Introduction

The global animal feed industry stands at a critical juncture in 2026. Transitioning from a traditional commodity-driven model to a high-tech, performance-focused sector, the industry is currently valued at approximately USD 559.66 billion. As global demand for high-quality protein in meat, dairy, and aquaculture continues to rise, feed manufacturers are shifting focus toward precision nutrition, sustainability, and supply chain resilience to mitigate the risks of a volatile global economic landscape.

Executive Summary: The 2026 Global Animal Feed Industry

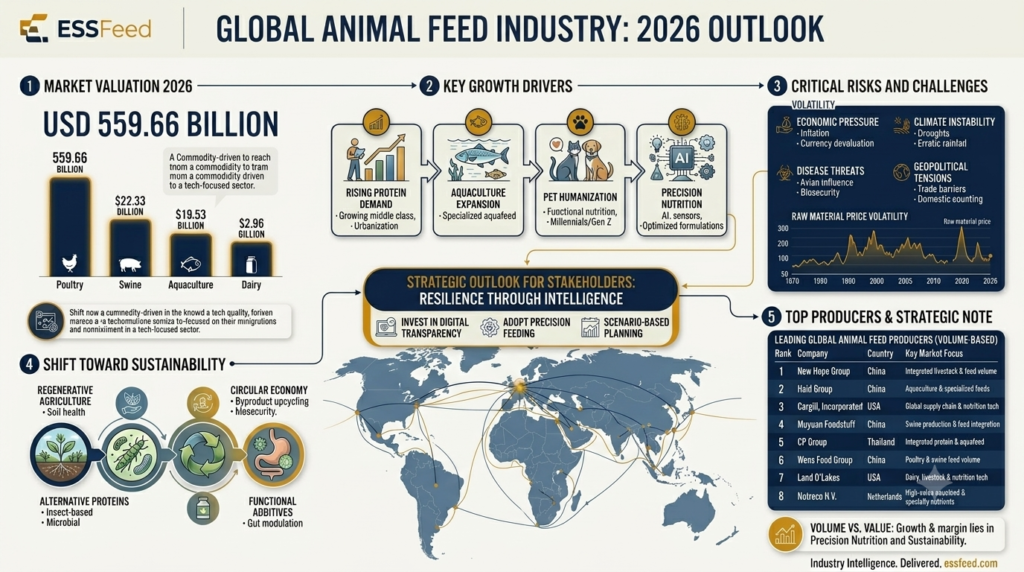

In 2026, the global animal feed industry, valued at approximately USD 559.66 billion, is undergoing a fundamental transformation. The sector is moving away from traditional, commodity-heavy models toward a precision-nutrition architecture driven by digital intelligence, sustainability, and supply chain resilience. As global protein demand continues to climb—spurred by urbanization in emerging markets and the “pet humanization” trend—feed manufacturers are increasingly adopting AI-driven formulations and bioactive additives to maximize growth and feed conversion ratios (FCR).

However, the global animal feed industry faces significant headwinds. Producers are currently navigating a “triple threat” of geopolitical trade volatility, climate-induced crop instability, and recurring disease pressures such as avian influenza. These challenges have elevated sustainability and transparency from corporate goals to absolute competitive necessities.

Key Takeaways for Stakeholders:

- Intelligence as Strategy: Success in 2026 is no longer solely about production volume. It requires the integration of IoT, blockchain, and predictive analytics to optimize procurement and ensure the ethical, low-carbon sourcing required by modern retail partners.

- The Precision Shift: Future-proof companies are shifting focus from “least-cost” formulations to high-value, species-specific nutrition that improves gut health and stress resilience.

- Consolidation and Diversification: The market remains a mix of massive, volume-leading Chinese conglomerates and Western multinational firms that leverage deep R&D and global supply chain integration.

Ultimately, the global animal feed industry of 2026 serves as the sophisticated backbone of global food security. Firms that prioritize resilience through digital transparency and invest in regenerative ingredient sources will be best positioned to capture market share in an increasingly volatile global economy.

Table of Contents

1. Market Overview: The 2026 Landscape

The global animal feed industry serves as the backbone of the global livestock and protein value chain. In 2026, the sector is characterized by:

- Industrialization: A shift toward large-scale, nutritionally optimized commercial feed production.

- Strategic Consolidation: Major players are engaging in aggressive mergers and acquisitions to strengthen regional presence and diversify specialty portfolios (e.g., De Heus’s acquisition of CJ Feed & Care).

- Value-Added Focus: Feed is no longer just a cost item; it is a strategic input used to optimize growth cycles, immune health, and feed conversion ratios (FCR).

2. Key Growth Drivers

Several interconnected factors are fueling industry expansion through 2034:

- Rising Protein Demand: Rapid urbanization and growing middle classes in emerging economies (India, China, Brazil) are driving higher consumption of animal-based food products.

- Aquaculture Expansion: With wild fish stocks under pressure, aquaculture is the fastest-growing food production sector. This is creating a surge in demand for specialized, high-digestibility aquafeed.

- Pet Humanization: The “pet as family” trend among Millennials and Gen Z is driving premiumization in the pet nutrition segment, where functional, science-backed ingredients mirror human health trends.

- Precision Nutrition: The adoption of AI, real-time sensors, and predictive modeling allows manufacturers to tailor formulations to species, age, and production conditions, minimizing waste and maximizing yield.

3. Critical Risks and Challenges

Producers are navigating a complex risk environment categorized by four primary pillars:

- Economic Pressures: Persistent inflation and currency devaluation are making essential imported inputs increasingly unpredictable for regional producers.

- Climate Instability: Droughts and erratic rainfall in key crop-producing zones (particularly Latin America) are disrupting the predictability of corn and soy supplies.

- Disease Threats: Outbreaks of highly pathogenic diseases, such as avian influenza, necessitate heightened investment in biosecurity and immunity-boosting feed additives.

- Geopolitical Tensions: Trade barriers and tariff fluctuations are forcing procurement teams to diversify suppliers and prioritize domestic ingredient sourcing.

4. The Shift Toward Sustainability and Innovation

Sustainability is no longer an optional attribute; it is a core business requirement.

- Regenerative Agriculture: The industry is increasingly sourcing ingredients from farms that utilize regenerative practices to improve soil health and reduce carbon footprints.

- Alternative Proteins: To reduce reliance on traditional ingredients, microbial proteins, insect-based proteins, and precision fermentation products are entering the mainstream.

- Circular Economy: Upcycling agricultural byproducts into high-value feed ingredients is helping to close the loop and reduce resource intensity.

- Functional Additives: There is a marked shift toward bioactive compounds—such as RNA-based additives and targeted probiotics—that modulate gut flora and enhance stress resilience.

5. Strategic Outlook for Stakeholders

For industry participants, the strategy for the remainder of 2026 and beyond should focus on resilience through intelligence.

“The biggest constraint in 2026 is not whether the demand exists, but whether supply chains can deliver amid global volatility. Firms that integrate digital technologies, optimize procurement, and ensure transparency throughout the value chain will capture significant market share.”

Actionable Recommendations:

- Invest in Digital Transparency: Utilize blockchain or IoT-enabled tracking to ensure ethical sourcing and regulatory compliance, which are becoming non-negotiable for retail and foodservice partners.

- Adopt Precision Feeding Models: Move beyond price-per-ton metrics. Evaluate feed value based on nutritional density, bioavailability, and overall impact on livestock productivity.

- Scenario-Based Planning: Deploy robust modeling tools to manage inventory positions and anticipate tariff impacts, ensuring business continuity in the face of sudden geopolitical or climatic shifts.

Leading Global Animal Feed Producers (Volume-Based)

The global animal feed industry is currently defined by a duality between massive Chinese agro-industrial conglomerates and traditional Western multi-national agri-business giants. While Chinese firms like New Hope Group and Haid Group dominate in terms of pure compound feed volume due to intense domestic demand, Western players like Cargill and ADM maintain a significant competitive edge through global supply chain integration, advanced nutritional research, and high-value specialty additive portfolios. This landscape reflects a broader industry trend where volume-based production is increasingly complemented—or in some cases overtaken—by precision-driven, technology-integrated nutrition strategies.

The table below identifies key players who consistently rank among the highest in annual compound feed production volume.

| Company Name | Country | Key Market Focus |

| New Hope Group | China | Integrated livestock & feed volume |

| Haid Group | China | Aquaculture & specialized feeds |

| Cargill, Incorporated | United States | Global supply chain & nutrition tech |

| Muyuan Foodstuff | China | Swine production & feed integration |

| CP Group (Charoen Pokphand) | Thailand | Integrated protein & aquafeed |

| Wens Food Group | China | Poultry & swine feed volume |

| Land O’Lakes | United States | Dairy, livestock & nutrition tech |

| Nutreco N.V. | Netherlands | High-value aquafeed & specialty nutrients |

Conclusion: The Path Forward for the Global Animal Feed Industry

As we look toward the remainder of 2026 and beyond, the global animal feed industry is defined by a permanent shift from volume-driven production to precision-integrated intelligence. The market, valued at approximately USD 550 billion, is proving remarkably resilient despite global macroeconomic headwinds, currency volatility, and climate-induced disruptions to crop yields.

The successful feed companies of 2026 and 2034 will be those that effectively balance operational efficiency (optimizing feed conversion ratios and lowering costs) with technological innovation (AI-driven formulation, gut microbiome engineering, and alternative proteins). As the industry further regionalizes and consolidates, stakeholders must prioritize supply chain transparency and adopt sustainable, regenerative ingredient sourcing not merely as a corporate social responsibility goal, but as a fundamental competitive necessity. By embracing data-driven procurement and precision nutrition, producers will not only navigate the current volatility but will emerge as essential, high-tech partners in the global food security architecture.

Related Reports

As the industry shifts from the high-inventory dynamics of previous years toward a tighter global supply-demand balance, understanding the current agricultural landscape is critical. Our Global Crops and Grains Market 2026 Report provides a data-driven look at the production trajectories, fertilizer cost pressures, and logistical challenges defining the current marketing year.

With the total addressable nut ecosystem now exceeding USD 200 billion, stakeholders are navigating a landscape defined by climate-resilient farming and shifting consumer preferences. Explore the full data, including segment growth for nut milks and butters, in the Global Nuts Industry Report 2026.

Frequently Asked Questions (FAQ)

What is the biggest driver of the animal feed market in 2026?

The primary driver is the rising global demand for high-quality animal protein (meat, dairy, and aquaculture products) in emerging economies, coupled with a shift toward industrial-scale, commercial feed production to maximize growth efficiency and immune health.

How is technology impacting feed formulation?

Feed formulation has moved from “least-cost” to “precision nutrition.” Companies are now using AI, real-time sensors, and computational modeling to tailor feed to specific species, ages, and production environments, which reduces waste and maximizes nutritional bioavailability.

Why is sustainability becoming a core requirement?

Sustainability is now a regulatory and commercial necessity. Investors and retail partners increasingly demand low-carbon footprints, regenerative agriculture sourcing, and circular economy approaches (upcycling byproducts) to minimize the environmental impact of livestock and aquaculture production.

What are the main challenges for feed manufacturers this year?

Producers face a “triple threat” of volatile raw material prices, persistent global economic inflation, and disease pressures (such as avian influenza). This requires robust procurement strategies and heightened investment in biosecurity and immunity-boosting additives.

Sources and References

Primary Market Intelligence Sources

- Fortune Business Insights: Global Animal Feed Market Outlook 2034

- Alltech 2026 Agri-Food Outlook: Global Feed Production Survey

- Persistence Market Research: Animal Feed Market Share and Trends Analysis

- Global Market Insights: Animal Feed Enzymes Market Analysis 2026-2035

Strategic & Industry Perspectives

- Kemiex: The Future of Animal Nutrition: Trends to Watch in 2026

- MBRF Ingredients: Animal Nutrition Trends 2026

- CSG Talent: Innovation and Growth in the Future of Feed

- Fastmarkets: Navigating Volatility in Global Feed Markets

- FAO (2026): Drivers of supply and demand of terrestrial animal source food