June 9, 2026

The global cold chain market is estimated at USD 276.5 billion in 2026 and is projected to reach USD 455.0 billion by 2031, registering a CAGR of 10.5% during the forecast period. The broader cold chain logistics market — encompassing temperature-controlled warehousing, refrigerated transportation, cold chain monitoring, and specialised pharmaceutical logistics — is valued at USD 496.80 billion in 2026 and is projected to grow to nearly USD 1.48 trillion by 2035 at a CAGR of 12.97%. Grand View Research places the cold chain market at USD 437.49 billion in 2026, growing at a CAGR of 20.5% through 2033.

The cold chain is not a logistics sub-sector. It is a foundational infrastructure of modern civilisation. Every fresh strawberry, every vaccine dose, every carton of milk, every biological therapy, every frozen meal, and every mRNA-based medicine that reaches a consumer, patient, or healthcare worker in the condition required for safety and efficacy does so because of an unbroken chain of refrigerated warehouses, temperature-controlled transport, continuous monitoring systems, and the tens of thousands of logistics professionals who maintain them. When the cold chain fails — a power outage at a warehouse, a reefer unit malfunction on a truck, a temperature excursion during a vaccine distribution campaign — the consequences range from financial losses and food waste to spoiled life-saving medicines and preventable deaths.

In 2026, the global cold chain industry is navigating the most transformative period in its history — compressed by extraordinary growth drivers on multiple fronts simultaneously. The explosive expansion of biologics, mRNA vaccines, and gene therapy medicines is creating pharmaceutical cold chain demand at temperature ranges previously confined to research laboratories. The global proliferation of online grocery, quick commerce, and meal kit delivery is extending the cold chain to the consumer’s doorstep. Regulatory frameworks including the US FDA’s FSMA and the Drug Supply Chain Security Act are mandating digital traceability at unprecedented granularity. And artificial intelligence, IoT sensor networks, and automation are transforming cold chain operations from reactive management to predictive, preventive systems.

This report provides the most comprehensive publicly available analysis of the global cold chain industry in 2026 — covering market scale, the food and beverage cold chain, the pharmaceutical cold chain revolution, technology and innovation, infrastructure and automation, regulatory landscape, sustainability, regional dynamics, key challenges, strategic outlook, and leading companies.

Executive Summary: The 2026 Cold Chain Landscape

The global cold chain industry in 2026 is defined by a single strategic imperative: build, automate, and digitalise faster than demand is growing — which is itself growing faster than at any point in the industry’s history.

Key Takeaways for Stakeholders:

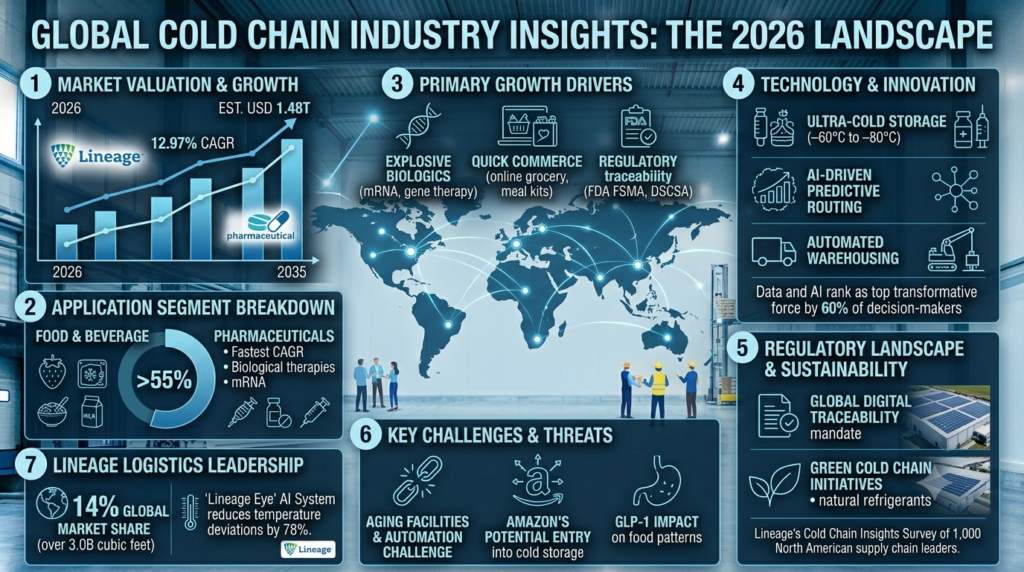

The global cold chain market is valued at USD 276.5–496.8 billion in 2026, depending on scope, growing at a CAGR of 10.5–20.5% toward USD 455 billion to USD 1.48 trillion by 2031–2035.

Food and beverages dominate with over 55% of cold chain market share, but pharmaceuticals is the fastest-growing segment, driven by the biological medicine revolution.

Lineage Logistics commands over 14% global market share with more than 3.0 billion cubic feet of storage, having transitioned from a real estate play to a technology platform through its “Lineage Eye” AI system that has reportedly reduced temperature deviations by 78% in pilot facilities.

60% of supply chain decision-makers rank data and AI among the top transformative forces in 2026, according to Lineage’s Cold Chain Insights Survey of 1,000 North American supply chain leaders.

The industry is navigating a “Mega-Reefer” consolidation wave — moving away from fragmented regional providers toward integrated operators that combine AI-driven predictive routing, automated sub-zero warehousing, and end-to-end visibility platforms.

mRNA vaccines and biologics are creating ultra-cold requirements at −60°C to −80°C that require entirely new cold chain infrastructure investment, driving the pharmaceutical cold chain to the fastest CAGR of any application segment.

Amazon’s potential entry into cold storage is identified by Lineage’s CEO as one of the three most significant threats to the industry over the next five years — alongside the GLP-1 impact on food consumption patterns and the challenge of automating ageing facilities.

Table of Contents

1. Market Overview: Scale, Structure and Scope

Defining the Cold Chain

The cold chain encompasses every infrastructure, system, technology, and process required to maintain temperature-sensitive products within their specified temperature range from the point of origin to the point of consumption or use. It is most commonly segmented into two primary components: cold storage (refrigerated warehousing, cold rooms, freezer facilities, and controlled atmosphere storage) and refrigerated transportation (reefer trucks, refrigerated rail wagons, reefer containers, temperature-controlled air cargo, and last-mile refrigerated delivery).

Temperature ranges within the cold chain are defined by the products they serve:

- Room temperature / ambient: 15°C–25°C for heat-sensitive products not requiring active refrigeration

- Cool chain: 8°C–15°C for fresh produce, some flowers, and certain chemicals

- Chilled: 0°C–4°C for fresh meat, dairy, and short shelf-life prepared foods

- Refrigerated: 2°C–8°C for most vaccines, insulin, and temperature-sensitive pharmaceutical products

- Frozen: −18°C to −25°C for frozen food, ice cream, and plasma products

- Ultra-cold / cryogenic: −60°C to −90°C for mRNA vaccines, advanced biologics, and gene therapies

Global Market Valuation

The global cold chain market is estimated at USD 276.5 billion in 2026 by MarketsandMarkets, growing to USD 455.0 billion by 2031 at a CAGR of 10.5%. Precedence Research’s cold chain logistics market estimate is significantly higher at USD 496.80 billion in 2026, projected to reach USD 1.48 trillion by 2035 at a CAGR of 12.97%. Grand View Research estimates the broader cold chain market at USD 437.49 billion in 2026, growing at a CAGR of 20.5% through 2033. The wide range of estimates reflects differences in scope: narrower definitions focus on cold storage and refrigerated transport, while broader definitions include cold chain monitoring technology, packaging, pharmaceutical logistics, and the full spectrum of temperature-controlled supply chain services.

The cold chain storage segment dominated the overall market with a revenue share of 51.8% in 2025, while refrigerated transportation accounted for approximately 48%. The frozen temperature segment dominated by volume, but the chilled segment is projected to experience the highest growth rate between 2026 and 2035 as fresh, minimally processed food demand grows.

The cold chain packaging market — encompassing insulated containers, gel packs, dry ice, phase-change materials, and vacuum insulation panels — is valued at USD 38.15 billion in 2026, growing at an 11.3% CAGR toward USD 100 billion by 2035.

Industry Structure

The global cold chain industry is moderately consolidated at the top, with a small number of very large operators commanding significant market share through their capital-intensive warehouse infrastructure and technology platforms, while thousands of regional and specialist operators serve niche markets. Lineage Logistics and Americold collectively control a majority of national refrigerated warehouse cubic footage in the United States, creating a quasi-duopoly in many metropolitan markets. Globally, the industry is moving away from fragmented regional providers toward “Mega-Reefer” operators that integrate AI-driven predictive routing, automated sub-zero warehousing, and end-to-end visibility platforms.

2. The Food and Beverage Cold Chain: The Sector’s Foundation

Market Scale and Dominance

Food and beverages represent the largest application segment of the global cold chain, accounting for over 55% of total market value. Within food and beverage cold chain, the dairy and frozen desserts segment commanded the largest revenue share of 36.10% in 2025, followed by fresh meat and poultry, fresh produce, and seafood. The food and beverage cold chain encompasses the full journey of perishable food from farm or processing plant through distribution centre, retailer, and increasingly, home delivery.

Cold chain contributes nearly 40% to the food and beverage logistics market, where fresh produce, dairy, meat, and frozen goods require controlled transport and storage. The global Top 25 cold storage capacity reached 7.76 billion cubic feet in 2026, up 6.3% year over year, with Latin America leading regional growth at 8.6% — driven by Brazil’s dominant position as a global protein exporter requiring extensive cold chain infrastructure for beef, poultry, and seafood export.

The Fresh Food and Quick Commerce Revolution

The explosion of online grocery, quick commerce, and meal kit delivery is fundamentally expanding the cold chain’s scope. E-grocery platforms — particularly in the US and Asia — are capturing a growing share of food retail and depend on reliable cold chain logistics that extends all the way to the consumer’s doorstep. The 15–30 minute grocery delivery promise of quick commerce platforms requires a network of dark stores with cold chain capability positioned within urban neighbourhoods, creating entirely new cold chain infrastructure requirements.

The challenge of last-mile cold chain — maintaining temperature-controlled conditions for individual consumer deliveries, in urban environments, at the speed required by quick commerce — is the most technically and economically demanding new frontier in food cold chain logistics. It requires refrigerated delivery vehicles (increasingly electric), insulated delivery packaging that maintains temperature during the final mile without continuous active refrigeration, and real-time monitoring that provides documentary evidence of temperature compliance to regulatory standards.

Food Waste Reduction as a Cold Chain Value Proposition

Globally, approximately one-third of all food produced for human consumption — an estimated 1.3 billion tonnes annually — is lost or wasted. A significant proportion of this waste occurs because of cold chain failures: inadequate refrigeration in developing markets allows fresh produce, meat, and dairy to spoil before reaching consumers; temperature excursions during transport degrade quality and reduce shelf life; and poor inventory management results in food remaining in cold storage past its optimal quality window.

The commercial case for cold chain investment in developing markets is therefore simultaneously economic and humanitarian. A cold chain dollar invested in emerging market food cold chain infrastructure can generate returns measured not just in commercial logistics revenue, but in reduction of food waste, improvement in food security, reduction in post-harvest loss, and improvement in nutritional outcomes for populations dependent on the preserved quality of protein and fresh food.

3. The Pharmaceutical Cold Chain: The Industry’s Fastest-Growing Frontier

The Biologics and mRNA Revolution

The pharmaceutical cold chain is growing faster than any other application segment within the cold chain market, driven by the biological medicine revolution that is reshaping human healthcare. The pharmaceuticals segment is expected to grow at the fastest CAGR of any cold chain application, with the global cold chain monitoring market for pharmaceuticals growing at a remarkable 24.52% CAGR through 2034.

The core driver is the extraordinary expansion of biologic medicines — therapeutic proteins, monoclonal antibodies, vaccines, gene therapies, cell therapies, and RNA-based medicines — that require continuous cold chain management from manufacturing through to patient administration. Unlike conventional small-molecule pharmaceuticals that are chemically stable at ambient temperatures, biologics are large, complex protein or nucleic acid molecules that degrade rapidly when exposed to temperatures outside their specified ranges.

mRNA vaccines — exemplified by the COVID-19 vaccines that demonstrated the commercial and public health potential of the technology platform — require ultra-cold storage conditions of −60°C to −80°C that exceed the capabilities of conventional pharmaceutical cold chain infrastructure. This has driven significant global investment in ultra-cold warehousing and transportation capacity. Subsequent mRNA medicines in development for influenza, RSV, cancer therapy, and rare diseases will sustain this ultra-cold infrastructure demand beyond any individual vaccine campaign.

WHO 2025 Guidelines and the New Standard

The WHO’s 2025 guidelines mark a milestone for the pharmaceutical cold chain. They draw a clear distinction between traditional active containers and newly defined advanced active systems, recognising that temperature control alone is no longer sufficient. Active, data-driven, reusable packaging solutions are now considered the gold standard for ensuring the integrity and sustainability of global vaccine shipments. The shift reflects a fundamental mindset change across the industry — from maintaining temperature to assuring it. The ability to monitor shipments in real time gives pharmaceutical manufacturers and logistics teams confidence that high-value vaccines will reach their destination exactly as intended, regardless of conditions along the way.

Temperature Ranges in Pharmaceutical Cold Chain

The pharmaceutical cold chain serves multiple distinct temperature ranges, each with specific infrastructure requirements:

Most vaccines must stay at +2°C–8°C without interruption — the “cold chain” temperature range recognised in global immunisation programmes. Frozen storage at −20°C to −10°C serves some plasma products and specialty biologics. Ultra-cold / cryogenic storage at −60°C to −90°C is required for mRNA vaccines and advanced biologics, while gene therapy products may require cryogenic temperatures below −150°C. Maintaining these ranges continuously is essential to prevent loss of potency, safety risks, or regulatory non-compliance.

Drug Supply Chain Security Act (DSCSA) and Regulatory Compliance

Beginning July 31, 2026, a significant new phase of DSCSA compliance requirements becomes enforceable for small dispensers — the final major cohort of pharmaceutical supply chain participants required to implement interoperable electronic tracking of prescription drugs. The DSCSA’s package-level electronic tracking requirements create mandatory integration between pharmaceutical cold chain logistics and digital traceability platforms, fundamentally changing the documentation and compliance requirements for pharmaceutical cold chain operators.

4. Technology: The Digital Cold Chain Revolution

AI-Powered Predictive Analytics

The cold chain in 2026 is transitioning from reactive management — detecting and responding to temperature excursions after they occur — to predictive, preventive logistics, where AI systems anticipate equipment failures, weather events, and transit delays before they create product-compromising temperature deviations. Fleets that can prove — with data — that every temperature-sensitive shipment was maintained within specification from origin to destination will win the contracts, avoid the spoilage, and command premium rates.

Lineage’s proprietary “Lineage Eye” AI platform has reportedly reduced temperature deviations by 78% in pilot facilities, demonstrating the extraordinary operational impact possible when AI-powered predictive analytics are applied to cold chain management at scale. The platform integrates sensor data from across the warehouse network to identify patterns preceding temperature excursions, enabling pre-emptive maintenance intervention before equipment failure affects stored product.

Symrise’s AI-powered flavour formulation platform and similar AI systems being deployed across the food industry are generating demand for cold chain operators who can provide the real-time visibility and predictive analytics capability that premium food manufacturers and pharmaceutical companies require to manage their temperature-sensitive supply chains.

IoT Sensor Networks: Continuous Monitoring as Standard

IoT sensors that transmit temperature data every 1–5 minutes are now the baseline expectation for any serious cold chain operator. This near-continuous monitoring allows for early detection of temperature excursions and immediate intervention — compared to the periodic manual checks that were industry standard a decade ago. Regulations like GDP (Good Distribution Practice) require continuous monitoring with documented records for pharmaceutical products; FSMA requires traceability records for specified food categories. Cold chain in 2026 comes down to one simple truth: operators who can prove, with data, that every shipment was maintained within specification will win the contracts and command premium rates.

IoT adoption is accelerating because visibility has become simultaneously a compliance and a risk management issue. A temperature excursion detected at the warehouse loading dock is a commercial problem; the same excursion undetected until the product reaches the recipient is a regulatory violation, a product liability event, and a brand crisis. The cost of IoT monitoring is negligible compared to these consequences, making sensor deployment a straightforward commercial decision.

Blockchain-Based Traceability

Governments are strengthening food and drug safety rules, mandating more granular traceability. Under FSMA 204 in the US, certain foods must be traced through electronic records. The EU’s Import Control System 2 and Canada’s Safe Food for Canadians Regulations require electronic pre-notification and traceability data. China has implemented digital clearance for food imports. These regulations are pushing cold chain logistics companies to adopt blockchain and cloud platforms that provide immutable records of a product’s journey.

Blockchain technology can link temperature logs, location data, and handling records, ensuring transparency and preventing fraud. In the pharmaceutical sector, blockchain enhances security for high-value biologics, reduces counterfeit risk, and provides the end-to-end chain of custody documentation required by regulators. In the food sector, blockchain-based traceability enables rapid, targeted product recalls when food safety issues are identified — the ability to trace a contaminated product to a specific supplier lot within hours rather than days dramatically reduces the scale and cost of food safety incidents.

Warehouse Automation: The Robotic Cold Chain

Automated cold storage — using robotic storage and retrieval systems (ASRS), autonomous mobile robots (AMRs), and automated guided vehicles (AGVs) operating in refrigerated and frozen environments — is transforming the economics and throughput capability of cold chain warehousing. The labour challenge in cold storage environments is acute: working in a −25°C freezer is physically demanding, limited by regulatory maximum exposure times, and increasingly difficult to staff in tight labour markets. Automation eliminates the labour constraint entirely in the most extreme temperature environments while simultaneously improving accuracy, throughput, and energy efficiency.

NewCold Coöperatief UA is the global leader in automated cold chain warehouse technology, operating facilities that are among the most automated in the world, with robotic crane systems operating continuously in fully frozen environments at throughput rates impossible with manual operations. The company’s model — highly capital-intensive automated facilities serving major food manufacturers and retailers on long-term contracts — represents the future architecture of the large-scale cold storage industry.

Smart Refrigerated Transport

Standard reefer trucks can maintain temperatures from −35°C to +35°C depending on cargo requirements. Modern smart reefer units are equipped with: GPS tracking providing real-time location; IoT sensors monitoring internal temperature, humidity, and cargo condition; remote diagnostic systems allowing fleet operators to identify and address equipment issues before they cause temperature excursions; and AI-powered route optimisation that reduces fuel consumption and minimises transit times. Reefer fleets fitted with energy-saving inverter-driven compressors are reducing energy consumption significantly compared to conventional reefer technology.

5. Sustainability: Decarbonising the Cold Chain

The Energy Challenge

Cold chain operations are among the most energy-intensive in the food and logistics industries. Refrigerated warehouses consume approximately 10–15% of all US commercial energy, and refrigerated transport adds significant fuel costs on top of the facility energy burden. The energy cost of maintaining cold chain infrastructure — and the greenhouse gas emissions from both the electricity consumed and the refrigerants used — creates a substantial environmental footprint that is increasingly subject to regulatory and customer scrutiny.

Electric Reefer Trucks

The transition from diesel-powered refrigeration units on road trailers to electric reefer systems is advancing commercially as electric truck platforms improve in range and payload capacity. North America’s cold chain logistics operators are adopting energy-efficient refrigeration systems, low-emission transport options like electric reefer units, and eco-friendly packaging. European cold chain logistics companies are using IoT and real-time systems to check temperature, humidity, and location in refrigerated warehouses and vehicles, helping reduce spoilage and meet strict EU food safety rules.

The economic case for electric reefer units is strengthening as diesel prices rise and electricity grid infrastructure improves. For urban and suburban delivery routes where daily mileage is predictable and charging infrastructure is accessible, electric reefer vehicles offer lower total cost of ownership than diesel equivalents over a multi-year operating period.

Solar-Powered Cold Storage

Innovations such as solar-powered portable freezers enable distribution in remote regions with limited grid access, while large-scale solar installations on cold storage facility rooftops are reducing grid electricity dependency and carbon emissions for major cold chain operators. The combination of solar generation, battery storage, and smart energy management systems is enabling some cold storage facilities to approach energy self-sufficiency during peak solar generation periods, dramatically reducing operating costs and carbon intensity.

Sustainable Packaging Innovation

Reusable cold chain packaging systems — standardised, trackable containers using vacuum insulation panels (VIPs), phase-change materials (PCMs), and smart temperature-monitoring devices — are reducing the waste and per-shipment cost associated with single-use cold chain packaging. The pharmaceutical cold chain has been an early adopter of reusable active temperature-controlled containers for high-value biologics shipments, and the technology is advancing toward broader food cold chain applications.

The global cold chain packaging market is forecast to expand from USD 38.15 billion in 2026 to USD 100 billion by 2035, with sustainable packaging innovation — including expanded polystyrene alternatives, bio-based insulation materials, and returnable container systems — driving significant innovation investment.

6. Regulatory Landscape: The Compliance Revolution

FSMA and Food Safety Traceability

The US Food Safety Modernization Act Section 204 Food Traceability Final Rule — which requires companies handling foods on the FDA’s Food Traceability List to maintain key data elements in electronic records across the supply chain — represents the most significant food safety regulatory development affecting the US cold chain in decades. While the compliance deadline has been extended (potentially to July 2028), the direction of travel is clear: digital, electronic traceability records for temperature-sensitive foods are becoming a regulatory requirement, not an optional quality enhancement.

IoT adoption accelerates because visibility has become a compliance and risk issue. Companies must modernise software and physical infrastructure simultaneously — digital tools implemented without corresponding improvements to foundational cold chain assets remain exposed to disruption, audit risk, and rising costs. Cold chain in 2026 is a systems challenge, not a technology checklist.

EU and Global Regulatory Convergence

The EU’s Import Control System 2 mandates electronic pre-notification of food shipments, while Good Distribution Practice (GDP) guidelines for pharmaceutical cold chain are being updated to reflect the requirements of advanced active systems for vaccine and biologic transport. China has implemented digital clearance for food imports, and Canada’s Safe Food for Canadians Regulations require comprehensive traceability documentation. The global trajectory is toward mandatory electronic traceability, continuous monitoring documentation, and validated cold chain records — creating a growing compliance infrastructure requirement for every cold chain operator serving regulated markets.

GDP and Pharmaceutical Cold Chain Compliance

The Drug Supply Chain Security Act (DSCSA) represents the pharmaceutical cold chain’s most significant regulatory development, requiring package-level electronic tracking of prescription drugs throughout the supply chain. Small dispensers face their DSCSA compliance deadline in November 2026 — the final major cohort of the pharmaceutical supply chain to implement interoperable electronic drug tracking. This creates a final wave of technology investment requirement that is driving adoption of cold chain management platforms across the pharmaceutical distribution network.

7. Regional Dynamics

North America: Technology and Capacity Leadership

The US cold chain logistics market is estimated at USD 97.13 billion in 2026, expected to reach USD 133.87 billion by 2031 at a CAGR of 6.63%. Automation rollouts, pharmaceutical temperature-control sophistication, and stricter sustainability mandates are reshaping network design, capital allocation, and service differentiation. North America’s cold chain market held the largest revenue share of more than 33% in 2025.

The US market is characterised by a quasi-duopoly at the top — Lineage Logistics and Americold collectively control a majority of national refrigerated warehouse capacity, creating a dominant position in many metropolitan markets that smaller operators serve by specialising in pharmaceutical GDP-compliant services, ethnic food distribution requiring bespoke handling, or urban last-mile facilities where mega-warehouse footprints are impractical.

Lineage’s Cold Chain Insights Survey, based on responses from 1,000 supply chain decision-makers across the US, Canada, and Mexico, found that resilience has become the defining priority for supply chain leaders, driving increased investment in data, automation, and closer collaboration with logistics partners. “Supply chain leaders are operating in an environment where volatility is the norm, not the exception,” said Greg Lehmkuhl, President and CEO of Lineage.

Asia-Pacific: The Growth Engine

The Asia-Pacific cold chain logistics market is valued at USD 222.10 billion in 2026 and is predicted to reach USD 724.17 billion by 2035, growing at a CAGR of 14.18% — the fastest of any major region. This extraordinary growth trajectory reflects the simultaneous modernisation of food retail infrastructure, rapid expansion of online grocery and quick commerce, growing pharmaceutical manufacturing and distribution capability, and massive middle-class dietary transition toward protein-rich, fresh, and temperature-sensitive foods across China, India, and Southeast Asia.

China and India display peak cold chain growth momentum. China’s food cold chain — still significantly underdeveloped relative to the country’s food production and consumption scale — is receiving massive infrastructure investment as the Chinese government has identified cold chain development as a strategic food security priority. India’s cold chain market is one of the fastest-growing globally, driven by the extraordinary pace of organised retail expansion, the growth of modern food processing, and the government’s National Cold Chain Policy that aims to reduce the approximately 40% post-harvest food loss rate that characterises traditional food distribution.

Europe: Sustainability Leadership and Regulatory Sophistication

Europe leads globally in cold chain sustainability practices, with strict EU food safety and pharmaceutical regulation creating the most demanding compliance environment globally. European cold chain logistics companies are deploying IoT and real-time systems to check temperature, humidity, and location throughout their networks. The European cold chain logistics market accounted for USD 90.8 billion in 2025, anticipated to grow at a CAGR of 12.9% between 2026 and 2035.

Latin America: The Fastest-Growing Cold Storage Region

Latin America led global cold storage growth at 8.6% in 2026, driven by Brazil’s dominant position as a global protein exporter requiring extensive cold chain infrastructure for beef, poultry, and seafood. Ferrero’s acquisition of Bold Snacks in Brazil reflects broader food industry investment in Latin American cold chain as a prerequisite for serving emerging market premium food demand.

8. Critical Risks and Challenges

Energy Cost Volatility

Cold chain operations face disproportionate exposure to energy cost volatility because refrigeration is a continuous, non-deferrable energy demand. Cold storage facilities cannot choose to reduce energy consumption during peak pricing periods without risking product safety and regulatory compliance. The combination of rising energy prices, increasing carbon taxes, and the growing energy demand of expanded cold chain capacity creates a persistent and structurally challenging cost environment for cold chain operators.

Labour Shortages in Extreme Environments

Working in cold chain environments — particularly in −25°C freezer facilities — is physically demanding, limited by regulatory maximum exposure times, and increasingly difficult to staff as labour markets tighten and younger workers seek less arduous working conditions. The industry’s response — automation — is capital-intensive and requires significant time to implement. In the interim, labour shortages are creating operational constraints that limit throughput and increase operating costs across the cold chain network.

Ageing Infrastructure and Automation Investment

A significant proportion of existing cold chain infrastructure — particularly in North America — was built decades ago using conventional non-automated designs that are difficult or impossible to retrofit with modern robotic systems. Whether ageing facilities can be automated with AI and autonomous vehicles to extend their lifespan is identified by Lineage’s CEO as one of the three most significant challenges facing the industry over the next five years. The capital investment required to automate or replace ageing cold storage infrastructure is enormous, creating a generational investment challenge.

Amazon’s Potential Market Entry

The potential entry of Amazon into the cold storage market — to control last-mile delivery of grocery and food products — is identified by Lineage’s CEO as one of the three most significant threats to the cold chain industry. Amazon’s logistics infrastructure, technology capability, and willingness to invest at scale in new market segments creates a potential competitive threat unlike any the cold chain industry has previously faced from within the logistics sector.

Climate Change and Physical Infrastructure Risk

Extreme weather events are becoming more frequent, disrupting cold chain routes and infrastructure. A sudden heatwave, flood, or hurricane can simultaneously damage cold storage facilities, disrupt power supply (triggering temperature excursions), and close road and rail routes, creating multi-dimensional supply chain crises. The pharmaceutical cold chain is particularly vulnerable — “designing systems that can withstand instability, whether it’s a grounded flight, a sudden heatwave or a customs delay, without compromising the safety or efficacy of the vaccine” is now a fundamental pharmaceutical cold chain design requirement.

9. Strategic Outlook for Stakeholders

Actionable Recommendations

Invest in Digital Infrastructure Before Compliance Mandates Force It: The trajectory of food safety and pharmaceutical cold chain regulation globally is toward mandatory continuous monitoring, electronic traceability, and validated temperature records. Cold chain operators who invest in IoT sensor networks, blockchain-based traceability platforms, and AI-powered monitoring systems ahead of regulatory deadlines will not only achieve compliance but will command premium rates from the pharmaceutical, premium food, and international trade customers who require these capabilities.

Treat Automation as a Survival Investment, Not a Productivity Enhancement: Labour shortages in cold environments are structural, not cyclical. The physical demands of sub-zero working environments and the tightening of labour market availability make the traditional staffing model for cold storage increasingly untenable. Automation investment — particularly in robotic ASRS for freezer environments — delivers payback periods that are increasingly compelling as labour costs rise, and creates operational capabilities that non-automated competitors simply cannot match.

Pharmaceutical Cold Chain as a Strategic Premium: The pharmaceutical cold chain — particularly ultra-cold biologics and mRNA vaccine logistics — commands materially higher margins than food cold chain because of the technical complexity, regulatory compliance requirements, and liability consequences of failure. Cold chain operators with validated pharmaceutical-grade facilities, continuous monitoring documentation, and experienced pharmaceutical logistics teams are competing in a market with structural supply scarcity relative to the explosive demand growth of the biologics industry.

Build Asia-Pacific Capacity Before the Window Closes: The Asia-Pacific cold chain market is growing at 14.18% CAGR — the fastest of any major region. Infrastructure partnerships, joint ventures, and acquisitions in China, India, and Southeast Asia cold chain now will secure the market positions that the region’s extraordinary growth will reward over the next decade.

Strategic Summary: The 2026 Cold Chain Business Model

| Strategic Priority | Traditional Model | 2026 Competitive Standard |

|---|---|---|

| Monitoring | Periodic manual checks | Continuous IoT with AI anomaly detection |

| Traceability | Paper records and manual logs | Blockchain-linked immutable digital records |

| Warehouse Operations | Manual labour in cold environments | Automated ASRS and robotic picking |

| Energy Strategy | Grid-dependent, unmanaged | Solar-powered, battery-backed, smart managed |

| Market Positioning | Food-focused commodity logistics | Diversified food + pharmaceutical premium |

| Growth Strategy | Organic capacity addition | M&A platform consolidation + technology integration |

10. Leading Industry Companies

| Company | Region | Strategic Focus |

|---|---|---|

| Lineage Logistics | USA/Global | World’s largest temperature-controlled warehousing company with over 3.0 billion cubic feet of storage and 14%+ global market share. Proprietary “Lineage Eye” AI platform reducing temperature deviations by 78% in pilot facilities. Data-driven platform transitioning from real estate to technology powerhouse. |

| Americold Realty Trust | USA/Global | Major publicly traded cold storage REIT. Dominant in US food cold chain with facilities across 17 countries. Integrated multimodal transportation and automation systems ensuring pharmaceutical-grade storage compliance. |

| NewCold Coöperatief UA | Netherlands/Global | Global leader in automated cold chain warehouse technology. Fully robotic frozen storage facilities serving major food manufacturers and retailers on long-term contracts. The industry’s benchmark for automated cold chain. |

| DHL Supply Chain (Cold) | Germany/Global | Global cold chain logistics through DHL’s supply chain division. Sustainable aviation fuel investment and net-zero 2050 target. Strong pharmaceutical and food cold chain across 220+ countries. |

| Maersk (Cold Chain) | Denmark/Global | World’s largest reefer container operator. Methanol-powered vessel investment and electric inland transport for green cold chain. Strong Asia-Pacific cold chain coverage. |

| Nichirei Logistics Group | Japan/Asia | Japan’s leading cold chain operator. Dominant in Japanese refrigerated warehousing and expanding across Asia-Pacific as regional cold chain demand grows. |

| Swire Cold Chain Logistics | Hong Kong/Asia | Leading Asia-Pacific cold chain specialist. Strong Hong Kong, mainland China, and Southeast Asia presence serving food and pharmaceutical clients. |

| CEVA Logistics | France/Global | Global cold chain logistics through CMA CGM Group. Comprehensive pharmaceutical and food cold chain across multimodal transportation networks. |

| DB Schenker | Germany/Global | European cold chain logistics leader with strong pharmaceutical GDP-compliant cold chain capability across Europe and Asia. |

| Snowman Logistics | India | India’s leading cold chain company. Expanding rapidly as India’s organised food retail sector grows. Leased new multi-temperature controlled warehouse in Guwahati, Assam in January 2024. |

Related: As global supply chain volatility persists, the ability to maintain the integrity of perishable goods while optimizing distribution networks has become a critical competitive advantage. Explore the latest advancements in cold-chain technology, digital tracking, and route optimization in our Global Food & Beverage Logistics Industry Report 2026.

Frequently Asked Questions (FAQ)

What is the global cold chain market size in 2026?

The global cold chain market is estimated at USD 276.5 billion to USD 496.8 billion in 2026, depending on the scope of measurement. MarketsandMarkets places the core cold chain market at USD 276.5 billion; Precedence Research estimates the cold chain logistics market at USD 496.80 billion; and Grand View Research estimates USD 437.49 billion. The variation reflects differences in what is included — narrower estimates focus on cold storage and refrigerated transport, while broader estimates include cold chain monitoring technology, packaging, and the full range of pharmaceutical cold chain services. The market is growing at a CAGR of 10.5–20.5% depending on the research scope, making cold chain one of the fastest-growing infrastructure sectors globally. Food and beverages account for over 55% of total market value, with pharmaceuticals the fastest-growing application segment.

What is the cold chain and why is it critical?

The cold chain is the coordinated, temperature-controlled movement of temperature-sensitive products — including fresh food, frozen food, vaccines, biologics, and pharmaceutical medicines — through a supply chain using refrigerated storage, transportation, and continuous monitoring to prevent spoilage, maintain safety, and ensure regulatory compliance. It is critical because the products it serves are essential to human health and food security: a temperature excursion during vaccine distribution can render life-saving medicines ineffective; inadequate food cold chain in developing markets contributes to the 1.3 billion tonnes of food wasted annually; and failures in pharmaceutical cold chain can create patient safety events with serious consequences. The cold chain is not optional infrastructure — it is the foundation of modern food distribution and pharmaceutical delivery, and its absence or inadequacy is directly correlated with disease, malnutrition, and preventable deaths at population scale.

What is driving such rapid growth in the cold chain market?

Five structural forces are simultaneously driving extraordinary cold chain market growth. First, the biological medicine revolution — mRNA vaccines, monoclonal antibodies, gene therapies, and cell therapies all require continuous cold chain management at increasingly stringent temperature requirements, driving unprecedented pharmaceutical cold chain investment. Second, online grocery and quick commerce — the global proliferation of e-grocery platforms and 15–30 minute delivery promises is extending cold chain infrastructure all the way to the consumer’s doorstep. Third, emerging market food transition — the dietary shift of billions of people across Asia, Africa, and Latin America toward protein-rich, fresh, and temperature-sensitive foods is creating enormous new cold chain demand in markets where infrastructure has historically been limited. Fourth, food safety and pharmaceutical regulation — FSMA, DSCSA, GDP, and their global equivalents are mandating continuous monitoring and digital traceability, driving technology investment across the cold chain. Fifth, climate change — rising ambient temperatures and more frequent extreme weather events are extending the geographic scope of cold chain requirements and increasing the technical challenge of maintaining cold chains reliably.

What is driving such rapid growth in the cold chain market?

Five structural forces are simultaneously driving extraordinary cold chain market growth. First, the biological medicine revolution — mRNA vaccines, monoclonal antibodies, gene therapies, and cell therapies all require continuous cold chain management at increasingly stringent temperature requirements, driving unprecedented pharmaceutical cold chain investment. Second, online grocery and quick commerce — the global proliferation of e-grocery platforms and 15–30 minute delivery promises is extending cold chain infrastructure all the way to the consumer’s doorstep. Third, emerging market food transition — the dietary shift of billions of people across Asia, Africa, and Latin America toward protein-rich, fresh, and temperature-sensitive foods is creating enormous new cold chain demand in markets where infrastructure has historically been limited. Fourth, food safety and pharmaceutical regulation — FSMA, DSCSA, GDP, and their global equivalents are mandating continuous monitoring and digital traceability, driving technology investment across the cold chain. Fifth, climate change — rising ambient temperatures and more frequent extreme weather events are extending the geographic scope of cold chain requirements and increasing the technical challenge of maintaining cold chains reliably.

What is the difference between food cold chain and pharmaceutical cold chain?

While both food and pharmaceutical cold chains share the fundamental objective of maintaining products within their specified temperature ranges, they differ significantly in technical requirements, regulatory framework, and commercial dynamics. Food cold chain primarily operates at chilled (0°C–4°C), frozen (−18°C to −25°C), and refrigerated (2°C–8°C) temperature ranges, with relatively forgiving excursion tolerance for most products. Food cold chain compliance is governed primarily by food safety regulations (FSMA, EU food safety laws) that require traceability records and temperature monitoring. Pharmaceutical cold chain operates at the same chilled and frozen ranges for conventional medicines but extends to ultra-cold (−60°C to −80°C) for mRNA vaccines and biologics, and cryogenic temperatures for cell therapies. Pharmaceutical cold chain compliance is governed by GDP (Good Distribution Practice) guidelines and the DSCSA, with zero tolerance for temperature excursions that could compromise drug potency and patient safety. The consequences of cold chain failure differ dramatically: a food cold chain failure typically results in food waste and commercial loss; a pharmaceutical cold chain failure can result in ineffective medicines, patient harm, and serious regulatory consequences.

Who are the largest cold chain companies globally in 2026?

The global cold chain market is led by a combination of specialised temperature-controlled warehousing companies and diversified logistics groups with significant cold chain capability. Lineage Logistics is the world’s largest temperature-controlled warehousing company with over 3.0 billion cubic feet of storage capacity and 14%+ global market share — and has transitioned into a technology platform through its AI-powered “Lineage Eye” monitoring system. Americold Realty Trust is the largest publicly traded cold storage REIT, operating over 250 facilities globally. NewCold (Netherlands) is the global leader in automated cold chain warehouse technology. Among diversified logistics groups, DHL, Maersk, DB Schenker, CEVA, and UPS all have significant cold chain capabilities. In Japan and Asia-Pacific, Nichirei Logistics and Swire Cold Chain Logistics are the dominant regional specialists. In India, Snowman Logistics is the market leader in a rapidly growing national cold chain market.

How is AI transforming cold chain operations in 2026?

AI is transforming the cold chain across three critical dimensions in 2026. First, predictive maintenance — AI algorithms analyse sensor data from refrigeration equipment, compressors, and temperature controllers to identify patterns preceding equipment failure, enabling maintenance intervention before a breakdown causes a temperature excursion. Lineage’s “Lineage Eye” system has reportedly reduced temperature deviations by 78% in pilot facilities through this capability. Second, route optimisation — AI-driven route planning minimises transit times, reduces fuel consumption, and selects routes that minimise temperature excursion risk based on weather, traffic, and historical performance data. Third, inventory management — AI-powered demand forecasting and inventory optimisation systems help cold chain customers make better decisions about production, storage, and movement, reducing excess inventory, minimising dwell time, and preventing the food and energy waste associated with suboptimal cold chain utilisation.

What are the biggest sustainability challenges in cold chain logistics?

Cold chain faces five significant sustainability challenges. First, energy consumption — cold storage facilities consume 10–15% of US commercial energy, and the expanding scope of cold chain infrastructure will increase total sector energy demand substantially. Second, refrigerant gases — the high-global-warming-potential refrigerants historically used in cold chain equipment (HFCs, HCFCs) are being phased out under the Kigali Amendment to the Montreal Protocol, requiring capital-intensive equipment replacement. Third, carbon emissions from diesel reefer trucks — refrigerated transport’s diesel consumption creates both fuel cost exposure and significant carbon emissions. Fourth, single-use cold chain packaging — the foam boxes, gel packs, and insulated liners used for pharmaceutical and food cold chain shipments generate significant waste. Fifth, infrastructure energy efficiency — many cold storage facilities were designed without energy efficiency as a priority, making them structurally energy-intensive. The industry is responding through solar-powered facilities, electric reefer truck fleets, natural refrigerant transitions, reusable container systems, and energy management platforms — but the scale of the challenge relative to the pace of cold chain market growth means the sector’s absolute energy consumption will continue rising for the foreseeable future even as energy intensity per unit improves.

Sources and Additional References

- MarketsandMarkets: Cold Chain Market Set to Reach USD 455.0 Billion by 2031 — https://www.marketsandmarkets.com/blog/FB/cold-chain-market-overview

- MarketsandMarkets: Americold and Lineage Leading Players in the Cold Chain Market — https://www.marketsandmarkets.com/ResearchInsight/cold-chains-frozen-food-market.asp

- Grand View Research: Cold Chain Market Size, Share, Trends & Industry Report 2033 — https://www.grandviewresearch.com/industry-analysis/cold-chain-market

- Grand View Research: Cold Chain Market to Reach USD 1,611.0 Billion by 2033 — https://www.grandviewresearch.com/press-release/global-cold-chain-market

- Precedence Research: Cold Chain Market Size, Share and Trends 2026–2034 — https://www.precedenceresearch.com/cold-chain-market

- Precedence Research: Cold Chain Logistics Market Size to Hit USD 1,477.53 Billion by 2035 — https://www.precedenceresearch.com/cold-chain-logistics-market

- GlobeNewswire / Precedence Research: Cold Chain Logistics Market Size Worth USD 1,477.53 Billion by 2035 — https://www.globenewswire.com/news-release/2026/02/25/3244730/0/en/Cold-Chain-Logistics-Market-Size-Worth-USD-1-477-53-Billion-by-2035.html

- Mordor Intelligence: US Cold Chain Logistics Market Size, Industry Growth & Share 2026–2031 — https://www.mordorintelligence.com/industry-reports/united-states-cold-chain-logistics-market

- Future Market Insights: Cold Chain Logistics Market Global Analysis Report 2035 — https://www.futuremarketinsights.com/reports/cold-chain-logistics-market

- Verified Market Research: Top 7 Cold Chain Logistics Companies — Market Share & Analysis 2026 — https://www.verifiedmarketresearch.com/blog/top-cold-chain-logistics-companies/

- The Business Research Company: Cold Chain Market Forecast Report 2026–2035 — https://www.thebusinessresearchcompany.com/report/cold-chain-global-market-report

- Technavio: Cold Chain Market Analysis, Size, and Forecast 2026–2030 — https://www.technavio.com/report/cold-chain-market-industry-analysis

- Towards Packaging: Cold Chain Packaging Market Trends and Size 2026–2035 — https://www.towardspackaging.com/insights/cold-chain-packaging-market

- Supply Chain Digital: Lineage — Cold Chain Resilience Rises Amid Volatility — https://supplychaindigital.com/news/lineage-cold-chain-resilience-rises-amid-volatility

- GCCA: 2026 Cold Chain Forecast — Experts on the Future of Logistics — https://www.gcca.org/magazine-article/driving-the-cold-chain/

- Olimp Warehousing: Cold Chain Logistics in 2026 — Trends, Costs & Solutions — https://olimpwarehousing.com/cold-chain-logistics-2026-trends-costs-solutions/

- iGPS: Cold Chain Logistics Trends That Are Changing the Industry 2026 — https://igps.net/cold-chain-logistics-trends-that-are-changing-the-industry/

- FleetRabbit: Cold Chain Logistics Technology Outlook for 2026 — https://fleetrabbit.com/blogs/post/cold-chain-logistics-2026

- Air Cargo Week / European Pharmaceutical Manufacturer: Protecting Vaccine Shipments in 2026 — https://aircargoweek.com/protecting-vaccine-shipments-in-2026-what-the-next-era-of-cold-chain-looks-like/

- Tempcontrolpack: Vaccine Cold Chain Monitoring Guide 2026 — https://www.tempcontrolpack.com/knowledge/vaccine-cold-chain-monitoring-guide-2026-real-time-data-compliance-trends/

- Tempcontrolpack: FDA Cold Chain Compliance in 2025 — Regulations and Trends — https://www.tempcontrolpack.com/knowledge/fda-cold-chain-compliance-in-2025-regulations-and-trends/

- Olimp Warehousing: Pharmaceutical Cold Chain Logistics Safety, Compliance & Integrity — https://olimpwarehousing.com/pharmaceutical-cold-chain-logistics/