Forecast for Yellow Broiler Production Remains Stable

Date: March 5, 2025

Read Time: 1 Minute

The outlook for chicken meat production in 2025 indicates a slight growth, albeit at a reduced rate compared to the revised estimates for 2024. This information stems from a recent report published by the U.S. Department of Agriculture (USDA) through its Global Agricultural Information Network (GAIN).

The projections for yellow broiler production remain steady. However, the growth trajectory for white broiler production has exhibited signs of deceleration. In response to the evolving demand for chicken meat—particularly for white broilers—producers are adjusting their output levels accordingly.

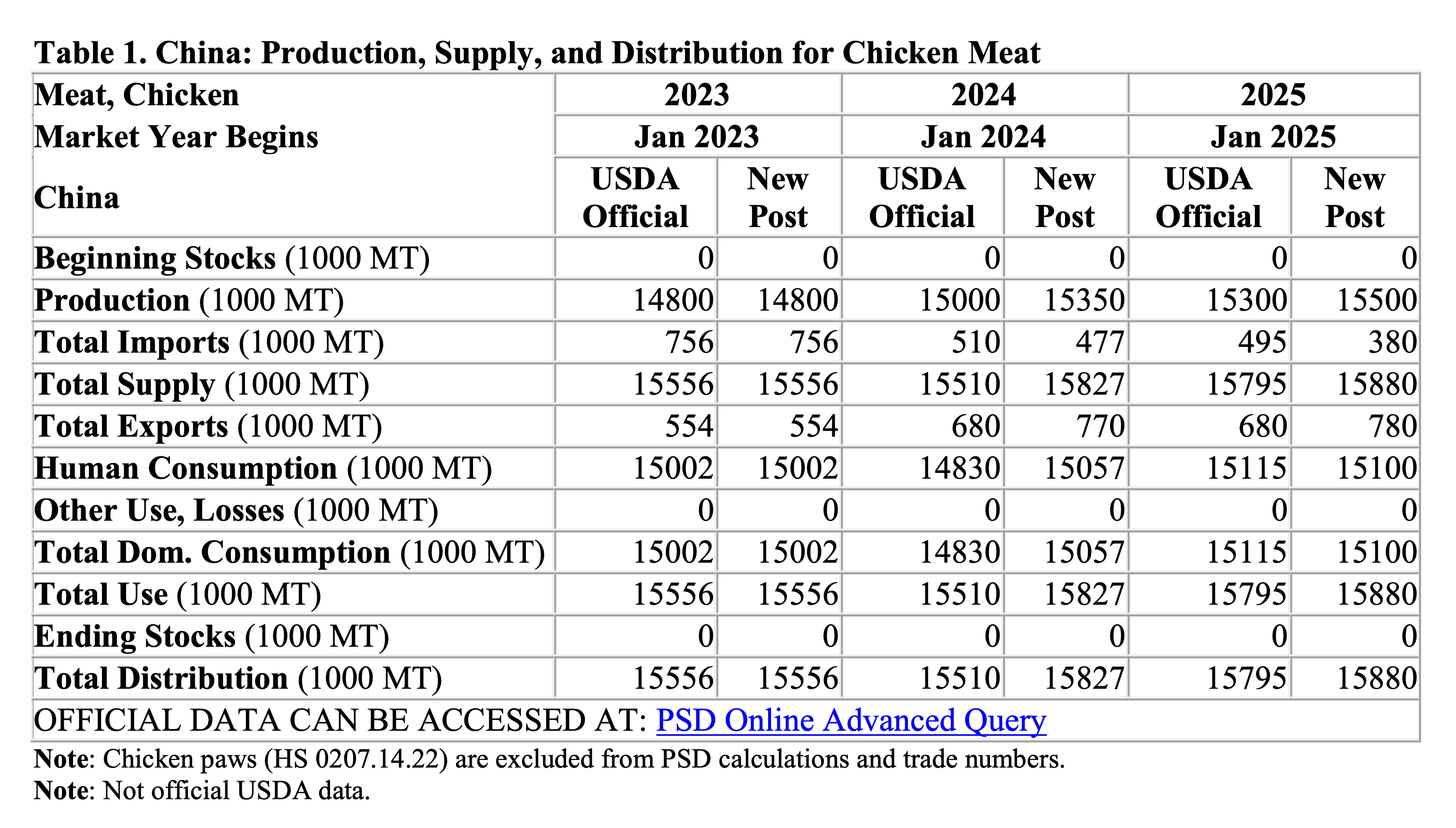

In a recent upward revision, the USDA post in China has adjusted its chicken meat production estimates for 2024. This revision is supported by reports that both large-scale and small-scale producers have increased their white broiler production during the year. Notably, large-scale producers, often characterized as integrated operations, have expanded their production capacity at rates that surpass those of smaller producers. Factors contributing to this expansion include increased sales, economies of scale, market share gains, and a decrease in feed costs. Many publicly listed poultry producers reported robust performances in their 2024 annual reports and are poised to continue their expansion efforts in 2025 to further capture market share.

Despite the optimistic production forecasts, the pricing landscape for chicken meat in 2024 has experienced a decline, primarily due to production outpacing consumption. This oversupply has led to financial challenges for some smaller producers, particularly those with lower production efficiencies, resulting in operational losses.

The financial pressures stemming from reduced profits and business losses in 2024 seem to be influencing the decisions of these smaller producers as they consider their production plans for 2025. The upcoming year is expected to see the commissioning of several new facilities, primarily focused on broiler slaughter and chicken processing. In contrast, the establishment of new breeding facilities remains limited.

As the industry navigates these dynamics, the focus will likely remain on optimizing production efficiencies and adapting to market demands. The interplay between supply, demand, and pricing will continue to shape the strategies of producers, influencing their decisions on whether to expand or consolidate their operations.

The poultry sector, particularly the broiler segment, is at a crucial juncture. Producers are tasked with balancing the need for increased output to meet consumer demand while also managing the economic realities of a competitive landscape. The successful navigation of these challenges will be essential for sustaining growth and profitability in the years to come.

In summary, while the forecast for yellow broiler production remains stable, the slower pace of growth in white broiler production reflects the complexities of the current market environment. Producers are encouraged to adopt strategic approaches that align production capabilities with consumer preferences while remaining vigilant to the broader economic factors at play in the poultry industry.

Related Analysis: View Previous Industry Report