June 9, 2026

The global Food and Beverage Warehousing and Storage Industry was valued at USD 234.06 billion in 2024 and is projected to reach USD 569.07 billion by 2033 at a CAGR of 10.2%. The broader food and beverage warehousing universe — when measured across all temperature zones, storage types, and value-added services — is estimated at USD 457.1 billion in 2024, growing toward USD 1.0 trillion by 2030 at a CAGR of 14.5%. The global warehouse automation market serving food and beverage is projected to reach USD 55 billion by 2030 at a CAGR of 15%.

Warehousing and storage is the still heart of the global food and beverage supply chain. It is the strategic buffer between the speed of production and the pace of consumption — the place where agricultural harvests are preserved, finished goods inventoried, imports consolidated, e-commerce orders assembled, and food safety standards enforced before product reaches a retailer’s shelf, a foodservice operator’s kitchen, or a consumer’s doorstep. Without warehousing, just-in-time production would be impossible, seasonal food security unachievable, global food trade impractical, and the promise of 24-hour grocery delivery a fantasy.

In 2026, the global Food and Beverage Warehousing and Storage Industry industry is undergoing its most consequential transformation in history. Driven simultaneously by labour shortages, rising energy costs, e-commerce demand for speed, food safety regulatory intensification, and the extraordinary growth of biologics and pharmaceutical cold chain requirements, warehousing is transitioning from a passive storage function to an active, intelligent, automated, and data-driven operation at the centre of supply chain competitiveness.

The defining technologies of this transformation — automated storage and retrieval systems (ASRS), autonomous mobile robots (AMRs), AI-powered warehouse management systems (WMS), IoT sensor networks, blockchain traceability platforms, and the micro-fulfilment centres proliferating across urban supply chains — are not incremental improvements to an existing model. They represent the architectural redesign of the food warehouse from the ground up.

This report provides the most comprehensive publicly available analysis of the global food and beverage warehousing and storage industry in 2026 — covering market scale, warehouse types and segments, cold storage infrastructure, warehouse automation, technology and AI, food safety and compliance, sustainability, regional dynamics, key challenges, strategic outlook, and leading companies.

Executive Summary: The 2026 F&B Warehousing Landscape

The global Food and Beverage Warehousing and Storage Industry in 2026 is defined by a “smart warehouse” imperative — the irreversible transition from manually operated, paper-based, labour-intensive storage facilities to fully integrated, data-connected, robotically optimised operations that deliver higher throughput, lower error rates, better food safety compliance, and materially lower cost per unit than their conventional predecessors.

Key Takeaways for Stakeholders:

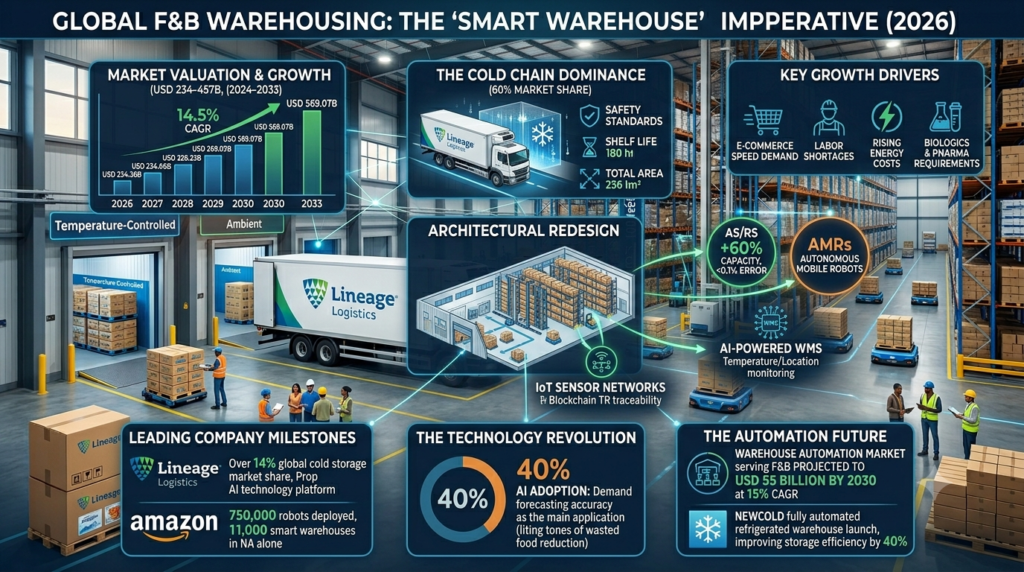

The global F&B warehousing market is valued at USD 234–457 billion in 2024, growing at a CAGR of 10.2–14.5% toward USD 569 billion to USD 1.0 trillion by 2030–2033, making it one of the fastest-growing infrastructure sectors in the global food economy.

Cold chain storage commands 60% of food warehouse operations — close to 60% of industry operations utilise temperature-controlled warehouses to uphold safety standards and extend shelf life.

ASRS installations can increase storage capacity by 60% and reduce error rates to less than 0.1%, making them the highest-ROI technology investment in the food warehouse sector.

AI is already the second most implemented technology in the food industry at 40% adoption, with demand forecasting accuracy as the primary application. In an industry where the cost of error is measured in tonnes of wasted food, AI-driven demand forecasting is the highest-value operational investment available.

45% of F&B warehouse facilities have adopted intelligent tracking and monitoring tools — IoT-based systems improving inventory management, operational accuracy, and supply chain visibility.

Lineage Logistics commands over 14% global cold storage market share with more than 3.0 billion cubic feet of capacity, having transitioned from a real estate company into a technology platform through its proprietary AI systems.

NewCold launched a fully automated refrigerated warehouse in North America, improving storage efficiency by 40%, setting the benchmark for the industry’s automation future.

Amazon leads smart warehouse deployment with 750,000 robots deployed across its facilities, deploying over 11,000 smart warehouses in North America alone.

Table of Contents

1. Market Overview: Scale, Structure and Scope

Defining Food and Beverage Warehousing

Food and beverage warehousing encompasses the full spectrum of storage, handling, and distribution infrastructure designed to receive, store, manage, and dispatch food and beverage products through the supply chain. It encompasses:

Ambient warehousing — storage of shelf-stable, non-perishable food and beverage products (canned goods, packaged snacks, dry grocery, beverages in ambient-stable formats) at room temperature, typically 15°C–25°C.

Chilled warehousing — storage of fresh, short shelf-life food products (fresh dairy, prepared meals, fresh produce, deli products, fresh meat and fish) at 0°C–8°C.

Frozen warehousing — storage of frozen food products (frozen meals, ice cream, frozen meat and seafood, frozen vegetables) at −18°C to −25°C.

Ultra-cold warehousing — storage of pharmaceutical products, biologics, and mRNA vaccines at −60°C to −90°C, a rapidly growing segment driven by the biological medicine revolution.

Controlled atmosphere storage — specialised warehousing for fresh produce (apples, pears, vegetables) where oxygen, carbon dioxide, and nitrogen levels are controlled to slow ripening and extend shelf life.

Bulk liquid storage — dedicated tank farms for edible oils, liquid dairy ingredients, wine, spirits, beverage concentrates, and other liquid food and beverage commodities.

Hazardous and regulated storage — specialised facilities for alcohol, certain food additives, and regulated agricultural inputs.

Global Market Valuation

The food and beverage warehousing market is one of the largest and most rapidly growing infrastructure segments in the global food economy. GII Research places the Food & Beverage Warehousing Market at USD 218.59 billion in 2024, growing at a CAGR of 13.73% to USD 476.44 billion by 2030. Global Industry Analysts estimates the market at USD 457.1 billion in 2024, growing to USD 1.0 trillion by 2030 at a CAGR of 14.5%. Business Research Insights estimates the market at USD 234.06 billion in 2024, projected to reach USD 569.07 billion by 2033 at a CAGR of 10.2%.

The ReAnIn market analysis provides a specific structural insight: close to 60% of industry operations utilise temperature-controlled warehouses, nearly 45% of facilities have adopted intelligent tracking and monitoring tools, and sustainability is increasingly influencing warehousing strategies with over half of new warehouse builds designed with sustainability credentials.

Industry Structure

The food and beverage warehousing industry is moderately concentrated at the top — dominated by a small number of very large specialist operators with the capital, technology capability, and geographic reach to serve major food manufacturers, retailers, and distributors on a national and global scale — while the broader market is highly fragmented, with thousands of regional, specialist, and in-house operations serving specific geographies, product categories, or customer bases.

Lineage Logistics and Americold collectively control a majority of national refrigerated warehouse cubic footage in the United States, creating a quasi-duopoly in metropolitan cold storage markets. In automated ambient warehousing, Ocado’s warehouse technology platform is setting the global standard, while Amazon’s deployment of 750,000 robots across its fulfilment and distribution network represents the largest single warehouse automation programme in the world.

Public warehousing — where the operator rents space per pallet to multiple tenants and typically provides handling and distribution services — is the dominant model for cold storage, with Americold and Lineage dominating this segment. Private warehousing — operated exclusively by a single food manufacturer or retailer for their own products — is the dominant model for the largest food companies whose volume and operational specificity justify dedicated facilities.

2. Warehouse Types: Deep Dives

Cold Storage Warehousing: The Market’s Largest Segment

Cold storage warehousing is the largest and fastest-growing segment of the food and beverage warehousing market. Dairy and frozen desserts represent the largest application at 55% of food cold chain warehousing demand in 2026, driven by strict temperature control requirements, high shipment frequency, and the short shelf-life of dairy products. Meat, fish, and seafood warehousing is projected to grow at a 16.0% CAGR — the fastest of any F&B warehousing sub-segment — driven by the global growth in protein consumption, the expansion of refrigerated protein export trade, and the increasing distance between protein production and consumption centres.

Cold-chain storage led with 55.66% of the food cold chain market share in 2024. Chilled storage (0–4°C) captured 60.15% of revenue share in 2024, whereas frozen (−18°C) storage is poised for the fastest growth at a 15.49% CAGR through 2030, driven by the global expansion of frozen food consumption and the growth of frozen food e-commerce.

The cold storage market is experiencing a wave of investment. Americold announced a USD 45 million expansion of its Dalgety site in New Zealand, increasing capacity by approximately 4.6 million cubic feet and 27,000 pallet positions. NewCold launched a fully automated refrigerated warehouse in North America, improving storage efficiency by 40% compared to conventional cold storage operations. VersaCold Logistics Services announced a 30% expansion of its North American cold storage network to meet increasing demand from online grocery distribution.

Ambient Dry Warehousing

Ambient dry warehousing — the storage of shelf-stable food and beverage products — is the largest segment by facility count globally, encompassing billions of square metres of storage space serving every link in the food supply chain from post-harvest grain storage to finished goods distribution. The segment is being transformed by e-commerce, which has fundamentally changed the warehouse picking model from pallet-in/pallet-out to individual item picking at a scale that conventional ambient warehouses were not designed to support.

The rise of online grocery and quick commerce has created demand for urban-adjacent micro-fulfilment centres — small, highly automated facilities positioned within 2–5km of high-density consumer demand — that combine ambient and chilled storage with automated picking systems capable of assembling individual grocery orders with the speed required by same-day and hour-delivery promises.

Controlled Atmosphere Storage

Controlled atmosphere (CA) storage — where the gas composition around fresh produce is actively managed to slow biochemical aging and extend shelf life — is the critical technology enabling the global trade of premium fresh fruit and vegetables across hemispheres and seasons. Apple producers in New Zealand can supply European retailers year-round; Chilean table grapes reach consumers across the globe at peak quality many months after harvest; South African citrus reaches Northern European supermarkets in premium condition.

The controlled atmosphere technology is advancing: dynamic controlled atmosphere (DCA) systems that continuously monitor individual produce lots and adjust conditions in real time are enabling shelf-life extensions of 20–30% compared to conventional CA storage, with corresponding reductions in food waste and improvements in product quality at retail.

Bonded and Customs Warehousing

Bonded warehousing — government-licensed facilities where imported food and beverage products can be stored under customs control before duty payment, enabling importers to defer duty liability until the point of sale — is an important segment of the food and beverage warehousing market for international food traders, importers, and distributors. For imported wines, spirits, and premium food products, bonded warehousing provides the financial flexibility to hold inventory without the cash flow burden of immediate duty payment.

3. Warehouse Automation: The Technology Revolution

The Scale of the Investment Wave

The global warehouse automation market is projected to reach USD 55 billion by 2030 at a CAGR of 15% between 2024 and 2030. Food and beverage is one of the primary drivers of this growth, as the sector’s unique combination of high volume, high product variety (SKU complexity), strict food safety requirements, temperature-sensitive handling, and intense labour market competition makes it one of the most compelling use cases for warehouse automation investment.

In 2026, companies are no longer looking for isolated equipment upgrades. Instead, they are building connected automation ecosystems that improve storage density, material flow, and operational visibility across the entire facility. Technologies including ASRS, shuttle systems, warehouse robotics, and integrated software platforms are helping food manufacturers and distributors create faster, more scalable, and more resilient logistics operations.

Automated Storage and Retrieval Systems (ASRS)

ASRS — computer-controlled systems that automatically place and retrieve goods from defined storage locations using robotic cranes, shuttle systems, vertical lift modules, or carousel systems — are the cornerstone technology of warehouse automation, offering the highest density storage and most reliable retrieval performance of any warehousing technology. ASRS installations can increase storage capacity by 60% and reduce error rates to less than 0.1%, making them particularly effective in cold storage, where their ability to operate continuously in sub-zero temperatures without the labour limitations that constrain manual cold storage is especially commercially valuable.

NewCold uses ASRS systems across its automated cold warehouses, achieving throughput rates that conventional cold storage facilities simply cannot match. The technology enables fully frozen facilities to operate with minimal human presence in the low-temperature environment, addressing both the labour shortage and the health and safety challenge of extended working in frozen environments.

For food manufacturers investing in ASRS, the ROI case is increasingly compelling: reduced labour costs, improved pick accuracy (reducing costly mispicks and customer claims), better inventory visibility, and the ability to serve e-commerce omnichannel demand at the speed consumers now expect.

Autonomous Mobile Robots (AMRs) and AGVs

Autonomous Mobile Robots — sophisticated robots using AI and sensors to navigate warehouses independently and transport goods between storage locations, picking stations, and dispatch docks — are transforming the warehouse labour model. Unlike their predecessors, Automated Guided Vehicles (AGVs), which require fixed guidance infrastructure (wires, reflective markers), AMRs navigate dynamically using onboard computing and sensor fusion, making them adaptable to changing warehouse layouts and product mixes.

Lineage Logistics uses AGVs to handle goods within its cold storage facilities, ensuring exact and fast movement while protecting workers from extended exposure to sub-zero environments. Amazon leads globally with 750,000 robots deployed across its network, reducing labour costs by 3% annually and achieving a 40% improvement in shipment-within-one-day performance.

Collaborative robots (cobots) — robots designed to work alongside human workers rather than replacing them — are emerging as an adaptable solution for dynamic food warehouse environments where full automation is economically unjustified but labour support is commercially valuable. Cobots handle the physically demanding, repetitive tasks — heavy lifting, repetitive picking, pallet building — while human workers handle the judgement-intensive tasks that robot technology cannot yet reliably perform.

AI-Powered Warehouse Management Systems

AI orchestrates warehouse robots for picking, sorting, and inventory management, reducing processing times by up to 60%. Computer vision powered by AI inspects inventory and detects errors or defects. AI-driven inventory management and predictive analytics reduce waste, improve demand forecasting accuracy, and ensure the right products are available at the right time.

In the food industry, AI is already the second most implemented technology at 40% adoption, with demand forecasting accuracy as the primary application. The cost of forecasting error in food warehousing is measured in tonnes of wasted food, immobilised working capital, and lost sales — making AI-powered demand forecasting the highest commercial value application of AI in the food supply chain. Machine learning algorithms that refine ordering and inventory positioning decisions, reducing overstock and stockouts simultaneously, are delivering measurable financial benefits that justify the investment.

Supply Chain Management systems (SCMs) are increasingly adopted at 32% penetration because they allow integration of demand planning, inventories, purchasing, and logistics — enabling companies to synchronise supply with real demand rather than suffering the stock failures that misalignment between these functions creates.

The Smart Warehouse: IoT, Digital Twins and 5G

Smart warehouses — powered by IoT sensors, AI analytics, real-time tracking devices, and increasingly 5G connectivity — represent the architectural endpoint of the warehouse automation investment wave. Sensors, RFID tags, and real-time tracking devices monitor inventory, equipment, and environmental conditions. IoT enables predictive maintenance, reducing downtime and energy consumption. Real-time data improves decision-making and reduces stock discrepancies. Drones assist with 24/7 inventory counts, improving efficiency and reducing errors.

The global IoT in logistics market is expected to reach USD 63.73 billion by 2026, while the global IoT in warehouse management market is estimated to grow from USD 12.13 billion in 2023 to USD 27.79 billion by 2030. For food and beverage warehousing, IoT’s most critical applications are temperature monitoring (continuous documentation of cold chain compliance), inventory tracking (real-time visibility of stock levels and locations), and predictive maintenance (anticipating equipment failures before they cause temperature excursions or operational disruptions).

Digital twin technology — creating a virtual replica of the physical warehouse that enables scenario modelling, layout optimisation, and performance simulation — is being deployed by the most advanced food warehouse operators to continuously optimise their physical operations without disrupting actual warehouse throughput.

4. Food Safety and Regulatory Compliance

FSMA and the Traceability Mandate

The US Food Safety Modernization Act Section 204 Food Traceability Final Rule — which requires companies handling foods on the FDA’s Food Traceability List to maintain key data elements in electronic records across the supply chain — is creating the most significant compliance investment requirement in the US food warehousing industry in decades. The rule mandates traceability record-keeping at every point of the supply chain, including during storage and handling in warehouses, effectively requiring warehouse operators serving covered food categories to implement electronic record systems capable of providing the required traceability documentation.

45% of facilities have adopted intelligent tracking and monitoring tools, but this means 55% are still operating without the comprehensive real-time monitoring capability that FSMA-compliant operations require. The compliance investment required to bring legacy warehouse facilities into full electronic traceability compliance is significant and is driving adoption of warehouse management systems with built-in FSMA-compliant record-keeping capability.

HACCP and Food Safety Standards

HACCP (Hazard Analysis and Critical Control Points) — the systematic, science-based food safety framework that identifies physical, chemical, and biological hazards in food handling and establishes preventive controls — is the universal baseline standard for food warehouse operations globally. In the US, FSMA’s Preventive Controls requirements effectively codify HACCP principles into federal law for food facilities including storage warehouses. In the EU, food safety regulations require equivalent HACCP-based systems.

For automated food warehouses, HACCP implementation benefits from the digital data streams generated by IoT sensors and warehouse management systems — continuous temperature monitoring, electronic lot tracking, automated date rotation, and real-time inventory visibility all contribute to a HACCP-compliant operating environment that is impossible to replicate at equivalent reliability through manual systems.

Cold Chain Compliance Documentation

In the pharmaceutical cold chain, GDP (Good Distribution Practice) requires continuous monitoring with documented records for all pharmaceutical products. The DSCSA (Drug Supply Chain Security Act) requires package-level electronic tracking of prescription drugs throughout the supply chain including during warehousing. For food warehousing serving pharmaceutical clients — a growing opportunity as biologics storage requirements expand into the food cold chain infrastructure space — GDP compliance is the gateway to accessing this high-margin market segment.

United States Cold Storage introduced a blockchain-based cold chain tracking system, enhancing traceability by 45% and creating an immutable audit trail that satisfies both food safety and pharmaceutical regulatory requirements. Burris Logistics implemented AI-driven warehouse management software, improving inventory accuracy by 35%.

5. Sustainability: The Green Warehouse Imperative

Energy: The Cold Storage Challenge

Energy consumption represents approximately 50% of cold storage warehouse operating costs — making energy the single largest variable cost in cold chain warehousing and the primary target for both cost reduction and sustainability programmes. Cold storage facilities consume approximately 10–15% of all US commercial energy. The challenge of reducing energy consumption in cold storage is particularly acute because refrigeration is a continuous, non-deferrable energy demand — the warehouse cannot choose to stop cooling when energy prices spike without risking food safety and product quality.

Nichirei Logistics Group introduced low-energy refrigeration technology, reducing electricity consumption by 25% in its Japanese facilities. Tippmann Group invested in solar-powered cold storage systems, reducing carbon emissions by 50% in newly developed warehouses. The combination of solar generation, battery storage, and smart energy management systems is enabling some cold storage facilities to approach energy self-sufficiency during peak solar generation periods.

Natural Refrigerants and HFC Phase-Out

Conventional cold storage refrigeration systems use HFC (hydrofluorocarbon) refrigerants with high global warming potential that are being phased out under the Kigali Amendment to the Montreal Protocol. The transition to natural refrigerants — ammonia (NH3), CO2 (R744), and propane (R290) — offers dramatic reductions in refrigerant global warming potential while delivering improved energy efficiency in many configurations. The capital cost of retrofitting existing cold storage infrastructure with natural refrigerant systems is significant, but new-build cold storage facilities are increasingly designed with natural refrigerants as the default.

25% lower energy consumption via new refrigerant systems is being achieved across the most advanced new-build cold storage facilities, according to industry analysis. AGRO Merchants Group and Kloosterboer are investing specifically in energy-efficient technologies to reduce their operational carbon footprints as customer sustainability requirements tighten.

Green Building Standards

Over 60% of new food warehouse builds are incorporating sustainability credentials — solar panels, LED lighting, rainwater harvesting, green roofing, and high-efficiency building envelopes that reduce heating and cooling loads. The most advanced new food warehouse developments are targeting BREEAM (Building Research Establishment Environmental Assessment Method) or LEED (Leadership in Energy and Environmental Design) certification as a baseline commercial requirement for the most demanding food manufacturer and retailer clients.

Shift toward eco-friendly warehousing is increasingly influencing warehousing strategies, with nearly 45% of facilities adopting higher sustainability standards in their operational practices. For food companies with ambitious Scope 3 emissions targets, the carbon intensity of their warehousing infrastructure is an increasingly visible component of their overall supply chain sustainability profile.

Food Waste Reduction Through Better Warehouse Management

Data-driven platforms give customers better visibility into inventory and supply-chain activity, helping them make more informed decisions about production, storage, and movement. That kind of insight can limit excess handling and dwell time, which ultimately reduces food and energy waste across the network while strengthening service levels and responsiveness. AI-driven inventory management and predictive analytics are reducing waste, improving demand forecasting, and ensuring the right products are available at the right time — not only cutting costs but enhancing sustainability by minimising overstock and spoilage.

Excess inventory accumulates more merchandise than necessary, immobilising working capital and dramatically increasing the risk of loss due to maturity — a “silent cost” that directly attacks profit margins. AI-powered demand forecasting that reduces excess inventory directly reduces food waste, energy consumption (less product to keep refrigerated), and the associated carbon emissions.

6. Regional Dynamics

North America: Technology and Capacity Leadership

North America holds 35% of the global refrigerated warehouse market share, driven by e-commerce grocery growth, pharmaceutical storage demand, and the sustained investment programmes of Lineage Logistics and Americold. The US cold storage market alone is estimated at USD 97 billion in 2026, with Lineage and Americold collectively controlling a majority of major metropolitan refrigerated warehouse capacity.

The US food warehousing market is characterised by a technology bifurcation: the largest operators are deploying cutting-edge automation, AI, and IoT at scale, while smaller regional operators — often operating ageing facilities — are struggling to compete on cost, service level, and compliance capability. This bifurcation is driving industry consolidation as smaller operators either upgrade through capital-intensive technology investment or are acquired by larger operators with the capital and expertise to modernise their facilities.

Amazon’s deployment of over 750,000 robots across more than 11,000 smart warehouses in North America represents the most aggressive warehouse technology investment in the world and is setting consumer delivery speed expectations that every food distributor, retailer, and e-commerce operator must compete against.

Asia-Pacific: The Growth Powerhouse

Asia-Pacific holds 30% of the global refrigerated warehouse market share and is growing at the fastest CAGR of any major region — driven by the extraordinary food cold chain investment requirements of China and India, the rapid expansion of organised food retail and e-commerce across Southeast Asia, and the pharmaceutical cold chain investment driven by the biological medicine revolution across the region.

China’s food and beverage warehousing market is forecast to reach USD 261.5 billion by 2030 at a CAGR of 18.8% — the highest growth rate of any single national market globally — driven by the transition from traditional wet market and unpackaged food distribution toward modern cold chain-dependent food retail. Americold Logistics acquired two major cold storage facilities in Asia-Pacific, increasing its regional storage capacity by 30%, reflecting the investment commitment required to capture Asia-Pacific market growth.

India represents one of the most significant emerging food warehousing growth markets globally, with organised cold chain capacity dramatically underdeveloped relative to the country’s food production and consumption scale. The Indian government’s National Cold Chain Policy and substantial infrastructure investment is creating the framework for rapid cold chain development, and private sector investment — from both domestic operators like Snowman Logistics and international companies including Lineage and Americold — is accelerating.

Japan, home to Nichirei Logistics Group — one of the world’s most sophisticated cold chain operators — leads Asia in cold storage technology quality, with Nichirei’s facilities representing global benchmarks for energy efficiency, automation, and pharmaceutical-grade quality standards.

Europe: Sustainability Leadership and Regulatory Sophistication

Europe holds 25% of the global refrigerated warehouse market, characterised by the highest sustainability and food safety regulatory standards globally and the most sophisticated application of controlled atmosphere storage for premium fresh produce. European cold storage operators — particularly in the Netherlands (Kloosterboer), Germany, and the UK — are deploying the most energy-efficient refrigeration systems and achieving some of the lowest carbon intensities per pallet position of any major global market.

The EU’s Farm to Fork strategy is creating direct pressure on the food warehousing industry to reduce food waste, improve energy efficiency, and adopt sustainable refrigerants, with regulatory timelines that are driving capital investment ahead of compliance deadlines.

7. Micro-Fulfilment: The Urban Warehousing Revolution

The MFC Model

Micro-fulfilment centres — small, highly automated warehousing facilities positioned within or adjacent to urban population centres, typically 1,000–5,000 square metres — represent the most architecturally innovative development in food warehousing in 2026. MFCs combine ambient and chilled storage with automated picking systems capable of assembling individual grocery orders at the speed required for same-day and sub-one-hour delivery. By positioning inventory within 2–5km of high-density consumer demand, MFCs dramatically reduce last-mile delivery distances and enable the delivery economics that quick commerce operators promise.

The Ocado Smart Platform — the world’s most advanced automated grocery fulfilment technology, licensed to retailers including Kroger (US), ICA (Sweden), Sobeys (Canada), and others — represents the large-scale, purpose-built MFC at its most sophisticated, deploying robotic grid systems where hundreds of robots simultaneously retrieve products from a three-dimensional storage structure to assemble grocery orders in minutes with extraordinary accuracy.

VersaCold Logistics Services announced a 30% expansion of its North American cold storage network specifically to meet increasing demand for online grocery distribution, recognising that the e-grocery growth wave requires cold storage infrastructure positioned close enough to consumer demand to support sub-2-hour delivery economics.

8. Bulk Liquid Storage: The Beverage Industry’s Foundation

Market and Scope

The food-grade liquid bulk storage sector — encompassing the dedicated tank farms, ISO tanks, and specialised tank vehicles used for edible oils, liquid dairy ingredients, wine, spirits, beverage concentrates, and other liquid food commodities — is a commercially significant and technically specialised segment of food and beverage warehousing. The global food-grade liquid bulk transportation and storage market is projected to grow from approximately USD 15 billion in 2025 to USD 23 billion by 2033 at a CAGR of 6.2%.

Bulk liquid food storage requires specialised materials (food-grade stainless steel, polyethylene, or FDA-approved coatings), cleaning and sanitation systems (clean-in-place, CIP), temperature management (heating or cooling depending on product), and segregation systems that prevent cross-contamination between different product types.

The wine and spirits storage sector — bonded warehouse facilities that hold bulk wine, spirits, and finished cases under customs control — is an important segment of the premium food and beverage storage market, serving the global wine trade’s requirement for extended maturation storage and the spirits industry’s ageing programmes that are foundational to brand identity for Scotch whisky, bourbon, cognac, and other aged spirits.

9. Critical Risks and Challenges

Labour Shortages in Extreme Environments

The food warehousing industry’s labour challenge is acute and structural. Cold storage environments — particularly frozen facilities at −25°C — are physically demanding, regulated by maximum exposure times, and increasingly unattractive to candidates who have better-compensated, less demanding alternatives. The industry’s response — automation — is capital-intensive and takes time to implement. In the interim, labour shortages are creating throughput constraints and operational cost increases across the food cold storage network.

In ambient warehousing, the labour challenge is different but equally significant: the volume of individual item picking required by e-commerce grocery creates demand for picking labour at a rate that traditional warehouse staffing models cannot sustainably supply. Warehouse picker roles are physically demanding, repetitive, and subject to the same labour market competition that is tightening across all manual labour categories.

Energy Price Volatility and Grid Reliability

Cold storage’s non-deferrable energy demand creates disproportionate exposure to energy cost volatility. A sudden energy price spike cannot be absorbed by temporary refrigeration reduction without risk to stored product. Power reliability issues affect 55% of cold storage facilities according to industry surveys, reflecting the challenge of maintaining uninterrupted refrigeration across facilities of varying age and in regions with varying grid reliability. The 45% higher investment required for green technology solutions creates a capital cost barrier that smaller operators struggle to overcome.

Ageing Infrastructure and the Retrofit Challenge

A significant proportion of existing food warehouse infrastructure — particularly in North America — was built in the 1970s–1990s using construction standards, insulation technologies, and refrigeration systems that are dramatically less efficient than modern equivalents. Retrofitting these facilities with modern automation, natural refrigerants, and high-efficiency insulation is complex, expensive, and disruptive. 35% of cold storage facilities use outdated systems, creating a structural efficiency disadvantage relative to new-build facilities.

Demand Forecasting Accuracy: The “Silent Cost” Challenge

The difficulty in predicting demand creates instability throughout warehouse operations — affecting 52% of food supply chain companies as a top operational challenge. Lack of precision about how much and when to supply prevents efficient planning. In an industry governed by expiration dates, incorrect forecast directly translates into decline or lost sales. Excess inventory (affecting 44% of companies) and product obsolescence (affecting 40%) appear as critical interconnected challenges, accumulating more merchandise than necessary while immobilising working capital and dramatically increasing the risk of loss due to product maturity.

10. Strategic Outlook for Stakeholders

Actionable Recommendations

Treat Automation Investment as Infrastructure, Not Equipment: The food and beverage warehousing companies achieving the best commercial outcomes in 2026 are those who have moved from evaluating individual automation technologies to designing connected automation ecosystems — integrating ASRS, AMRs, WMS, and IoT monitoring into a unified operational architecture. The ROI from each individual technology is strengthened when it operates as part of an integrated system; a best-in-class ASRS connected to a mediocre WMS will underperform a well-integrated moderate ASRS with a sophisticated WMS.

Invest in AI Demand Forecasting Before Energy and Waste Costs Make It Unavoidable: AI-powered demand forecasting is the highest-ROI technology investment available in food and beverage warehouse management — reducing both overstock waste and stockout lost sales simultaneously, while reducing the energy wasted keeping excess inventory refrigerated. In an industry where 52% of companies cite demand forecasting accuracy as a top challenge, the competitive advantage from genuine AI-powered forecasting capability is commercially significant and compounding.

Prioritise FSMA Traceability Compliance as a Commercial Capability: FSMA Section 204 electronic traceability requirements are creating a compliance floor that all food warehouses serving covered categories must meet. The most sophisticated operators are treating FSMA traceability not merely as a compliance obligation but as a commercial capability — the real-time lot tracking, temperature documentation, and chain-of-custody record-keeping required for FSMA compliance also enables faster targeted recalls, better customer service, and the provenance transparency that premium retailers and foodservice operators increasingly require as a supplier qualification criterion.

Design New Warehouse Builds for Net-Zero from Day One: The capital cost of retrofitting existing cold storage infrastructure with natural refrigerants, solar generation, battery storage, and high-efficiency insulation is significantly higher than incorporating these features into new-build design. Warehouse operators commissioning new facilities in 2026 should design for net-zero energy intensity from the outset — specifying natural refrigerants, rooftop solar, LED lighting, high-performance insulation, and smart energy management systems as standard rather than optional features.

Strategic Summary: The 2026 F&B Warehousing Business Model

| Strategic Priority | Traditional Model | 2026 Competitive Standard |

|---|---|---|

| Operations Model | Labour-intensive, paper-based | Automated, data-connected, AI-optimised |

| Temperature Management | Manual monitoring, periodic checks | Continuous IoT monitoring with AI anomaly detection |

| Inventory Management | Periodic cycle counting | Real-time RFID/vision-tracked, AI demand-driven |

| Energy Strategy | Grid-dependent, unmanaged | Solar-powered, battery-backed, smart-managed |

| Food Safety Compliance | HACCP documentation manual | Electronic traceability with blockchain audit trail |

| Growth Strategy | Organic capacity expansion | Technology platform consolidation and MFC network |

11. Leading Industry Companies

| Company | Region | Strategic Focus |

|---|---|---|

| Lineage Logistics | USA/Global | World’s largest temperature-controlled warehousing company with over 3.0 billion cubic feet of storage and 14%+ global market share. Proprietary “Lineage Eye” AI platform reducing temperature deviations by 78% in pilot facilities. Uses AGVs for goods handling. Transitioning from real estate to technology platform. |

| Americold Realty Trust | USA/Global | Largest publicly traded cold storage REIT. USD 45 million expansion at Dalgety site (New Zealand). Robotics deployed across facilities for handling efficiency. Acquired two major cold storage facilities in Asia-Pacific, increasing regional capacity by 30%. |

| NewCold Coöperatief UA | Netherlands/Global | Global leader in automated cold chain warehousing. Fully automated refrigerated warehouse launched in North America improving storage efficiency by 40%. ASRS systems across all facilities. Industry benchmark for automated cold warehouse design. |

| Ocado Group | UK/Global | World’s most advanced automated grocery fulfilment technology. Licensing the Ocado Smart Platform — deploying robotic grid systems for MFC operations — to Kroger, ICA, Sobeys, and others globally. Defining the future of automated food warehousing. |

| Amazon | USA/Global | 750,000 robots deployed across 11,000+ smart warehouses. Reducing labour costs by 3% annually. 40% improvement in same-day shipment performance. Potential entry into dedicated food cold storage market identified as major competitive threat. |

| Nichirei Logistics Group | Japan/Asia | Japan’s leading cold chain operator. Low-energy refrigeration technology reducing electricity consumption by 25%. Asian benchmark for energy efficiency and pharmaceutical-grade cold storage quality standards. |

| VersaCold Logistics Services | Canada/North America | 30% expansion of North American cold storage network for online grocery. Strong pharmaceutical storage capability. Focusing on healthcare and food cold chain convergence. |

| AGRO Merchants Group | USA/Europe/Global | Global cold storage specialist focused on sustainability and carbon footprint reduction in warehousing operations. Multi-temperature facilities across multiple continents. |

| Kloosterboer Group | Netherlands/Europe | European leader in port-side cold storage and temperature-controlled logistics. Strong sustainability focus with energy-efficient warehousing technology. Key node in European and global food cold chain import/export infrastructure. |

| Burris Logistics | USA | North American cold chain specialist. AI-driven WMS improving inventory accuracy by 35%. Expanding in Latin America through strategic partnerships. |

Related: As global supply chain volatility persists, the ability to maintain the integrity of perishable goods while optimizing distribution networks has become a critical competitive advantage. Explore the latest advancements in cold-chain technology, digital tracking, and route optimization in our Global Food & Beverage Logistics Industry Report 2026.

Frequently Asked Questions (FAQ)

What is the global food and beverage warehousing market size in 2026?

The global food and beverage warehousing market is valued at approximately USD 234–476 billion depending on scope and research methodology. GII Research estimates the Food & Beverage Warehousing Market at USD 218.59 billion in 2024, growing at a CAGR of 13.73% to USD 476.44 billion by 2030. Business Research Insights estimates USD 234.06 billion in 2024, projected to reach USD 569.07 billion by 2033 at a CAGR of 10.2%. Global Industry Analysts provides the broadest estimate at USD 457.1 billion in 2024, growing to USD 1.0 trillion by 2030 at a CAGR of 14.5%. The wide range of estimates reflects differences in what is included: narrower definitions focus on temperature-controlled storage only, while broader definitions include all ambient and specialised food storage, handling services, and value-added logistics. Close to 60% of food warehouse operations utilise temperature-controlled infrastructure, with dairy and frozen desserts representing the largest cold storage application at 55% of demand.

What is ASRS and why is it transforming food warehousing?

ASRS — Automated Storage and Retrieval Systems — are computer-controlled warehouse systems that automatically place and retrieve goods from defined storage locations using robotic cranes, shuttle systems, vertical lift modules, or carousel systems. They represent the most transformative technology in food warehousing because they simultaneously address the industry’s most acute challenges: ASRS installations can increase storage capacity by 60% (enabling significantly more product in the same facility footprint), reduce error rates to less than 0.1% (dramatically improving picking accuracy), and operate continuously in sub-zero temperatures without the labour limitations that constrain manual cold storage operations. For frozen food warehouses, ASRS is particularly revolutionary — enabling facilities to operate at full throughput in −25°C environments where human workers can only work in short, regulated time periods. NewCold deploys ASRS across all its automated cold warehouses, achieving throughput rates that conventional facilities cannot match. In ambient food distribution, ASRS systems are enabling the rapid individual item picking required to support e-commerce grocery at commercial scale and speed.

What is a micro-fulfilment centre (MFC) and how is it changing food distribution?

A micro-fulfilment centre (MFC) is a small, highly automated warehousing facility — typically 1,000–5,000 square metres — positioned within or adjacent to urban population centres, combining ambient and chilled storage with automated picking systems capable of assembling individual grocery orders with the speed and accuracy required by same-day and sub-one-hour delivery promises. MFCs dramatically reduce last-mile delivery distances by positioning inventory within 2–5km of consumer demand, enabling the sub-2-hour delivery economics that quick commerce platforms require. The Ocado Smart Platform — deploying robotic grid systems where hundreds of robots simultaneously retrieve products from a three-dimensional storage structure — represents the most advanced MFC technology, licensed to major retailers including Kroger, ICA, and Sobeys. MFCs represent a fundamental architectural shift in food warehousing: rather than serving thousands of stores from a single large regional distribution centre, food retailers are building networks of automated mini-warehouses that serve smaller geographic areas with greater speed.

How is AI transforming food and beverage warehouse management?

AI is transforming food and beverage warehouse management across four key dimensions in 2026. First, demand forecasting — AI and machine learning algorithms analyse historical sales data, weather, promotions, seasonality, and economic indicators to predict demand with significantly greater accuracy than conventional statistical methods, reducing both overstock waste and stockout lost sales. AI is already the second most implemented technology in the food industry at 40% adoption, with demand forecasting as the primary application. Second, inventory management — AI-powered systems track inventory in real time, optimise stock positioning across multi-location networks, and automatically trigger replenishment orders before stockouts occur. Third, predictive maintenance — AI analyses sensor data from refrigeration equipment, conveyor systems, and robots to identify failure patterns before equipment breakdown occurs, enabling pre-emptive maintenance that prevents costly operational disruptions. Fourth, warehouse orchestration — AI orchestrates the movement of robots, human workers, and inventory through the facility, optimising throughput, minimising travel distances, and reducing processing times by up to 60%.

What are the biggest sustainability challenges in food warehousing?

Food and beverage warehousing faces four significant sustainability challenges. First, energy consumption — cold storage facilities consume approximately 10–15% of all US commercial energy, and energy represents approximately 50% of cold storage operating costs. Second, refrigerant transition — conventional cold storage uses HFC refrigerants with high global warming potential that must be phased out under international environmental agreements, requiring capital-intensive equipment replacement with natural refrigerant alternatives. Third, food waste generation — inadequate warehouse management including poor demand forecasting, inaccurate inventory tracking, and poor date rotation management generates billions of tonnes of food waste annually from warehouses globally. Fourth, building energy efficiency — ageing warehouse infrastructure with poor insulation, inefficient lighting, and outdated refrigeration systems creates structural energy intensity that is expensive to address through retrofit. The most progressive operators are addressing these through solar-powered facilities achieving 50% carbon emission reductions, natural refrigerant transitions reducing refrigerant GWP dramatically, AI-powered waste reduction programmes, and new-build facilities designed to net-zero standards.

What is the difference between public and private food warehousing?

Public warehousing in the food cold storage sector refers to facilities where the operator rents space per pallet to multiple tenants, typically providing handling, packaging, and distribution services. Americold and Lineage dominate the public cold warehouse space, operating facilities used by hundreds of food manufacturer, retailer, and food service customers. Public warehousing offers food companies the flexibility of variable storage costs (paying only for space used), access to professional logistics expertise without capital investment, and geographic coverage across a national or global network. Private warehousing is operated exclusively by a single food manufacturer or retailer for their own products, offering complete operational control, proprietary process optimisation, and the ability to design the facility specifically for the operator’s product and throughput requirements. The largest food companies — Nestlé, Unilever, Walmart — operate significant private warehouse networks alongside using public warehouse providers for overflow, seasonal, and geographic coverage. Contract warehousing — a hybrid where a third-party operator runs a dedicated facility for a single customer under a long-term contract — is a growing model that combines the customisation advantages of private warehousing with the operational expertise of professional warehouse managers.

Who are the leading food and beverage warehousing companies globally in 2026?

The global food and beverage warehousing industry is led by specialised temperature-controlled warehouse operators and diversified logistics groups. Lineage Logistics is the world’s largest temperature-controlled warehousing company with over 3.0 billion cubic feet of storage capacity and 14%+ global market share, having transitioned from a real estate company to a technology platform through its AI-powered “Lineage Eye” monitoring system. Americold Realty Trust is the largest publicly traded cold storage REIT, operating over 250 facilities globally. NewCold (Netherlands) is the global leader in fully automated cold chain warehouse technology. In automated ambient food fulfilment, Ocado Group’s Smart Platform — licensing robotic grid technology to major retailers — is the global standard-setter. In Asia-Pacific, Nichirei Logistics Group leads in cold chain quality and energy efficiency. In North America, VersaCold Logistics Services, Burris Logistics, AGRO Merchants Group, and United States Cold Storage are the major specialist operators. In Europe, Kloosterboer is the leading port-side cold storage specialist. Amazon — the world’s most aggressive warehouse automation investor — remains the operator whose scale, technology investment, and potential market entry into food cold storage represents the most significant competitive threat to the established food warehousing industry.

Sources and Additional References

- GII Research / ResearchAndMarkets: Food & Beverage Warehousing Market by Storage Type, Facility Size, Component, Technology, Application, End-User — Global Forecast 2025–2030 — https://www.giiresearch.com/report/ires1614427-food-beverage-warehousing-market-by-storage-type.html

- Global Industry Analysts: Food and Beverage Warehousing — Market Research Report 2024–2030 — https://www.marketresearch.com/Global-Industry-Analysts-v1039/Food-Beverage-Warehousing-40763588/

- Business Research Insights: Food and Beverage Warehousing Market Size, Share, 2033 — https://www.businessresearchinsights.com/market-reports/food-and-beverage-warehousing-market-103179

- ReAnIn: Food and Beverage Warehousing Market Size & Share — https://www.reanin.com/reports/food-and-beverage-warehousing-market

- Knowledge Sourcing Intelligence: Food and Beverage Warehousing Market — Global Forecast to 2030 — https://www.knowledge-sourcing.com/report/global-food-and-beverage-warehousing-market

- PRNewswire / Technavio: Food and Beverage Warehousing Market to Grow by USD 508.7 Billion 2024–2028 — https://www.prnewswire.com/news-releases/food-and-beverage-warehousing-market-to-grow-by-usd-508-7-billion-2024-2028-as-warehouse-automation-increases-with-ai-driving-market-transformation–technavio-302275363.html

- Custom Market Insights: Global Warehousing Market Size, Trends, Share 2026–2035 — https://www.custommarketinsights.com/report/warehousing-market/

- Research and Markets: Food & Beverage Warehousing Market by Product Category, Temperature Control, Service Type, Ownership Type — https://www.researchandmarkets.com/reports/5887285/food-and-beverage-warehousing-market-product

- Reports and Data: Refrigerated Warehousing Storage Market Forecast to 2034 — https://www.reportsanddata.com/report-detail/refrigerated-warehousing-storage-market

- Global Growth Insights: Refrigerated Warehouse Market Size, Trends & CAGR 2035 — https://www.globalgrowthinsights.com/market-reports/refrigerated-warehouse-market-107309

- LogisticsIQ: Warehouse Automation Market — Food & Beverage, Global Forecast to 2030 — https://www.thelogisticsiq.com/research/warehouse-automation-market

- SelectHub: Warehouse Automation Trends In 2026 — https://www.selecthub.com/warehouse-management/warehouse-automation-trends/

- Automate X: 7 Game-Changing Warehouse Automation Technologies for 2026 — https://automate-x.com.au/knowledge-hub/warehouse-automation-technologies

- DELIECN: Warehouse Automation Trends 2026 — ASRS, Shuttle Systems and Robotics — https://www.delilogitech.com/news/warehouse-automation-trends-2026-manufacturing/

- Scalar Spaces: The Rise of the Smart Warehouse in 2026 — https://scalarspaces.com/smart-warehouse-ai-iot-automation-2026/

- Automate.org: Top 16 Warehouse Automation Trends — Cobots, AMRs, AI — https://www.automate.org/robotics/editorials/16-warehouse-automation-trends

- Datup: Food & Beverage Supply Chain Key Trends for 2026 — https://datup.ai/en/supply-chain-trends/food-beverage

- AEW Capital: The Role of Cold Storage in the Supply Chain 2024 — https://www.aew.com/research/logistics-today

- AMZ Prep: Top 12 Cold Storage Companies in the USA 2026 — https://amzprep.com/best-cold-storage-companies/

- Addverb: Automation in Food and Beverage Industry — https://addverb.com/blog/automation-in-food-and-beverage-industry/

- Nova Pallet Tracking: Future Trends in ASRS Warehousing & Automation — https://www.novapalletracking.com/blog/future-trends-in-asrs-warehousing-and-automation

- Micromarket Insights: Food Grade Liquid Bulk Transportation and Storage Market 2026–2033 — https://www.micromarketinsights.com/product/food-grade-liquid-bulk-transportation-market/

- Food Navigator: Top 5 Food and Beverage Retail Trends for 2026 — https://www.foodnavigator.com/Article/2025/11/20/top-5-food-and-beverage-retail-trends-for-2026/