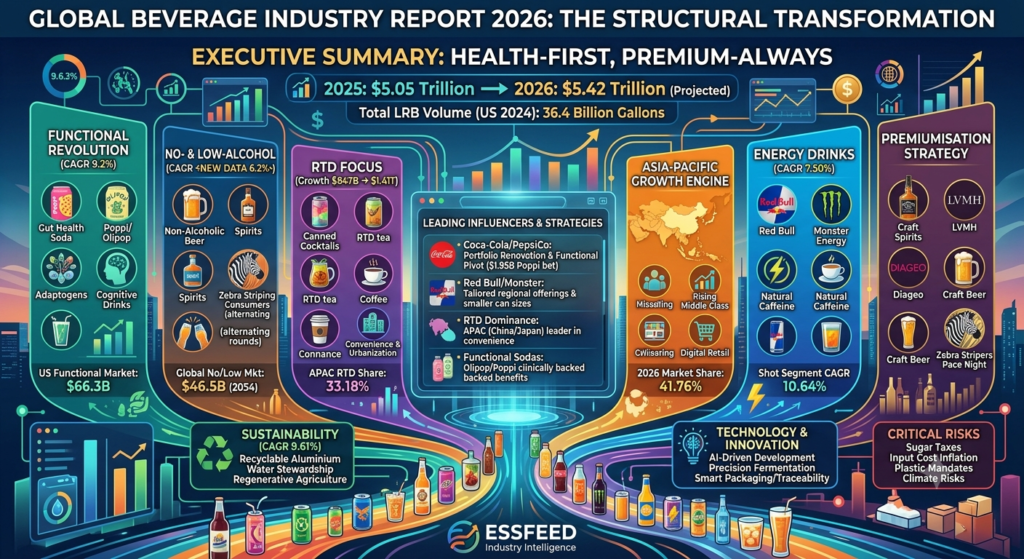

The global beverages market reached approximately $5.05 trillion in 2025 and is projected to grow to $5.42 trillion in 2026, driven by dual forces: a surging wellness movement that rewards functional and non-alcoholic drinks, and a premiumisation trend that lifts spirits and craft beverages to higher price points. Few industries touch every human being on the planet every single day. The beverage sector is one of them — and in 2026, it is undergoing the most fundamental structural transformation in its modern history.

The shift is not cyclical. It is architectural. In the US alone, total liquid refreshment beverage volume climbed to nearly 36.4 billion gallons in 2024, while retail sales rose from $247.3 billion in 2023 to $255.3 billion. Yet the real story is not in volume — it is in value, category migration, and the redefinition of what consumers want from a drink. They no longer reach for refreshment alone. They reach for function, identity, wellness, and experience.

This report provides a comprehensive analysis of the global beverage industry in 2026 — covering market size, category performance, key growth drivers, critical challenges, technology and innovation, sustainability, strategic outlook, and the leading companies defining the decade ahead.

Executive Summary: The 2026 Beverage Landscape

The beverage industry in 2026 is defined by a “health-first, premium-always” consumer mandate. Across every category — from carbonated soft drinks to spirits to bottled water — the consumer expectation has fundamentally shifted: beverages must now deliver function, clean ingredients, sustainability credentials, and a premium experience, or they face displacement by the thousands of new entrants who will.

Key Takeaways for Stakeholders:

The Functional Revolution is Mainstream: Functional beverages — drinks with specific health-oriented ingredients — are growing at a CAGR of 9.2% from 2026 to 2033. The US functional beverage market stands at $66.3 billion and is expected to grow 6.2% annually through 2029. Function is no longer a niche — it is the default consumer expectation.

No- and Low-Alcohol is Structural, Not Temporary: The global low and no-alcohol market is projected to hit USD 46.5 billion by 2034. Global alcohol volumes are projected to decline by -0.4% in 2025, with wine taking the hardest hit at -2.4%. The “sober curious” movement has matured into a permanent market reconfiguration.

RTD is the Fastest-Growing Format: The global ready-to-drink beverages market size is projected to grow from $847.69 billion in 2026 to $1,413.10 billion by 2034, exhibiting a CAGR of 6.60%. Convenience, urbanisation and on-the-go consumption patterns are structurally shifting demand away from at-home preparation formats.

Asia-Pacific is the Growth Engine: In 2026, Asia-Pacific holds the largest share of the beverage market at approximately 41.76%. China, India, and Southeast Asia are driving both volume growth and rapid premiumisation across all categories.

PepsiCo’s $1.95 Billion Signal: PepsiCo’s $1.95 billion acquisition of Poppi signals how prebiotic, low-sugar soda formats have reached mainstream relevance and created a new standard for nutrient-forward refreshment. When the world’s second-largest beverage company makes a near-$2 billion bet on a gut-health soda brand, the functional pivot is official.

Table of Contents

1. Market Overview: The 2026 Landscape

Valuation and Scale

The global beverages market size is USD 2.03 trillion in 2026, forecast to grow at a 5.65% CAGR between 2026 and 2031, reaching USD 2.67 trillion by 2031. When including all beverage categories — alcoholic and non-alcoholic, packaged and served — the total market is considerably larger. The global beverage market is projected to grow from USD 2.83 trillion in 2026 to USD 3.38 trillion by 2032, exhibiting a CAGR of 4.5% during 2026-2032. The industry is moderately fragmented, with over 1,000 organised companies operating globally alongside numerous regional and local players, though the top five players collectively account for approximately 40% share.

Category Architecture

The beverage market divides into two primary macro-categories: alcoholic and non-alcoholic. Alcoholic beverages hold a significant share of approximately 61% of the total market in 2026, though this dominance is being gradually eroded by the structural growth of non-alcoholic alternatives, functional beverages, and the no/low movement across developed markets.

Within non-alcoholic beverages, the key segments by market share in 2026 are: carbonated soft drinks (CSDs), bottled water, energy and sports drinks, ready-to-drink tea and coffee, fruit juices, and the rapidly expanding functional and health beverage segment. Within alcoholic beverages, beer remains the largest category by volume, with spirits commanding the fastest premiumisation dynamic and wine facing structural volume challenges in Western markets.

Packaging Trends

Cans are expanding at a 5.75% CAGR because of recyclability and convenience advantages, while bottles hold the dominant packaging share at approximately 59% of the market in 2026. The shift toward aluminum cans is driven by their recyclability credentials — a critical factor as sustainability mandates tighten — and by their alignment with the on-the-go RTD format preference of urban consumers.

2. Category Deep-Dives

Carbonated Soft Drinks: Reformulation or Irrelevance

Carbonated soft drinks (CSDs) remain the largest single non-alcoholic category globally, but face accelerating headwinds from health-conscious consumers and regulatory sugar taxes. The industry response has been decisive: zero-sugar and reduced-sugar reformulation is no longer an option, it is the primary growth vector. Coca-Cola’s growth engine is portfolio renovation, not constant brand creation. The company is defending mature CSD share by pushing zero-sugar deeper into the core architecture while leaning on global systems to scale hydration and RTD platforms.

The functional soda segment is the most disruptive force within the CSD space. Brands like Olipop, Poppi, and their growing roster of competitors have demonstrated that consumers will pay significant premiums — typically 2-3x the price of conventional soda — for drinks that deliver gut health benefits through prebiotic fibre, without sacrificing the carbonated experience. Olipop has invested in clinical work showing improved blood-sugar responses compared with traditional cola and continues publishing research related to digestion and metabolic performance to reinforce credibility.

Energy Drinks: The Unstoppable Category

The global energy drinks market size was valued at USD 84.03 billion in 2025, and the global market size is expected to reach USD 90.33 billion in 2026, with the market projected to reach USD 161.10 billion by 2034 at a CAGR of 7.50%.

Energy drinks are the beverage industry’s most consistently high-growth category — and in 2026, the category is being turbocharged by a critical strategic pivot: from stimulant to functional lifestyle product. Manufacturers are reformulating products using natural caffeine sources such as green coffee beans, guarana, and yerba mate, alongside reduced sugar and added micronutrients including B-complex vitamins, electrolytes, and magnesium.

Red Bull generated US sales worth approximately eight billion US dollars, while Monster Energy reported sales of around 5.8 billion US dollars. Energy drink sales reached almost 21 billion US dollars in the US in 2024. Globally, the competitive structure is clear: Red Bull leads by brand equity and global distribution; Monster leads by US market share through its Coca-Cola bottling partnership. The opportunity ahead, however, lies beyond these incumbents — in the rapidly growing Asia-Pacific market, where Asia-Pacific generated 52.62% of 2025 demand for energy drinks and the Middle East and Africa is on track for a 6.21% CAGR through 2031.

The energy shots segment is projected to grow at the fastest CAGR of 10.64% during 2026–2034, driven by compact formats, higher caffeine concentration, and rising adoption among working professionals and athletes.

Ready-to-Drink (RTD): The Format of the Decade

RTD beverages — spanning RTD coffee, RTD tea, RTD cocktails, and the broader functional and hydration RTD space — represent the single most important format shift in the beverage industry. The global non-alcoholic RTD segment was valued at $804.87 billion in 2025 and is expected to reach $1.41 trillion by 2034.

In 2025, the Asia-Pacific region commanded a dominant 33.18% share of the RTD beverages market, driven by its vast population, a burgeoning middle class, and a cultural penchant for tea. China’s RTD tea segment was significantly bolstered by domestic frontrunners like Nongfu Spring capitalising on well-established distributor networks. Meanwhile, Japan and South Korea are leading the charge in premiumisation within RTD, with products like collagen-infused coffees and hyaluronic-acid sodas tapping into the “beauty-from-within” consumer trend.

Bottled Water: The Silent Dominant

Bottled water has quietly become the most consumed packaged beverage in developed markets. US per capita bottled water consumption reached 47.3 gallons in 2024, a 2.1% increase over the prior year, cementing it as the nation’s most consumed packaged beverage. The category is bifurcating rapidly between commodity still water at the base and a fast-expanding premium segment featuring enhanced mineral water, functional water with added electrolytes, adaptogens or vitamins, and premium sparkling water. Brands like FIJI, Evian, San Pellegrino, and the challenger brand Liquid Death — which positioned water in a tallboy aluminium can with irreverent branding and grew to a billion-dollar valuation — demonstrate the extraordinary premiumisation potential within what was once a commodity category.

The No- and Low-Alcohol Revolution

Non-alcoholic beer experienced a 9% increase in volume in 2024, marking it as the fastest-growing segment within the beverage alcohol industry. The no/low movement has graduated from a niche lifestyle choice to a mainstream commercial phenomenon.

New social concepts, such as soft clubbing, are gaining traction by offering high-energy environments without alcohol. According to Eventbrite, “coffee clubbing” events alone have grown by 478%, showing how caffeine and community are replacing traditional nightlife.

The most exciting demographic for 2026 is the “Zebra Striper” — the consumer who alternates between full-strength alcohol and no/low options throughout a single night. The data confirms the scale of this shift: 78% of Gen Z now actively alternate between alcoholic and non-alcoholic rounds to pace their night. This behaviour isn’t driven by abstinence — it’s driven by longevity. They want to stay at the party longer without the hangover.

The commercial implication is profound: no/low brands that successfully engineer the sensory complexity — the mouthfeel, aroma, body, and “burn” — of their alcoholic counterparts will command the most significant loyalty and premium pricing. The category’s maturation phase, which began around 2023–2024, is now in full commercial execution.

Functional Beverages: The Wellness Revolution

Functional beverages are now firmly embedded in US consumption habits, with the vast majority of consumers buying into the category at least occasionally. The definition of “functional” has expanded dramatically beyond the original energy and sports drink paradigm.

In 2026, functional beverage subcategories include: gut health (kombucha, prebiotic and probiotic sodas), stress and mood management (adaptogen-infused teas and tonics), cognitive performance (nootropic drinks), beauty-from-within (collagen and hyaluronic acid beverages), immunity (vitamin-fortified waters), and sleep (ashwagandha and magnesium formulations).

Benefit stacking is now the expectation. Convenience and perceived time scarcity are pushing consumers towards beverages that work harder for them. Combining health, wellness and lifestyle advantages into a single beverage will be a key innovation strategy, with value measured by how many needs a drink can address at once.

The prebiotic and probiotic soda category is expected to reach $766.1 million by 2030. While this figure appears modest relative to the overall beverage market, it understates the broader functional soda momentum — a category that barely existed at commercial scale five years ago.

Alcoholic Beverages: Premiumisation Offsetting Volume Decline

Beer remains the world’s most consumed alcoholic beverage by volume, though growth in developed markets has plateaued. The craft beer movement continues to drive premiumisation and category engagement, particularly among younger consumers who prioritise provenance, flavour complexity, and local origin stories over global brand familiarity.

Spirits are the premiumisation story of the decade. Premium and ultra-premium whisky, tequila, gin, and rum commands remarkable retail price points and continues to attract disproportionate investment from the world’s largest beverage companies. LVMH’s Moët Hennessy, Diageo, Pernod Ricard, and AB InBev’s premium spirits division are all competing aggressively for shelf space and consumer preference in the $50+ bottle segment.

Wine faces the most significant structural challenge. Global alcohol volumes are projected to decline by -0.4% in 2025, with wine taking the hardest hit at -2.4%. A combination of the sober curious movement, competition from premium spirits, changing millennial and Gen Z drinking occasion preferences, and climate-driven vintage quality variability is creating a difficult operating environment for wine producers globally.

3. Key Growth Drivers

Urbanisation and the RTD Lifestyle

As of 2024, 57.3% of the global population lived in urban areas, creating enormous demand for convenient, ready-to-drink formats that fit fast-paced routines. This urbanisation megatrend underpins growth across every beverage subcategory, from bottled water to functional drinks to RTD cocktails.

Urban consumers — particularly in megacities across Asia, Africa, and Latin America — are shifting consumption away from home-prepared beverages toward packaged formats purchased from convenience stores, vending machines, and delivery platforms. This structural shift creates tailwinds for every segment of the packaged beverage market.

The Health and Wellness Megatrend

According to the 2026 What’s Hot Culinary Forecast, the shift in consumer behavior is being driven by a desire for healthier, more functional benefits that go beyond basic hydration or refreshment. This is especially true for Gen Zs and Millennials, who say they want alternatives that meet those expectations, including alcohol-free beers and CBD-infused beverages.

The wellness megatrend is not a passing consumer preference — it is a generational value shift. Younger consumers have grown up with unprecedented access to nutritional information, health tracking technology, and social media content from health and wellness influencers. For this cohort, every purchase decision — including beverages — is filtered through a health lens. Products that cannot articulate a functional or wellness benefit are structurally disadvantaged in competing for their spending.

Asia-Pacific Middle Class Expansion

Asia Pacific is the fastest-growing region, with the segment valued at $480 billion in 2025 and projected to surpass $983 billion by 2035, growing at a CAGR of 7.44%. The region’s growth is driven by urban youth populations, high health consciousness, and rapidly expanding digital retail infrastructure.

India deserves particular emphasis as an emerging beverage powerhouse. With a population of 1.4 billion, a rapidly growing middle class, a young demographic profile, and accelerating organised retail penetration, India is on a trajectory to become one of the top three global beverage markets before 2030. The transition from traditional chai and lassi consumption toward packaged RTD formats is creating structural demand for virtually every beverage category.

Digital Commerce and Direct-to-Consumer

The US generates the most eCommerce beverage revenue worldwide, with a projected $110.48 billion in 2025. E-commerce has fundamentally disrupted the traditional beverage distribution model. Direct-to-consumer subscription models — pioneered by brands like Athletic Brewing Company (no/low), Olipop, and a growing roster of functional beverage challengers — allow emerging brands to build loyal consumer bases and generate recurring revenue without the need for traditional retail distribution, fundamentally lowering the barrier to market entry and creating a pipeline of well-capitalised challenger brands that incumbent beverage companies must either acquire or compete against.

4. Critical Risks and Challenges

Sugar Taxes and Regulatory Headwinds

The global regulatory environment for sugar-sweetened beverages continues to tighten. Sugar taxes — already implemented in the UK, Mexico, South Africa, and dozens of other markets — are expanding geographically and increasing in rate. For producers of high-sugar CSDs, juices, and sports drinks, these taxes represent both a direct cost increase and a signal that reformulation is not optional.

The reformulation challenge is technically significant: removing sugar from a beverage while maintaining the same taste profile, mouthfeel, and consumer satisfaction requires sophisticated flavour science and ingredient substitution. Brands that can deliver zero-sugar or low-sugar reformulations without consumer-detectable quality degradation will protect market share; those that cannot will face ongoing volume pressure.

Input Cost Inflation and Supply Chain Volatility

Commodity costs — sugar, coffee, aluminium, PET resin, orange juice, and cocoa — remain elevated relative to pre-2020 levels and subject to weather-driven volatility, geopolitical supply chain disruptions, and currency translation risks for multinationals operating across dozens of markets. Nestlé plans to reduce its workforce by 16,000 roles, representing about 6% of global employees, and aims to reach $3.8 billion in cost reductions by 2027 as part of a larger plan to improve speed. Heineken is taking a related approach as it removes 400 head-office roles under its Evergreen 2030 strategy. These restructuring programs reflect the industry-wide imperative to reduce structural costs in an environment of persistent input inflation.

Plastic Packaging and Sustainability Mandates

The global beverage industry is the world’s largest producer of single-use plastic packaging, making it a prime target for environmental regulation and consumer activist pressure. The EU’s Single-Use Plastics Directive, extended producer responsibility schemes, and plastic tax proposals across dozens of markets are forcing the industry to accelerate the transition toward recycled content, recyclable formats, and reduced packaging volumes. The global beverage packaging market is projected to grow from USD 175.19 billion in 2025 to USD 300.25 billion by 2035, with sustainable packaging and smart packaging technologies driving the fastest growth segments.

Health Claim Credibility and Regulatory Scrutiny

As the functional beverage market has exploded, so has regulatory scrutiny of health claims. In the EU, the UK, and increasingly in the US, food and beverage health claims must be substantiated by clinical evidence — a requirement that raises the cost and complexity of bringing functional beverages to market. Brands making claims that outpace their clinical evidence face both regulatory action and consumer backlash as transparency demands increase. As cleanliness and function continue to shape consumer expectations, companies will need clear validation for their claims and packaging that accurately conveys benefits.

Water Scarcity and Climate Risk

The beverage industry is inherently water-intensive — every litre of bottled water, beer, soft drink, or juice requires significantly more than one litre of water in production, including agricultural inputs. Climate-driven water scarcity in key production regions — from Californian vineyards to Indian tea estates to Brazilian coffee farms — represents a long-term structural risk to ingredient supply and production costs. The industry’s largest operators are investing heavily in water stewardship programs, but the underlying physical risk of reduced water availability in key growing regions is non-negotiable.

5. Technology and Innovation

AI-Driven Product Development

Artificial intelligence is transforming beverage product development from an art-form guided by flavour scientists and market researchers into a data-driven discipline capable of predicting consumer preference before a single product is manufactured. Major beverage companies are deploying AI tools that analyse flavour compound combinations, social media flavour trend data, regional taste preferences, and ingredient cost optimisation simultaneously — compressing product development timelines from 18 months to as few as six months.

AI-driven product development, plant-based proteins, and convenient urban formats are speeding up new product launches across the industry, creating both opportunities for rapid innovation and risks of market fragmentation as the category count expands faster than consumer attention can absorb.

Precision Fermentation and Novel Ingredients

Precision fermentation technology — using engineered microorganisms to produce specific bioactive compounds — is enabling the commercial-scale production of functional ingredients that were previously too expensive or too difficult to source from natural inputs. This technology is particularly impactful in the functional beverage space, where ingredients like rare adaptogens, specific probiotic strains, and targeted flavour compounds can now be produced consistently at commercial scale.

Gen Z, in particular, is opting for mushroom-based wellness shots and tonics over coffee or alcohol for mental clarity and a sense of calm energy. Ashwagandha, L-theanine and rhodiola are gaining traction because they’re associated with stress moderation and improved concentration. Precision fermentation enables consistent, high-purity production of these and other functional ingredients at the scale required for mass-market beverage applications.

Smart Packaging and Traceability

Smart packaging technology — incorporating QR codes, NFC chips, and blockchain-based provenance tracking — is enabling beverage brands to create interactive consumer experiences while simultaneously building the supply chain transparency demanded by regulators and sustainability-focused consumers. A consumer scanning a QR code on a premium water bottle can access the source spring’s water quality data in real time; a wine drinker can trace the precise vineyard, vintage conditions, and production process behind every bottle.

Sustainable Packaging Innovation

Sustainable packaging innovations, including recyclable aluminium cans, bio-based PET bottles, and glass options, appeal to environmentally aware buyers and support regulatory pushes for eco-friendliness. Beyond these well-established formats, the industry is investing in genuinely novel solutions: plant-based bottles made from sugarcane PET, edible packaging for portion-controlled beverage concentrates, and refillable container systems that leverage digital tracking to incentivise consumer return behaviour.

6. Sustainability: The Industry’s Defining Imperative

The beverage industry’s sustainability challenge is significant and multidimensional. It encompasses packaging waste, water consumption, agricultural supply chain sustainability, carbon emissions from production and distribution, and the social welfare of smallholder farmers who produce key ingredients including coffee, tea, cocoa, and sugar.

Sustainability is reshaping drink manufacturing, with PepsiCo, Mars, Heineken, Nestlé, Asahi, Starbucks, AB InBev, Coca-Cola, Danone and Suntory leading. From carbon reduction and water stewardship to circular packaging and regenerative agriculture, companies are reshaping how products are sourced, produced and distributed.

The sustainable beverage segment itself is growing at a remarkable pace. The sustainable beverage market is projected to grow from USD 1,062.89 billion in 2026 to USD 2,215.02 billion by 2034, exhibiting a CAGR of 9.61% during the forecast period. This growth reflects both the increasing share of sustainably-produced beverages within existing categories and the emergence of new categories — such as regenerative agriculture-certified coffee and biodynamic wine — where sustainability credentials are the primary value proposition.

7. Strategic Outlook for Stakeholders

The beverage industry in 2026 rewards operators who can deliver health credentials, premium experiences, and sustainability validation simultaneously — at scale. The era of competing purely on distribution reach and advertising spend is over for all but the largest incumbents, and even they are investing heavily in portfolio renovation to stay relevant to a rapidly evolving consumer.

Actionable Recommendations

Embed Functionality into Existing Portfolios: The most capital-efficient route to functional relevance is renovating existing mainstream brands — adding prebiotic fibre to a CSD, electrolytes to a water brand, adaptogens to an iced tea — rather than building entirely new functional sub-brands. This is the playbook PepsiCo’s beverage strategy demonstrates: functional cues are being embedded where distribution already exists, rather than being isolated in niche brands, which lowers innovation risk and increases the odds that “better-for-you” translates into real shelf velocity.

Invest in the No/Low Infrastructure: Brands in the alcoholic beverage space that have not yet made serious investment in no/low alternatives are falling behind a wave that will not reverse. The infrastructure investment required — recipe development, separate production lines, regulatory compliance, consumer education — takes time, and brands that begin now will be significantly better positioned for 2028–2030 when no/low volumes are projected to approach double-digit market share in developed markets.

Build Asia-Pacific Capability Before the Window Closes: The APAC beverage opportunity is enormous but intensely competitive. Domestic players — particularly in China, India, and Southeast Asia — are building category leadership with the speed and local consumer insight that international brands struggle to match. Partnerships, acquisitions, or localised manufacturing are more reliable routes to sustainable APAC market share than export-led or purely marketing-led approaches.

Prioritise Packaging Transition Now: The regulatory and consumer pressure on single-use plastic packaging will only intensify. Companies that have not already mapped their packaging transition roadmaps and begun commercial-scale pilots of alternative formats are behind the curve. Early movers in sustainable packaging will benefit from first-mover brand equity advantages that will be difficult to replicate once competitors catch up.

Strategic Summary: The 2026 Beverage Business Model

| Strategic Focus | Traditional Model | 2026 Competitive Reality |

|---|---|---|

| Product Value | Taste and refreshment | Function, wellness and identity |

| Target Consumer | Mass market demographics | Values-led psychographic segments |

| Growth Strategy | Distribution and advertising | Portfolio renovation and functional innovation |

| Sustainability | CSR report line item | Commercial differentiator and license to operate |

| Format Priority | Large-format retail | RTD, DTC, convenience and digital channels |

| Revenue Model | Volume-led, commodity pricing | Premium pricing via functional and provenance claims |

8. Leading Industry Influencers

| Company | Region | Strategic Focus |

|---|---|---|

| The Coca-Cola Company | Global | Portfolio renovation — defending CSD share via zero-sugar while scaling hydration and RTD platforms through global distribution systems. |

| PepsiCo | Global | Portfolio diversification and functional claim modernisation. The $1.95B acquisition of Poppi anchors prebiotic cola as a mainstream format. |

| Nestlé | Global | Top sustainable drink manufacturer, integrating environmental and social responsibility across water and beverage operations. Leading in coffee through Nespresso and Nescafé platforms. |

| AB InBev | Global | World’s largest brewer investing aggressively in no/low alcohol across its Corona, Stella Artois, and Budweiser brands. No/low now a stated strategic priority. |

| Red Bull GmbH | Austria/Global | Energy drinks market leader. Tailoring product offerings to regional preferences, introducing smaller can sizes and lower-sugar variants in key APAC markets. |

| Diageo | UK/Global | Premium spirits powerhouse. Johnnie Walker, Guinness, Tanqueray. Leading investment in no/low spirits alternatives and RTD cocktail formats. |

| Keurig Dr Pepper | USA | Major player in North America combining soft drinks with coffee systems, Wikipedia with a growing portfolio of functional and premium beverages. |

| Olipop / Poppi | USA | The disruptor generation — functional prebiotic sodas that forced the industry’s largest operators to either acquire or compete directly. |

9. Conclusion: The Path Forward

The global beverage industry in 2026 is at the most exciting and consequential inflection point in its modern history. The fundamental drivers — population growth, urbanisation, rising incomes, and the universal human need for hydration — provide an unassailable foundation for long-term growth. But within that growth story, the categories, formats, and value propositions that will capture the most dynamic share are undergoing rapid and permanent transformation.

Function will replace refreshment as the primary consumer motivation. No/low will continue its structural displacement of traditional alcoholic formats. RTD will absorb an ever-larger share of consumption occasions from home-prepared alternatives. Asia-Pacific will become the undisputed centre of global beverage volume growth. And sustainability will transition from a marketing credential to a regulatory baseline.

The companies that will define the next decade of global beverage are not necessarily those with the largest distribution networks or the most established brand equities — though these remain formidable advantages. They are those with the clearest understanding of the health-first consumer, the most agile innovation capability, and the most credible sustainability commitments. The race to redefine what the world drinks has never been more open — or more consequential.

Related:

From the evolution of artisanal craft spirits to the digital transformation of alcohol retail, we break down the most significant trends shaping the industry in the Global Alcohol Industry Market 2026 Report.

As consumers pivot toward functional hydration and ‘clean label’ nutrition, the juice and smoothie sector is undergoing a shift toward cold-pressed innovation and high-density, nutrient-rich formulations. Explore the key trends and market dynamics shaping the industry in our Global Juice & Smoothies Industry Report 2026.

With shifting consumption habits and the rapid expansion of the ‘ready-to-drink’ segment, manufacturers and traders are navigating a dynamic global landscape. We analyze the critical supply chain bottlenecks, pricing trends, and future growth projections in our Global Coffee & Tea Industry Report 2026.

From energy-boosting botanicals to gut-health-focused elixirs, we analyze the key market drivers and emerging product categories in the Global Functional & Nutritional Drinks Industry Report 2026.

What is the size of the global beverage industry in 2026?

The global beverage industry is valued at approximately $2.03 trillion to $2.83 trillion in 2026, depending on the scope of measurement — with estimates varying based on whether they include all alcoholic and non-alcoholic categories, packaging, and distribution. The broader total market including all beverage segments is projected at $5.42 trillion when including on-premise and foodservice consumption. The market is growing at a CAGR of approximately 4.5–5.65% through 2031, driven by functional beverages, RTD formats, premiumisation, and Asia-Pacific demand expansion.

What are the fastest-growing beverage categories in 2026?

Three categories stand out as the fastest-growing in 2026. First, functional beverages — growing at a CAGR of 9.2% through 2033 — driven by gut health drinks, adaptogens, nootropics, and wellness-oriented formulations. Second, the no- and low-alcohol segment, which grew volume 9% in 2024 alone and is projected to reach USD 46.5 billion by 2034. Third, ready-to-drink (RTD) beverages across all formats, growing at a CAGR of 6.6% from 2026 to 2034. Energy drinks are also a consistent high-growth category, projected to reach USD 161 billion by 2034 from USD 90 billion in 2026.

Why is the no- and low-alcohol movement growing so rapidly?

The no/low movement is being driven by three converging forces. First, a generational shift — 78% of Gen Z now actively alternate between alcoholic and non-alcoholic drinks on a single occasion, not because they are abstaining but because they want to pace themselves and avoid hangovers. Second, product quality has improved dramatically — modern no/low beers, wines, and spirits now deliver the sensory complexity — mouthfeel, aroma, body — that earlier generations of alcohol-free products lacked. Third, new social formats like “soft clubbing” and “coffee clubbing” are creating alcohol-free social occasions that legitimise the choice. The result is a structural market shift rather than a passing wellness trend.

Which region is driving the most beverage industry growth in 2026?

Asia-Pacific is the dominant growth engine, accounting for approximately 39–42% of global beverage market share in 2026 and growing faster than any other region. China is the world’s largest market for alcoholic beverages, generating more than $335 billion in annual revenue. India is the fastest-growing major market, driven by its 1.4 billion population, rising middle class, and expanding organised retail. Southeast Asia — particularly Vietnam, Indonesia, and the Philippines — is seeing rapid RTD and functional beverage adoption driven by urbanisation, heat-climate hydration demand, and an expanding convenience store infrastructure. The Asia-Pacific functional beverage segment alone is projected to grow from $480 billion in 2025 to over $983 billion by 2035.

What does “functional beverage” mean and why is it important in 2026?

A functional beverage is a drink that delivers specific health or wellness benefits beyond basic hydration, through the addition of active ingredients such as vitamins, minerals, probiotics, prebiotics, adaptogens, electrolytes, amino acids, or plant extracts. In 2026, the functional beverage category has expanded far beyond its original energy drink and sports drink roots to encompass gut health drinks (kombucha, prebiotic sodas like Olipop and Poppi), stress and mood management (adaptogen-infused teas and tonics with ashwagandha, lion’s mane, rhodiola), cognitive performance (nootropic drinks), beauty-from-within (collagen and hyaluronic acid beverages), and sleep support (magnesium and ashwagandha formulations). The US functional beverage market alone stands at $66.3 billion in 2026, growing at 6.2% annually. The importance lies in the consumer mindset shift: beverages are no longer just refreshment — they are a daily wellness delivery mechanism.

What is the biggest challenge facing the global beverage industry?

There is no single biggest challenge — rather, a confluence of structural pressures that are most acute simultaneously in 2026. Sugar taxes and health regulations are forcing reformulation across the CSD and juice categories. Plastic packaging mandates are requiring billions in capital investment for packaging transitions. Input cost inflation — driven by climate-affected agricultural commodities including coffee, orange juice, sugar, and cocoa — is squeezing margins. Water scarcity in key production regions creates long-term supply risk. And the pace of consumer preference change — driven by social media, wellness culture, and the democratisation of nutritional information — means that product cycles are compressing, creating both innovation opportunity and the risk of rapid brand obsolescence for companies that move slowly.

Who are the largest beverage companies in the world in 2026?

The global beverage market is dominated by a small number of very large multinationals who collectively account for approximately 40% of total market share despite competing in a market of over 1,000 organised companies. The Coca-Cola Company is the world’s largest non-alcoholic beverage company, with Coca-Cola Zero Sugar and its RTD and hydration platforms driving current growth. PepsiCo is the second-largest, distinguished by its simultaneous food and beverage portfolio and its landmark $1.95 billion acquisition of Poppi in 2026. Nestlé is the world’s largest food and beverage company overall, with strength in coffee (Nespresso, Nescafé), bottled water, and health-nutrition beverages. AB InBev is the world’s largest brewer. Diageo leads in premium spirits. Red Bull and Monster dominate the global energy drinks category. Among challenger brands, Olipop, Athletic Brewing, and Liquid Death represent the most commercially significant disruptors of the current cycle.

How is sustainability reshaping the beverage industry?

Sustainability has moved from a CSR credential to a commercial prerequisite and regulatory compliance requirement for the beverage industry. The three most significant sustainability pressures in 2026 are packaging (governments mandating recycled content, deposit return schemes, and plastic tax), water stewardship (beverage companies are among the world’s largest commercial water users and face growing scrutiny in water-stressed regions), and agricultural supply chain sustainability (carbon footprints from sugar, coffee, cocoa, and other commodity inputs). The sustainable beverage market — beverages made, packaged, and distributed with environmental responsibility — is projected to grow from USD 1.06 trillion in 2026 to USD 2.21 trillion by 2034 at a CAGR of 9.61%, making sustainability not just an ethical imperative but the industry’s highest-growth commercial segment.

What will the global beverage industry look like by 2030?

By 2030, the global beverage market is projected to reach approximately $2.30 trillion in packaged beverages, with the broader total market approaching $9.6 trillion by 2033. The functional beverage segment will have moved from premium niche to mainstream baseline expectation — drinks without functional credentials will struggle for relevance in developed markets. The no/low alcohol segment will command double-digit market share in the UK, Germany, Australia, and the US. Asia-Pacific will have cemented its position as the world’s dominant beverage growth engine, with India potentially overtaking the US as the second-largest single market. RTD formats will have displaced traditional at-home preparation in a growing number of occasion categories. And sustainability — in packaging, sourcing, and production — will have transitioned from a differentiator to the minimum entry standard for premium channel access globally.

Sources and References

- Mordor Intelligence: Global Beverages Market Size, Share & Industry Report 2026–2031 — https://www.mordorintelligence.com/industry-reports/beverages-market

- MarkNtel Advisors: Beverage Market Share, Growth Drivers & Forecast 2026–2032 — https://www.marknteladvisors.com/research-library/beverage-market-report.html

- Knowledge Sourcing Intelligence: Global Beverage Market Insights & Forecasts 2025–2030 — https://www.knowledge-sourcing.com/report/global-beverage-market

- Revenue Memo: Beverage Industry Statistics 2026 — https://www.revenuememo.com/p/beverage-industry-statistics

- Fortune Business Insights: Energy Drinks Market Size, Share & Industry Report 2026–2034 — https://www.fortunebusinessinsights.com/energy-drinks-market-112182

- Mordor Intelligence: Energy Drinks Market Report 2026–2031 — https://www.mordorintelligence.com/industry-reports/energy-drinks-market

- Fortune Business Insights: Ready-to-Drink Beverages Market 2026–2034 — https://www.fortunebusinessinsights.com/ready-to-drink-rtd-beverages-market-102124

- Mordor Intelligence: Ready-to-Drink Beverages Market 2026–2031 — https://www.mordorintelligence.com/industry-reports/ready-to-drinks-beverages-market

- Clarkston Consulting: 2026 Beverage Industry Trends — https://clarkstonconsulting.com/insights/2026-beverage-industry-trends/

- Tastewise: Top CPG Beverage Companies 2026 — https://tastewise.io/blog/best-cpg-beverage-companies

- BevSource: 2026 Beverage Trends: The Flavours, Functions and Forces — https://www.bevsource.com/news/beverage-trends-2026

- Good Culture Ingredients: Non-Alc Trends 2026 — https://www.goodcultureingredients.com/blog/consumption-habits-non-alc-trends-2026

- Botrista: 2026 Drink Trends — https://botrista.com/resources/blog-post/2026-drink-trends-non-alcoholic-beverages-nostalgic-comfort/

- National Restaurant Association: What’s Hot 2026 Culinary Forecast — https://restaurant.org/education-and-resources/resource-library/whats-hot-in-2026-healthier-functional-beverages/

- Fortune Business Insights: Sustainable Beverage Market 2026–2034 — https://www.fortunebusinessinsights.com/sustainable-beverage-market-115388

- Food & Drink Digital: Top 10 Sustainable Drinks Manufacturers — https://fooddigital.com/top10/top-10-sustainable-drinks-manufacturers

- Attest: Functional Beverage Market Key 2026 Trends — https://www.askattest.com/blog/research/fueled-up-how-energy-became-the-must-have-benefit-in-functional-beverages

- Pinky Beverages: Non-Alcoholic Beverage Trends 2026 — https://pinkybeverages.com/non-alcoholic-beverage-trends-2026/

- Business Stats: Energy Drinks Worldwide 2026 — https://businesstats.com/energy-drinks-worldwide/