Date: June 9, 2026

In 2026, the global plant-based protein industry has definitively exited its “hyper-growth” speculative phase, entering a critical period of operational maturity and consumer rationalization. While early market narratives were dominated by meat-mimicry “hype,” the 2026 landscape is defined by a shift toward clean-label integrity, nutritional density, and price-competitiveness. The market is valued at approximately USD 22.5 billion in 2026, with a clear trajectory toward a more integrated role in the mainstream global food system by 2030.

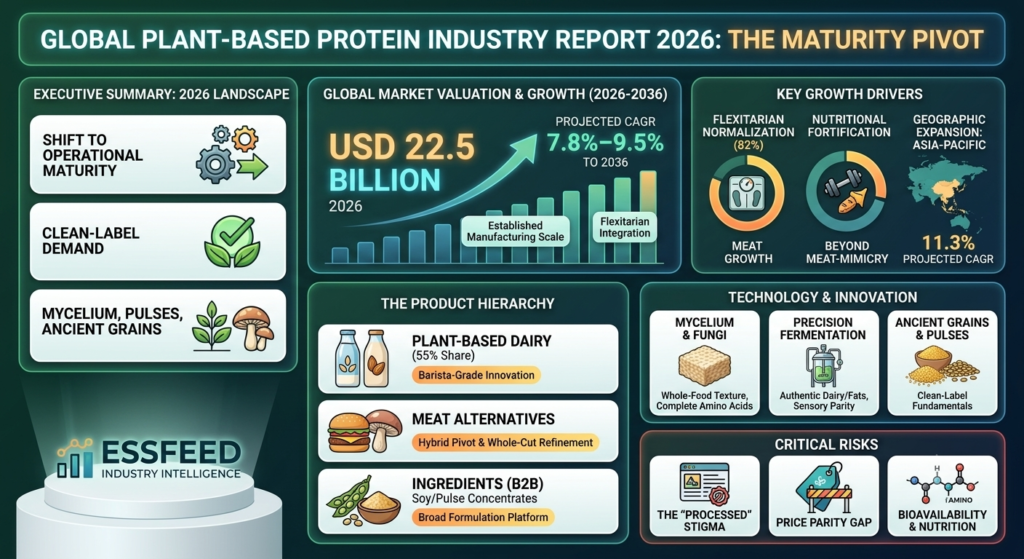

Executive Summary: The 2026 Plant-Based Industry Landscape

The plant-based sector is currently undergoing a “correction-and-consolidation” strategy. Consumers are demanding transparency, leading manufacturers to pivot away from ultra-processed, long-ingredient-list formulations toward whole-food-based proteins (mycelium, pulses, ancient grains). While plant-based dairy remains the dominant volume driver, the meat-alternative segment is pivoting to hybrid models and functional nutrition to overcome taste and price barriers.

Key Takeaways for Stakeholders:

- The “Clean Label” Mandate: The primary friction point for mass-market adoption is no longer just taste; it is the perception of “ultra-processing.” Winners in 2026 are those prioritizing short, recognizable ingredient lists.

- Fungi & Fermentation Take Center Stage: Mycelium and fermentation-enabled proteins are solving the texture and nutrition gap that early-generation pea/soy isolates struggled with.

- Dairy Dominance: Plant-based dairy (oat, almond, soy) continues to outperform meat alternatives in retail velocity, driven by established consumer habits and barista-grade functional formulations.

- Mainstream Integration: Plant-based proteins are moving from the “vegan aisle” into broad-scale B2B food formulation, increasingly utilized for protein fortification in regular food formats (snacks, bakery, recovery drinks).

Table of Contents

1. Market Overview: The 2026 Landscape

The market is shifting from “niche alternative” to “broad food formulation platform.”

Valuation & Growth

The global plant-based proteins market is valued at USD 22.5 billion in 2026, with projections showing a consistent CAGR of 7.8% to 9.5% through 2036. Growth is driven by established manufacturing scale and wider consumer acceptance of flexitarian dietary patterns.

The Product Hierarchy

- Plant-Based Dairy (55% share): Continues to hold the largest market share. The dominance of oat milk—thanks to barista-friendly formulations—has cemented dairy alternatives as a daily staple rather than a luxury choice.

- Meat Alternatives (Meat-style formats): While growth has cooled, the category is seeing a resurgence through “hybrid” products (blending plants with fungi or high-quality legume proteins) to improve texture and lower costs.

- Ingredients (B2B): Protein concentrates and isolates remain the backbone of the industry, with soy leading due to its familiarity, cost-efficiency, and established supply chains.

The plant-based protein market has transitioned from a period of high-growth, speculative novelty into a stage of operational maturity. The industry’s overarching strategy has shifted: manufacturers are no longer exclusively chasing “meat-mimicry” in the center of the plate. Instead, they are integrating plant proteins as versatile, functional components across the entire food landscape.

Valuation & Growth

The global plant-based protein market is valued at approximately USD 22.5 billion in 2026. Projections indicate a consistent CAGR of 7.8% to 9.5% over the next decade. This growth is sustained not by short-term dietary trends, but by long-term structural changes in global manufacturing and consumer behavior:

- Manufacturing Scale: Large-scale food conglomerates have integrated plant protein processing into their existing supply chains, significantly reducing the “innovation premium” that previously inflated product costs.

- Flexitarian Integration: The market is now driven by “flexitarian” consumers—the vast majority of the market—who do not adhere to strict veganism but actively seek to incorporate plant-derived ingredients into their daily diet for health, sustainability, or variety.

The Product Hierarchy: A Maturing Ecosystem

The industry is structured into three distinct layers, each serving a different commercial objective:

- Plant-Based Dairy (55% share): The Foundation

- This segment has reached maturity. Plant-based milk (oat, almond, soy) has transitioned from a specialty item to a household commodity.

- Barista-Grade Innovation: The success of oat milk is largely due to advanced formulation—specifically designing products that replicate the functional properties of cow’s milk (frothing, stability in coffee, texture). This focus on “functional performance” over simple “substitute status” has cemented dairy alternatives as a daily staple.

- Meat Alternatives (Meat-style formats): The Refinement Phase

- Growth in this category has cooled as consumer skepticism toward “ultra-processed” foods has risen. The industry is currently in a “refinement era,” moving away from complex stabilizers and artificial binders.

- The Hybrid Pivot: To bridge the gap between “artificial” and “animal-like,” leading firms are adopting hybrid models. By blending plant proteins with mycelium (fungi) or high-quality legume proteins, they are improving texture, nutritional profiles, and umami flavor without the need for extensive chemical processing.

- Ingredients (B2B): The Backbone

- B2B supply represents roughly 26% of the market share, serving as the hidden engine of the industry.

- Soy’s Dominance: Despite the rise of newer sources like pea or chickpea, soy protein remains the dominant isolate (holding approximately 30% of the product segment). Its established supply chain, formulation familiarity among food scientists, and excellent solubility make it the “gold standard” for large-volume, cost-efficient product development.

- Technical Versatility: As manufacturers shift toward “broad food formulation platforms,” they are purchasing concentrates and isolates to fortify everything from protein-enhanced bakery and snack foods to recovery beverages, treating plant protein as a functional building block rather than just a meat substitute.

The Move to a Broad Formulation Platform

The most critical evolution in 2026 is that plant-based protein is no longer just for the “vegan aisle.” It is becoming a broad food formulation platform. Food scientists are utilizing these proteins to support health-positioning in mainstream products, such as adding fiber-rich pulse proteins to pasta or fortifying breakfast cereals with chickpea isolates. This shift allows the industry to distribute demand across a wider range of food categories, reducing reliance on the volatility of any single consumption trend.

2. Key Growth Drivers

- Flexitarian Normalization: 82% of industry experts highlight flexitarianism as the strongest growth engine. Most consumers are not seeking total dietary exclusion but are looking for “balance.”

- Nutritional Fortification: Manufacturers are leveraging plant proteins to boost the nutrient density of snacks, bakery, and recovery foods, moving beyond the “meat-alternative” trap into high-growth functional nutrition.

- Geographic Expansion: Asia-Pacific is the fastest-growing region (projected CAGR of 11.3%), fueled by rising lactose intolerance, urbanization, and expanding e-commerce channels.

In 2026, the plant-based protein sector is shifting its strategy from “category disruption” to “category integration.” By aligning with broader wellness trends and demographic shifts, manufacturers are successfully embedding plant proteins into the fabric of everyday consumption.

Flexitarian Normalization: The New “Balanced” Diet

The industry has largely moved past the era of marketing to a small, strictly vegan minority. In 2026, the growth engine is the flexitarian consumer—the roughly 82% of industry experts cite this as the dominant market force.

- The “Balance” Imperative: Today’s consumers are not looking to strictly exclude animal protein. Instead, they are seeking “nutritional variety.” This shift has lowered the barrier to entry for plant-based products, as they are now positioned as an “addition” to a meal rather than a radical “replacement.”

- Retail Velocity: Because flexitarians treat plant-based options as an occasional or alternating choice, brand loyalty is shifting toward products that offer familiar comfort (e.g., plant-based bolognese or breakfast sausages) rather than niche, high-concept alternatives.

Nutritional Fortification: Moving Beyond the “Meat-Alternative” Trap

The industry is intentionally evolving away from the “meat-alternative” branding, which often triggers skepticism regarding the high processing levels of such products.

- Functional Nutrition: By leveraging plant protein isolates as additives in “non-meat” categories—such as high-protein bakery items, nutrient-dense breakfast cereals, and post-workout recovery bars—manufacturers are finding a larger, more receptive audience.

- Value-Added Health: Positioning plant protein as a “clean label” fortifier is a powerful strategy. In 2026, a cookie or bread slice that is fortified with chickpea or lentil protein carries a “health halo” that allows it to compete directly with premium, conventional snacks. This “stealth health” approach turns every snack aisle into a point-of-sale opportunity for plant-based ingredients.

Geographic Expansion: The Asia-Pacific Surge

Asia-Pacific has solidified its position as the fastest-growing region globally, with a projected CAGR of 11.3% through 2030.

- Lactose Intolerance and Urbanization: A significant portion of the Asian population is lactose-intolerant, creating a massive, organic market demand for dairy alternatives. As urbanization accelerates, the convenience of shelf-stable oat and soy beverages has made them an essential component of the modern urban diet.

- E-Commerce and Cold Chain: The expansion of robust e-commerce platforms and the rapid modernization of cold-chain logistics in markets like China, India, and Indonesia have allowed high-quality, chilled plant-based products to reach consumers in secondary and tertiary cities, where they were previously inaccessible.

Growth Driver Impact Summary

| Driver | Primary Target Market | 2026 Market Impact |

| Flexitarianism | Gen Z and Millennials | High; creates volume stability |

| Nutritional Fortification | Health/Wellness consumers | Moderate; captures premium price points |

| APAC Expansion | Urban/Middle-class | High; drives top-line revenue growth |

3. Critical Risks and Challenges

- The “Processed” Stigma: Consumers are increasingly skeptical of ultra-processed meat alternatives. Products with long lists of artificial binders and emulsifiers are losing shelf space to “whole-food” alternatives.

- Price Parity Gap: In most markets, plant-based meat alternatives still cost 40–80% more than conventional animal proteins. Achieving scale-driven price parity remains the single biggest barrier to mass-market retail penetration.

- Bioavailability & Nutrition: The industry is facing increased scrutiny regarding the bioavailability and complete amino acid profiles of certain plant-based proteins compared to animal-derived sources.

While the plant-based protein sector has matured into a vital component of the global food architecture, it faces significant structural headwinds in 2026. The “hype cycle” has concluded, and the industry is now being measured against the same rigorous standards as the established animal-protein industry—specifically regarding health, affordability, and nutritional integrity.

The “Processed” Stigma: A Crisis of Perception

Consumer trust in meat alternatives has been compromised by the perception of “ultra-processing.” In 2026, the retail environment is unforgiving toward products with long, complex ingredient lists.

- The “Clean Label” Shift: Shoppers are increasingly wary of binders, emulsifiers, and artificial flavorings required to force plant proteins into meat-like structures. Products that rely on chemical stabilization are rapidly losing shelf space to “whole-food” alternatives like mycelium, legumes, and ancient grains.

- Consumer Confusion: Research indicates that many consumers struggle to categorize processing levels, often misidentifying various plant-based products. This confusion has led to a blanket suspicion of the category. Brands that fail to provide transparent, simple ingredient labeling are increasingly viewed as “artificial,” a perception that is becoming the single largest barrier to repeat purchase among health-conscious flexitarians.

The Price Parity Gap: The Barrier to Mass Adoption

Despite significant technological progress, the price premium for plant-based meat remains the most stubborn hurdle.

- Persistent Premiums: In most developed markets, plant-based meat alternatives continue to retail at 40–80% higher prices than conventional beef or poultry. While economies of scale have improved, the reliance on high-cost, proprietary protein isolates and the need for specialized, small-batch manufacturing have kept these products firmly in the “premium” category.

- Inelastic Demand for Animal Protein: For the average price-sensitive consumer, animal protein remains a highly price-inelastic staple. Without reaching “price parity”—where a plant-based burger costs the same or less than a beef burger—the sector will continue to struggle to capture the truly mass-market, budget-conscious household.

Bioavailability & Nutrition: The Scientific Scrutiny

In 2026, the industry is no longer shielded from nutritional critique. Scientists and regulators are placing greater emphasis on the “completeness” of plant-based protein.

- Amino Acid Profiles: While soy is a complete protein, many other plant isolates (such as pea or wheat) can have lower levels of essential amino acids like methionine or lysine. Consumers are becoming more educated about protein quality, often prioritizing animal-derived sources because they are “bioavailable”—meaning the body can absorb and utilize them more efficiently.

- Nutritional Credibility: To maintain market growth, manufacturers must move beyond simple “protein grams per serving” marketing. The focus is shifting toward PDCAAS (Protein Digestibility Corrected Amino Acid Score) and ensuring that plant-based proteins provide the same synergistic nutritional benefits as whole-food animal proteins. Failure to address these concerns effectively leaves the industry vulnerable to the “not-a-real-food” narrative.

Risk Impact Matrix

| Risk Factor | Core Consumer Concern | 2026 Industry Response |

| Processed Stigma | Artificial additives & chemicals | Pivot to whole-food, short ingredient lists |

| Price Parity | Cost of living / Affordability | Scale manufacturing & lower ingredient costs |

| Bioavailability | Nutritional adequacy & digestibility | Protein blending & amino acid fortification |

4. Technology and Innovation: Beyond the Isolate

Innovation in 2026 focuses on ingredient purity and structural functionality.

- Mycelium & Fungi: Mycelium is the “breakout star” of 2026. Because it grows as a whole-food structure (not a blended isolate), it naturally replicates meat textures while delivering fiber and complete amino acids without artificial processing.

- Precision Fermentation: This technology is being used to produce high-value components—like specific proteins, fats, and flavors—that provide the sensory experience of dairy or meat without requiring animal source material.

- Ancient Grains & Pulses: There is a renewed focus on staples like finger millet, lentils, and chickpeas, which offer high-protein profiles and “clean” labels that resonate with health-conscious shoppers.

In 2026, the era of relying solely on highly processed protein isolates—like soy and pea—is rapidly drawing to a close. The industry’s R&D focus has pivoted from “mimicry at any cost” to “structural integrity and ingredient purity.” Innovation is currently driven by a quest to match the nutritional and sensory complexity of whole animal foods using nature-identical or whole-food-based technologies.

Mycelium & Fungi: The Whole-Food Revolution

Mycelium has emerged as the definitive “breakout star” of 2026. Unlike conventional meat alternatives that rely on the mechanical extrusion of isolated protein powders (which necessitates extensive binding agents), mycelium offers a superior technological pathway.

- Natural Texture: Mycelium grows in a filamentous, branched structure that natively replicates the fibrous texture of muscle tissue. This means manufacturers can produce “whole-cut” analogues (steaks, fillets) with minimal processing.

- Nutritional Density: Because the base material is the protein structure, it inherently contains fibers, essential amino acids, and micronutrients. It bypasses the need for the “ultra-processed” ingredient labels that plague first-generation meat alternatives, allowing brands to market products with short, consumer-friendly ingredient lists.

Precision Fermentation: Engineering the “Authentic” Sensory Experience

While mycelium provides the structure, precision fermentation is solving the industry’s flavor, fat, and functional deficiencies.

- Beyond the Meat Substitute: In 2026, precision fermentation is being used to produce specific, nature-identical molecules—such as heme for color/flavor, dairy proteins (casein and whey) for meltability/stretching, and specialized fats for mouthfeel.

- Solving the Allergen/Stability Gap: Industry giants are utilizing these microbes to create high-performance ingredients that are lactose-free, cholesterol-free, and allergen-free, yet chemically indistinguishable from their animal-derived counterparts. This is transforming how plant-based dairy is formulated, enabling shelf-stable products that froth and melt with the same consistency as cow’s milk.

Ancient Grains & Pulses: The Return to “Clean” Fundamentals

There is a profound movement back to the basics. Staples like finger millet, lentils, fava beans, and chickpeas are no longer just commodities; they are being repositioned as the “premium base” for 2026 product development.

- The “Clean Label” Demand: Health-conscious shoppers are explicitly rejecting complex chemical formulations. Innovators are utilizing sophisticated milling, fractionation, and fermentation techniques on these ancient crops to maximize their protein bioavailability and functional properties (like solubility and gelling) without adding synthetic additives.

- Versatility and Sustainability: Beyond their clean-label appeal, these crops are prized for their adaptability to regenerative agricultural practices, which aligns with the broader ESG commitments now demanded by major retail and foodservice buyers.

Innovation Matrix: The 2026 Tech Stack

| Technology | Core Objective | Key Advantage |

| Mycelium | Whole-food structural texture | Natural mimicry; minimal processing |

| Precision Fermentation | Sensory parity (Fats, Flavor, Dairy) | Nature-identical taste/performance |

| Ancient Grains/Pulses | Ingredient transparency | Clean label; broad consumer appeal |

5. Strategic Outlook for Stakeholders

Success in 2026 requires balancing “technological idealism” with “consumer pragmatism.”

Actionable Recommendations:

- Pivot to Clean-Label: If your product has more than 10 ingredients, prioritize reformulation. Transparency is the new quality hallmark.

- Focus on Function: Do not just compete with meat. Compete with health. Position your protein as a source of fiber, gut-supporting prebiotics, and satiety (the “GLP-1 awareness” advantage).

- Diversify Formats: Move beyond the “burger.” Explore savory breakfasts, protein-rich snacks, and hybrid products that satisfy the palate without relying solely on expensive, highly processed isolates.

In 2026, the plant-based protein industry has reached a “pragmatism inflection point.” The speculative fervor of the early 2020s has been replaced by a rigorous focus on profitability, health-centric branding, and ingredient integrity. Success in the current landscape requires stakeholders to stop viewing their products as “meat replacements” and start viewing them as “value-added health solutions.”

Actionable Recommendations

- Pivot to “Clean-Label” Reformulation:

- The Strategy: The “short list” is the new competitive advantage. If your product label requires a chemistry degree to interpret, you are losing shelf space to “whole-food” brands.

- Implementation: Prioritize the removal of synthetic methylcellulose, artificial colors, and overly processed texturizers. Utilize natural ingredients like mycelium, fava bean flour, and vegetable fibers that provide structure while satisfying the growing consumer demand for “real food” transparency.

- Market Outcome: Brands that proactively shrink their ingredient lists see a direct increase in repeat-purchase rates, as they successfully shed the “ultra-processed” stigma.

- Focus on Functional Health (The “GLP-1 Awareness” Edge):

- The Strategy: Shift the marketing narrative from “it tastes like meat” to “it makes you healthier.”

- Implementation: Emphasize the nutritional synergy of your product. If your protein is fortified with gut-supporting prebiotics, high dietary fiber, or specialized antioxidants, lead with these benefits. In 2026, as consumers become increasingly aware of metabolic health and weight-management tools (like GLP-1 medications), positioning plant protein as a tool for satiety and stable blood sugar management is a high-growth pivot.

- Competitive Edge: Positioning your brand within the “functional nutrition” space allows you to command premium pricing that is not strictly tethered to the commodity price of animal meat.

- Diversify Beyond the “Burger”:

- The Strategy: The burger and nugget categories are saturated and price-sensitive.

- Implementation: Reallocate R&D toward high-utility, protein-dense formats that solve specific consumer problems. Think savory protein-rich breakfast bowls, fermented plant-based cheese spreads, or high-protein snack-able options (like crackers or jerky) that fit the “on-the-go” lifestyle.

- Hybridization: Utilize hybrid formulations—combining plant protein with smaller amounts of fungi or animal-derived ingredients if applicable—to optimize flavor and cost while moving away from a 100% reliance on expensive, volatile, and highly processed protein isolates.

Strategic Summary: The 2026 Plant-Based Business Model

| Strategic Focus | 2020–2024 Mindset | 2026 Competitive Reality |

| Primary Goal | Mimic animal meat exactly | Optimize for health and purity |

| Ingredient Strategy | Highly processed isolates | Whole-food bases (Mycelium, Pulses) |

| Marketing Angle | Sustainability & Ethics | Health, Nutrition, & Satiety |

| Retail Positioning | “Vegan/Alternative” aisle | “High-Protein/Functional” categories |

6. Leading Industry Companies

| Company/Entity | Focus |

| Archer-Daniels-Midland (ADM) | Massive scale, broad portfolio of soy, pea, and wheat solutions. |

| Roquette Freres | Leader in textured vegetable protein and pea-based innovation. |

| Cargill Inc. | Global logistics and supply chain stability for protein isolates. |

| Kerry Group | Taste and texture masking solutions for plant-based formulations. |

| Meati Foods | Leading the mycelium-based whole-food protein revolution. |

In 2026, the competitive landscape for plant-based proteins is dominated by entities that have successfully pivoted from commodity supply to integrated, value-added functional platforms. Influence is now measured by the ability to solve the industry’s two biggest hurdles: clean-label structural integrity and sensory parity.

| Company/Entity | Focus | Strategic Advantage |

| Archer-Daniels-Midland (ADM) | Massive scale & functional variety | Dominates the B2B space by continuously expanding its portfolio (including new soy/pea isolates like ProFam 883 and Arcon IH) to meet demand for high-solubility, clean-taste ingredients across global food categories. |

| Roquette Freres | Pea-based innovation | Maintains market leadership via highly automated, large-scale production (such as their massive Manitoba facility), setting the standard for quality-controlled, textured vegetable protein (TVP) ingredients. |

| Cargill Inc. | Global logistics & supply chain stability | Acts as the primary reliable backbone for the industry; leverages its massive global footprint to stabilize supply chains for protein isolates and concentrate demand during periods of commodity volatility. |

| Kerry Group | Taste, texture & functional masking | The “secret sauce” of the industry. Kerry’s data-intensive flavor charts and fermentation-based “umami/kokumi” technologies allow brands to solve the processing-taste gap, while their biotics platform targets the high-growth GLP-1 nutrition segment. |

| Meati Foods | Mycelium-based whole-food protein | The pioneer of the “whole-food” pivot. By delivering complete protein and fiber through a mycelium structure that requires minimal processing, Meati is the standard-bearer for the clean-label, non-isolate movement. |

The Shift in Competitive Moats

The “moat” around these leading companies has fundamentally changed since the early 2020s:

- From Volume to Versatility: Influencers are no longer simply selling the most protein; they are selling the most functional protein. Whether it is ADM’s high-solubility isolates for protein drinks or Kerry’s flavor masking for savory meat-free applications, these entities provide the technical expertise that allows food brands to innovate faster.

- The Data-Driven Formulation: Leading firms have integrated “formulation intelligence” into their offerings. By providing digital, real-time access to technical data, regulatory support, and clinical research (as seen with Kerry’s focus on probiotic/GLP-1 clinical data), they have transformed from ingredient suppliers into essential, strategic partners for global food retailers.

- The Clean-Label Arms Race: With the rise of the “processed” stigma, influencers are aggressively investing in R&D to shorten their clients’ ingredient labels. The most successful players are those who can provide the structural benefits of an isolate (texture, melt, stretch) while effectively marketing it as a “whole-food” solution.

7. Conclusion: The Path Forward

The plant-based protein industry has “grown up” in 2026. The era of blind hype is over; the era of product-market fit has arrived. By refocusing on clean labels, functional health, and whole-food sources like fungi, the industry is successfully moving out of the “alternative” shadow and into the mainstream protein architecture. The next four years will reward companies that prioritize nutrition, cost-efficiency, and absolute ingredient transparency.

Related: As the global meat industry faces both structural production shifts and evolving trade dynamics, staying ahead of market volatility is critical. Get the latest insights on export surges, pricing trends, and supply chain updates in our Global Meat Industry Outlook June 2026.

8. Sources and References

- Persistence Market Research: Global Plant-based Proteins Market Size & Share Report, 2033

- Future Market Insights (FMI): Plant-Based Protein Market Analysis 2026–2036

- Good Food Institute (GFI): 2026 State of the Industry: Plant-based meat, seafood, dairy, and ingredients

- Research and Markets: Plant-Based Protein Market Global Report 2026

- Meati Foods: Plant-Based Eating in 2026: What’s Next for Food Lovers

Is the plant-based protein market still growing, or has the “hype” peaked?

While the extreme “hyper-growth” of the early 2020s has stabilized, the market is not shrinking; it is rationalizing. The market is currently valued at USD 22.5 billion and continues to grow at a healthy 7.8%–9.5% CAGR. The growth is now driven by mainstream integration (e.g., flexitarians and functional food fortification) rather than just “vegan-only” product demand.

Why are consumers becoming skeptical of “processed” plant-based meats?

The skepticism stems from the complexity of ingredient lists in first-generation meat alternatives. Modern consumers are increasingly health-conscious and associate long lists of artificial binders, methylcellulose, and emulsifiers with “ultra-processed” foods. The industry is currently correcting this by pivoting toward whole-food, clean-label alternatives like mycelium and simple legume-based proteins.

What is the “Price Parity Gap,” and when will it close?

The price parity gap refers to the cost difference between plant-based meat and animal protein (currently 40–80% higher for plant-based). It remains the largest barrier to mass adoption. Closing this gap requires further investment in domestic protein crop supply chains, automated manufacturing, and reducing the industry’s reliance on high-cost, proprietary protein isolates. We expect price competitiveness to improve as large-scale food manufacturers continue to optimize their production infrastructure.

What is “Mycelium,” and why is it considered a game-changer?

Mycelium is the root structure of fungi. Unlike protein isolates derived from peas or soy that must be heavily processed and bound together to mimic meat, mycelium grows in a fibrous, branch-like structure that naturally replicates the texture of muscle tissue. It is considered a “whole-food” protein because it delivers fiber and amino acids without requiring intensive chemical processing, making it ideal for the current “clean-label” market.

What role does “Precision Fermentation” play in 2026?

Precision fermentation is a technological tool used to brew specific, high-value ingredients—such as specialized fats, heme (for flavor), or milk proteins (casein/whey)—using microorganisms. It allows brands to recreate the exact sensory experience (melt, stretch, sizzle) of animal products without using animals, effectively solving the “taste and performance” gap that has historically hampered the plant-based dairy and meat categories.

Are plant-based proteins nutritionally equivalent to animal proteins?

This is a subject of ongoing scrutiny. While soy is a complete protein, some plant-based sources are less bioavailable than animal-derived sources. In 2026, the focus has shifted toward “Protein Synergy”—blending different plant sources to ensure a complete amino acid profile—and fortification. Manufacturers are increasingly prioritizing nutritional metrics like PDCAAS (Protein Digestibility Corrected Amino Acid Score) to provide transparency to consumers.

Which region is leading the growth in plant-based proteins?

Asia-Pacific is currently the fastest-growing region (projected CAGR of 11.3%). This is driven by high rates of lactose intolerance, rapid urbanization, and a surging middle class that is increasingly integrating plant-based beverages and protein-rich snacks into their daily diets.