Date: June 9, 2026

In 2026, the global seafood industry is navigating a fundamental structural transition. Moving beyond the “experience economy” of previous years, the sector has entered the “Transformation Economy.” Today’s consumers are not just looking for a meal; they are seeking tangible outcomes—longevity, cognitive health, and metabolic balance. With a market value projected at USD 278.08 billion in 2026 and a clear trajectory toward a more integrated, digital-first supply chain, seafood is repositioning itself from a commodity to a benchmark for high-performance nutrition.

Executive Summary: The 2026 Global Seafood Industry Landscape

The industry is currently defined by a “resilience-and-innovation” strategy. Producers are balancing supply-side constraints—such as environmental pressures and rising energy costs—with a surging global demand for protein-rich, health-optimized diets. The rise of GLP-1 medications and a heightened focus on metabolic health have created a “protein-first” tailwind, while digitalization and e-commerce are bridging the gap between coastal production and inland consumption.

Key Takeaways for Stakeholders:

- Seafood as “Transformation Nutrition”: Seafood is the primary beneficiary of the shift toward longevity-focused diets. Its naturally high levels of Omega-3s, vitamin B12, and lean protein make it the gold standard for health-conscious consumers.

- The Asian Catalyst: Asia-Pacific remains the engine of global demand. Urbanization, the rise of the middle class, and an e-commerce-dominated retail environment are turning seafood into a daily staple in markets like China, South Korea, and India.

- Traceability is the New Currency: With consumers demanding transparency, companies using AI-driven traceability, blockchain, and robust eco-labeling (MSC/ASC) are winning market share and securing premium pricing.

- The “Frozen” Pivot: Rising operating costs have cemented frozen, pre-packed, and value-added seafood as a permanent consumer favorite, offering affordability, convenience, and reduced food waste.

Table of Contents

1. Market Overview: A Sector in Transition

The global seafood industry has transitioned from post-pandemic recovery into a period of strategic adaptation.

Valuation & Growth

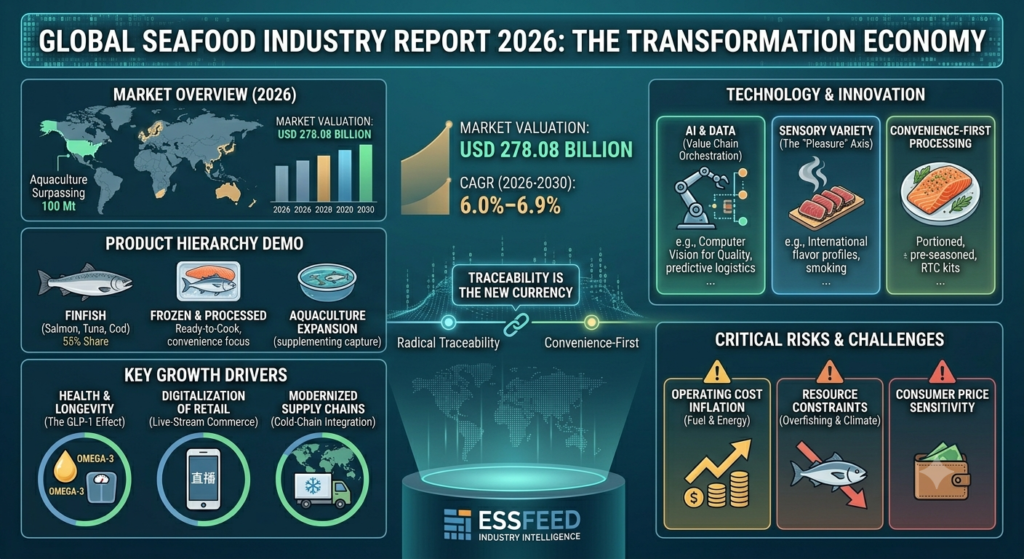

The global seafood market is valued at approximately USD 278.08 billion in 2026, with a projected CAGR of 6.0% to 6.9% through 2030. This growth is sustained by a balance between rising global consumption and the necessary modernization of supply chain infrastructure.

The Product Hierarchy

- Fish (55% share): Continues to dominate the market. Species like salmon, tuna, cod, and tilapia remain the primary drivers of retail and foodservice volume.

- Frozen & Processed (Growth Segment): Consumers increasingly favor frozen, ready-to-cook, and value-added (marinated/breaded) products due to their convenience and lower price points compared to fresh alternatives.

- Aquaculture Expansion: Aquaculture production is anticipated to surpass the 100 Mt mark globally, playing a critical role in supplementing capture fisheries and stabilizing global supply.

The global seafood industry has definitively moved past the era of post-pandemic volatility, settling into a phase of strategic adaptation. This transition is characterized by a shift in value creation: the industry is no longer solely focused on increasing raw catch volumes, but on maximizing the value and nutritional efficacy of every harvested tonne.

Valuation & Growth: The Stability of High-Demand Protein

The global seafood market is valued at approximately USD 278.08 billion in 2026. Industry projections anticipate a consistent CAGR of 6.0% to 6.9% through 2030, a robust performance driven by three structural pillars:

- The “Protein-First” Diet: As aging global populations and the widespread use of metabolic health medications (like GLP-1s) prioritize high-quality, lean, and bioavailable protein, seafood has become a primary beneficiary, often displacing higher-fat red meats in daily consumption.

- Cold-Chain Modernization: Massive investments in cold-chain infrastructure across emerging economies—specifically in India, Indonesia, and China—are successfully unlocking inland markets, converting regions that were previously dependent on dried/preserved products into consumers of fresh and frozen seafood.

- Manufacturing Efficiency: The “industrialization” of seafood processing is mitigating the historic risks of supply-side commodity volatility, allowing large-scale processors to maintain margins even when fuel and energy costs fluctuate.

The Product Hierarchy: A Maturing Ecosystem

The industry’s product portfolio is segmenting into three clear categories, each serving a distinct consumer need and profitability profile:

- Fish (55% Share): The Foundation of Consumption While “fish” remains the bedrock of the sector, its dominance is fueled by a move toward versatility. Species such as salmon, tuna, cod, and tilapia are being rebranded as functional “base ingredients” for rapid, daily meals, rather than just “center-of-the-plate” weekend indulgences.

- Frozen & Processed: The “Convenience-Quality” Hybrid This segment is the industry’s most critical growth lever. Modern consumers, facing time-scarcity and inflation, are increasingly turning to value-added formats—breaded fillets, marinated skewers, and ready-to-cook meal kits. Advanced blast-freezing technologies have finally bridged the “quality gap,” with many consumers now perceiving frozen-at-sea products as equivalent, or even superior, to “fresh-thawed” counter fish.

- Aquaculture Expansion: The Supply Stabilizer Aquaculture has officially redefined the supply landscape, with global production consistently surpassing the 100 million tonne mark. It is no longer just a “supplement” to wild capture; it is the industry’s primary hedge against climate-related volatility. By stabilizing output, aquaculture enables the long-term supply agreements required by large retail chains and global foodservice operators, effectively anchoring the industry’s ability to plan for future growth.

2. Key Growth Drivers

- Health & Longevity Trends: The “protein-first” movement—fueled by aging populations and the use of GLP-1 medications—is driving demand for high-quality, lean proteins. Seafood is uniquely positioned to meet this demand.

- Digitalization of Retail: In Asia, the boundary between social media and food retail has collapsed. Live-stream commerce and home delivery of fresh, premium seafood are now the primary indicators of quality and trust.

- Modernized Supply Chains: Improved cold-chain logistics are unlocking inland markets in India, China, and Southeast Asia, converting populations previously reliant on dried/salted fish into consumers of fresh and frozen seafood.

The seafood industry’s growth in 2026 is fueled by a synergy between evolving biological needs, technological empowerment, and a restructuring of global retail. The sector is effectively capitalizing on the shift toward “Transformation Nutrition,” where consumers view their diet as an active investment in their physical and cognitive future.

Health & Longevity Trends: The “Protein-First” Movement

Seafood is uniquely positioned to benefit from the current focus on metabolic health and longevity, a trend significantly accelerated by the widespread adoption of GLP-1 receptor agonists (e.g., Ozempic, Wegovy).

- The GLP-1 Effect: These medications have fundamentally altered dietary behavior. Users are consuming fewer total calories, but are significantly more focused on the nutrient density of those calories. With the reduction in appetite, every meal must count, creating an inelastic demand for high-quality, lean, and bioavailable protein. Seafood, naturally rich in Omega-3 fatty acids, vitamin B12, and selenium, provides a nutritional profile that is difficult to replicate with synthetic supplements, positioning it as the ultimate “functional” food.

- Transformation Nutrition: The industry has moved beyond marketing “fish” as a mere alternative to meat. It is now positioned as a cornerstone of the “Transformation Economy”—a framework where consumers prioritize foods that promote tangible outcomes like sleep quality, cognitive clarity, and sustained energy levels. Seafood is the benchmark for this lifestyle, viewed by health-conscious demographics as the “gold standard” for sustainable longevity.

Digitalization of Retail: The Blurring of Social and Commerce

In the Asia-Pacific region, the seafood market is leading a global trend where the distinction between social media platforms and food retail has effectively collapsed.

- Live-Stream Commerce: Purchasing journeys frequently begin on platforms like TikTok or local equivalents, where live-commerce sessions offer transparency, entertainment, and immediate social proof. For a younger, digitally native demographic, watching a high-quality product being prepared or hearing a brand story in real-time is the primary trust-building exercise.

- The “Home-Delivery” Marker of Quality: E-commerce has transformed from a convenience tool into a status symbol. Fresh seafood delivered directly to the consumer’s doorstep is now perceived as a primary indicator of cold-chain integrity, safety, and superior quality. In markets like China and South Korea, where the number of single-person households is rising, small-portion, ready-to-eat formats (such as pre-filleted sashimi-grade packs) are seeing massive velocity increases through digital retail channels.

Modernized Supply Chains: Unlocking Inland Markets

The industry is successfully converting populations that were historically reliant on dried, salted, or preserved fish into daily consumers of fresh and frozen seafood.

- Cold-Chain Democratization: Significant capital expenditure in logistics—including refrigerated rail, port modernization, and standardized containerization—has bridged the “distance gap.” Sophisticated cold-chain operators now provide end-to-end traceability, ensuring that temperature-sensitive products remain within strict safety parameters from the point of harvest to inland distribution centers.

- Predictive Logistics: By leveraging AI-driven demand forecasting, logistics providers can manage capacity more effectively, reducing dwell times and spoilage risks at ports. This modernization has made fresh and frozen seafood more affordable and accessible in the secondary and tertiary cities of India, Indonesia, and China, where the burgeoning middle class is rapidly adopting modern seafood-rich diets as a primary protein source.

3. Critical Risks and Challenges

- Operating Cost Inflation: Fuel, energy, and refrigeration costs remain high. The industry is under significant pressure to pursue an energy transition across fleets, farms, and cold storage to remain competitive.

- Environmental & Resource Constraints: Overfishing, habitat degradation, and climate change (e.g., El Niño events) continue to limit the expansion of wild-capture fisheries, placing greater importance on sustainable aquaculture management.

- Consumer Price Sensitivity: Despite the demand for quality, inflation has made the average consumer more cautious. The industry must balance premium positioning with affordable, value-added formats to maintain volume.

While the seafood industry is benefiting from long-term health and demand tailwinds, 2026 presents a complex risk landscape. Stakeholders are operating in an environment where resource volatility and operational overhead are colliding with shifting consumer purchasing power.

Operating Cost Inflation: The Energy Transition Mandate

The seafood industry is uniquely energy-intensive, with costs spanning from high-seas fuel consumption to the 24/7 power requirements of global cold-chain infrastructure.

- The “Fleet-to-Fridge” Pressure: As carbon pricing and environmental regulations tighten, the industry is under intense pressure to decarbonize. For wild-capture fleets, this means exploring alternative fuels and hybrid propulsion systems; for aquaculture and processing facilities, it requires a massive shift toward renewable energy integration and high-efficiency refrigeration systems.

- Margin Compression: Because many seafood products are commodities, individual firms have limited ability to pass rising energy and logistics costs directly to the consumer. This is forcing a massive industry-wide consolidation, where only those with the scale to invest in operational efficiency can maintain sustainable margins.

Environmental & Resource Constraints: The Climate Hedge

The industry is currently facing a “production plateau” in wild-capture fisheries, necessitating a fundamental pivot in how global seafood volume is secured.

- Ecosystem Instability: Climate events—most notably the intensification of El Niño and La Niña cycles—are drastically shifting migratory patterns, causing fish stocks to relocate and disrupting established harvest zones. Habitat degradation and ocean acidification further threaten the long-term viability of key capture grounds.

- The Aquaculture Imperative: Because capture fisheries cannot sustainably expand to meet growing global protein demand, aquaculture management has moved from a “growth option” to a “survival imperative.” In 2026, the focus has shifted toward Circular Aquaculture Models, which prioritize closed-containment systems, disease resistance, and sustainable, non-fish-meal-based feeds to decouple production from the limitations of the natural ocean environment.

Consumer Price Sensitivity: The “Value-Gap” Challenge

The post-inflationary environment of 2026 has left the global consumer more cautious, forcing a re-evaluation of how seafood is marketed and sold.

- The Bifurcation of Demand: We are witnessing a clear split in the market: a small, affluent segment remains willing to pay premiums for “ultra-fresh” or “sustainably-certified” artisanal seafood, while the mass market is increasingly sensitive to the price-per-kilogram.

- Value-Added Retention: To maintain volume during periods of fiscal tightening, producers are aggressively pivoting toward “value-added” formats (e.g., portioned, seasoned, or pre-cooked seafood). These products satisfy the desire for premium protein while offering the predictability of a fixed price point per meal. The challenge for 2026 is maintaining the “health halo” of seafood while using processing techniques that keep products accessible to budget-conscious households.

Risk Impact Matrix

| Risk Factor | Core Consumer/Industry Concern | 2026 Strategic Response |

| Operating Costs | Rising fleet/refrigeration overhead | Energy transition & operational automation |

| Resource Limits | Ecosystem collapse & stock volatility | Shift to circular, sustainable aquaculture |

| Price Sensitivity | Reduced purchasing power | Value-added formats & portion control |

4. Technology and Innovation: Digitizing the Blue Economy

Global Seafood Industry Innovation in 2026 is focused on Traceability, Efficiency, and Sensory Appeal.

- AI and Data Along the Value Chain: Digital tools are being used to manage resources, forecast demand, and ensure product origin. This transparency is crucial for building trust in an environment where consumers scrutinize the “how” behind their food.

- Sensory Variety: The “Pleasure” axis is growing. Manufacturers are utilizing intense marinades, subtle smoking techniques, and international flavor profiles (e.g., Asian-inspired tataki or soy-marinated tuna) to attract new segments.

- Convenience-First Processing: Sophisticated cutting and cooking techniques are making it easier for consumers to enjoy seafood in everyday meals, removing the “skill barrier” to preparation.

In 2026, the seafood industry is undergoing a digital and culinary transformation. Technology is no longer just about harvesting efficiency; it is about creating a “connected” value chain that delivers transparency, culinary pleasure, and daily convenience to a global consumer base that demands more from their protein.

AI and Data: The Orchestration of the Value Chain

Artificial Intelligence has moved from a speculative tool to a central operating system for the global seafood supply chain.

- Predictive Transparency: Companies are leveraging AI to ingest decades of production, harvesting, and quality control data. By using generative business intelligence, decision-makers can now “talk to their data”—prompting systems to identify supply chain gaps, flag illegal fishing risks, or optimize harvest timing to ensure peak freshness.

- Computer Vision for Quality: Smart cameras and computer vision are replacing manual, error-prone quality control. Automated inspection systems now scan every fillet, can, or crustacean for defects, color consistency, and size, creating a granular, verifiable digital record of quality that protects brands against claims and enhances consumer trust.

- Operational Resilience: AI-powered systems are managing aquaculture environments by monitoring water quality (pH, oxygen, ammonia) in real-time and adjusting feeding schedules automatically. This precision not only improves fish welfare and reduces feed waste but also provides the data-driven proof of sustainability that retailers and eco-conscious shoppers now require.

Sensory Variety: The “Pleasure” Axis

Innovation in seafood is increasingly dictated by the “Pleasure” axis, with taste and culinary excitement acting as the primary drivers of new product development.

- International Infusion: Product developers are moving beyond simple seasoning, adopting complex culinary techniques from international traditions—such as flame-searing Japanese tataki, infusion of global spices in sophisticated marinades, and specialized smoking techniques (e.g., truffle-infused or wood-smoked aromatics). These products are designed to make seafood “festive” or “gastronomic,” elevating it from a weekly staple to a premium culinary experience.

- Refinement of Ingredients: Innovation is now focused on “noble ingredients” and unique pairings. Using distinctive, premium additives (like specialty salts, herb butters, or artisanal oils) enhances the perceived value, allowing producers to capture higher margins in a market that is increasingly seeking refinement over commodity offerings.

Convenience-First Processing: Removing the “Skill Barrier”

The industry is aggressively targeting the time-starved consumer by removing the friction involved in cooking seafood.

- Ready-to-Enjoy Formats: The “skill barrier”—the fear of overcooking or not knowing how to prepare fish—is being dismantled. Through the proliferation of pre-seasoned, portion-controlled, and ready-to-cook (RTC) formats, seafood is becoming a viable option for quick, mid-week meals.

- Culinary-Driven Manufacturing: Processing equipment is now integrated with advanced robotics to achieve precise cutting, filleting, and de-boning that was previously only possible by hand. This culinary-focused automation ensures that home cooks receive a product that is already prepared to professional standards, encouraging frequent consumption by removing the prep work that historically hindered seafood’s daily appeal.

5. Strategic Outlook for Stakeholders

Success in 2026 requires shifting from “volume-only” strategies to “value-and-trust” strategies.

Actionable Recommendations:

- Invest in Transparency: If you cannot verify the source of your seafood, you are losing the trust of the modern consumer. Invest in blockchain-based or digital traceability now.

- Lean Into Convenience: Develop products that solve the “time barrier.” Ready-to-cook, portion-controlled, and flavor-enhanced seafood are the keys to capturing daily household meal occasions.

- Target High-Growth Markets: Prioritize distribution and digital engagement in Asia-Pacific markets, where the middle-class appetite for fresh, delivered seafood is expanding most rapidly.

In 2026, the seafood industry has moved beyond the commodity trap. The “volume-only” race to the bottom, which prioritized bulk landings at the lowest cost, has been superseded by a Value-and-Trust paradigm. Profitability is no longer just a function of supply chain scale; it is increasingly a function of brand equity and the ability to prove product integrity to an hyper-informed consumer.

Actionable Recommendations for 2026

1. Invest in Radical Transparency (The Trust Moat)

In an era where “greenwashing” is easily detected by data-literate consumers and strict regulatory bodies, transparency is your most defensible asset.

- The Strategy: Move beyond simple “origin labeling” to granular traceability. Consumers now want to know the who, where, and how behind their meal.

- Implementation: Deploy blockchain or cloud-based ledger systems that allow a consumer to scan a QR code on packaging and see the vessel name, harvest date, and GPS coordinates of the catch or farm. This “digital provenance” eliminates information asymmetry and allows brands to command a consistent price premium, as trust becomes a tangible product differentiator.

2. Lean Into “Frictionless” Convenience (The Time Moat)

The biggest competitor for seafood is not other protein types—it is the consumer’s lack of time and culinary confidence.

- The Strategy: Solve the “time barrier.” Modern households prioritize ease of preparation over culinary exploration.

- Implementation: Pivot R&D toward “Heat-and-Eat” or “Prep-Free” solutions. This includes sous-vide fillets that are ready in minutes, flavor-infused portions that require no additional seasoning, and “oven-ready” seafood kits. By removing the preparation hurdle, you shift seafood from a “special occasion” meal to a “daily protein” habit, effectively increasing the frequency of purchase and household penetration.

3. Target High-Growth Velocity Markets (The Geography Moat)

The center of gravity for seafood demand has firmly shifted to the Asia-Pacific region, driven by rapid urbanization and the ubiquity of digital retail.

- The Strategy: Align your supply chain and marketing with the digital retail ecosystems of APAC.

- Implementation: In markets like China, Vietnam, and Indonesia, the “path to purchase” is digital. Establish partnerships with local e-commerce giants and leverage social-commerce platforms (live-streaming) to reach urban middle-class consumers directly. Success here requires a “local-first” approach, focusing on culturally relevant flavor profiles (e.g., specific regional spices, ready-to-sashimi formats) and a logistics network optimized for last-mile fresh delivery.

Strategic Summary: The 2026 Seafood Business Model

| Strategic Pillar | Legacy Strategy (Pre-2024) | 2026 Competitive Reality |

| Primary Goal | Maximize total catch volume | Maximize value-added margin |

| Traceability | Compliance-based; static labels | Consumer-facing; digital/blockchain |

| Product Format | Whole fish/commodity blocks | Convenience-first (portion/pre-seasoned) |

| Market Focus | Established Western retail | Digital-first APAC retail/foodservice |

6. Leading Industry Influencers

| Company/Entity | Focus |

| Mowi | Global leader in Atlantic salmon; innovation in sustainable farming. |

| Thai Union | Massive scale in global canned and ambient seafood; value-added focus. |

| Lerøy Seafood | Expert in cold-water harvesting and logistics. |

| Nutreco (Skretting) | Critical for sustainable aquafeed technology. |

| Bumble Bee Foods | Dominant in shelf-stable, accessible protein formats. |

In 2026, the global seafood industry competitive landscape is defined by “Vertical Mastery”—the ability of these firms to control not just the harvest, but the entire value chain from sustainable feed formulation to the digital interface at the point of consumer purchase. The most influential players are those who have successfully transitioned from being pure-play commodity suppliers to essential partners in global food security and functional nutrition.

| Company/Entity | Core Focus | 2026 Strategic Advantage |

| Mowi | Atlantic Salmon | The global benchmark for industrial-scale sustainability. Mowi’s heavy investment in post-smolt technology and AI-driven biological monitoring allows them to stabilize output despite climate volatility, making them the most reliable partner for premium retail. |

| Thai Union | Global Canned & Ambient | Masters of the “value-added” pivot. Thai Union has successfully diversified into alternative proteins and functional health ingredients (e.g., marine collagen), positioning their massive ambient footprint as the “backbone” of accessible nutrition. |

| Lerøy Seafood | Cold-Water Harvest | Experts in “integrated logistics.” Their dominance in cold-water harvesting is bolstered by a proprietary distribution network that guarantees “fjord-to-fork” freshness, effectively setting the standard for speed-to-market in European and Asian markets. |

| Nutreco (Skretting) | Sustainable Aquafeed | The “engine room” of the industry. As the world shifts from wild-capture to aquaculture, Skretting’s breakthroughs in insect-based and algal-based feed have solved the industry’s greatest bottleneck: decoupling production from finite fishmeal resources. |

| Bumble Bee Foods | Shelf-Stable Protein | The leader in “democratized seafood.” By optimizing supply chain efficiency and focusing on flavor-enhanced, easy-open formats, they have turned shelf-stable seafood into a high-velocity, inflation-resistant essential for mass-market consumers. |

The Competitive Shift: From Catch to Capability

The “moat” around these industry leaders has fundamentally changed. The winning strategy in the Global Seafood Industry 2026 is no longer about who owns the most boats; it is about who owns the most efficient, transparent, and consumer-aligned platform.

- Platform Versatility: These leaders are no longer selling “fish.” They are selling data-backed traceability. Retailers now favor these companies because they provide the digital documentation (API-ready audit trails) required to meet global ESG (Environmental, Social, and Governance) compliance standards.

- Nutritional Integration: By aligning with the “Transformation Economy,” these companies have shifted their R&D away from simple product preservation and toward bioavailability. They are partnering with clinical research groups to market their products not just as seafood, but as targeted, high-performance dietary solutions—tapping into the consumer shift toward metabolic health.

- Climate Resilience: The true “competitive moat” in 2026 is the ability to maintain supply despite environmental disruption. Companies that have invested heavily in land-based RAS (Recirculating Aquaculture Systems) and offshore closed-containment technologies are the ones securing long-term, high-value contracts with major global retailers.

7. Conclusion: The Path Forward

The global seafood industry in 2026 is a dynamic sector defined by adaptation. By leveraging the “Transformation Economy”—positioning seafood as an essential tool for health and longevity—the industry has an opportunity to secure a central role in the global diet. Companies that successfully bridge the gap between sustainability, digital trust, and culinary convenience will thrive in this new era.

8. FAQ

What is the projected market value of the global seafood industry in 2026?

The global seafood market is valued at approximately USD 278.08 billion in 2026. The industry is currently experiencing a steady growth trajectory, with a projected Compound Annual Growth Rate (CAGR) of 6.0% to 6.9% through 2030.

How has the “GLP-1 effect” impacted the seafood industry?

The widespread adoption of GLP-1 receptor agonists (metabolic health medications) has fundamentally shifted dietary behavior toward “Transformation Nutrition.” Because these drugs reduce total caloric intake, consumers are prioritizing high-quality, lean, and bioavailable protein. Seafood is uniquely positioned as a “functional food” rich in Omega-3s and B12, leading to inelastic demand for these products among health-conscious demographics.

Why is the “Frozen & Processed” segment considered the industry’s most critical growth lever?

Due to persistent inflationary pressures and time-scarcity, modern consumers increasingly prioritize the “Convenience-Quality” hybrid. Advanced blast-freezing technologies have eliminated the historic quality gap between fresh and frozen fish. Consequently, value-added formats—such as pre-marinated fillets, breaded portions, and ready-to-cook meal kits—are now the primary drivers of retail volume and frequency of purchase.

What is meant by the “Transformation Economy” in the context of seafood?

The “Transformation Economy” refers to the shift in consumer mindset where food is no longer purchased solely for sustenance or flavor, but as an active investment in tangible personal outcomes, such as sleep quality, cognitive clarity, and sustained metabolic energy. Seafood is being repositioned as the “gold standard” for this lifestyle.

How are supply chains being modernized to reach inland markets?

The industry is undergoing a “Cold-Chain Democratization.” Massive capital expenditure in refrigerated rail, port modernization, and standardized containerization is bridging the distance gap. This has allowed fresh and frozen seafood to reach secondary and tertiary cities in high-growth markets like India, China, and Indonesia, effectively converting populations that were previously reliant on dried/preserved fish into consumers of fresh protein.

What are the primary risks to industry profitability in 2026?

The three primary risks are:

Operating Cost Inflation: Persistent high costs in fuel, energy, and global refrigeration.

Environmental Constraints: Climate-driven shifts in fish migration patterns and the plateau of wild-capture fisheries.

Consumer Price Sensitivity: The challenge of maintaining premium health branding while providing affordable price points to a budget-conscious mass market.

Why is aquaculture management now a “survival imperative”?

Because wild-capture fisheries are limited by environmental thresholds and climate volatility, they cannot sustainably scale to meet global protein demand. Aquaculture has moved from a “supplemental growth option” to the industry’s primary hedge against supply-side instability, enabling long-term, predictable supply agreements with global retailers.

What is the “Digital Traceability” mandate?

In 2026, transparency is a competitive moat. Retailers and consumers demand “digital provenance”—the ability to verify the vessel name, harvest date, and GPS coordinates of a product via blockchain or QR codes. Companies that cannot provide this verifiable data are increasingly excluded from premium retail shelves.

Which markets are currently seeing the fastest “growth velocity”?

The Asia-Pacific region is the clear leader. Rapid urbanization, a burgeoning middle class, and the collapse of the boundary between social media and food retail (via live-stream commerce and home delivery) are turning seafood into a high-velocity, daily staple in markets like China, South Korea, India, and Vietnam.

What is the strategic shift in the 2026 Seafood Business Model?

The industry has pivoted from a “Volume-Only” strategy (maximizing total catch tonnage) to a “Value-and-Trust” paradigm. Profitability is no longer determined solely by supply chain scale, but by the ability to provide brand equity, proven product integrity, and convenience-focused formats that remove the “skill barrier” for home preparation.

9. Sources and References

- Research and Markets: Global Seafood Market Report 2026 Direct Link: Seafood Market Report 2026 – Research and Markets

- Future Market Insights (FMI): Seafood Market | Global Market Analysis Report 2026–2036 Direct Link: FMI Oyster and Clam Market Outlook 2026-2036

- Note: FMI produces granular reports by species/region. The link above provides the detailed methodology and outlook for the 2026–2036 period.

- Pesceinrete (Industry Insights): Global Seafood Industry Trends 2026 Direct Link: Global Seafood Trends & Market Insights 2026 (via FHA-Food & Beverage)

- SeafoodSource: Seafood sales for 2026 and beyond expected to benefit from health, protein trends Direct Link: SeafoodSource: Seafood Sales Trends 2026

- FAO: Fish and Seafood Outlook 2026 Direct Link: FAO Globefish: Aquatic Products and the Global Economy (2026 Update)