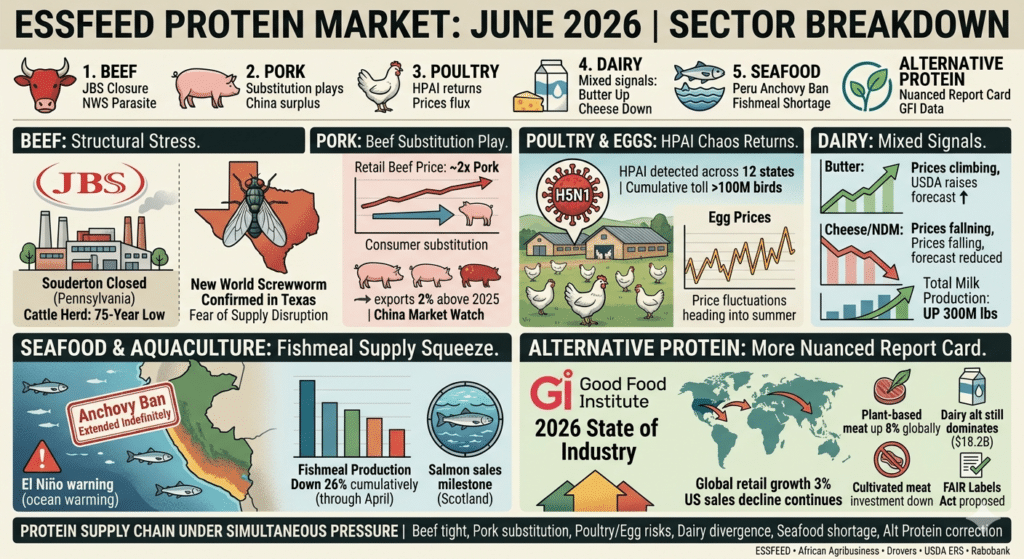

Published: 15 June 2026 | Category: Beef · Pork · Poultry · Dairy · Seafood · Alternative Protein

If you work anywhere along the food and beverage value chain — buying, selling, processing, or distributing protein — June 2026 is delivering a lot to keep track of. The beef industry is restructuring at pace under a historic supply crunch. A flesh-eating parasite is now loose in Texas. A legal war between Teamsters and Cargill is taking capacity offline. Egg prices are in flux after two years of HPAI chaos. Dairy is sending mixed signals. And in the seafood world, Peru has just extended an indefinite anchovy fishing ban that threatens to squeeze fishmeal supplies through the rest of the year. Oh, and the alternative protein sector just published its annual report card — and it’s more nuanced than either the boosters or the sceptics would have you believe.

Here is everything that matters, broken down sector by sector.

BEEF: An Industry Under Structural Stress

The JBS Shutdown and What It Really Means

The headline that rattled the meat industry this week was JBS USA’s announcement on 12 June that it will permanently close two US processing facilities: its beef plant in Souderton, Pennsylvania, and a value-added protein packaging operation in Memphis, Tennessee. The Souderton facility near Philadelphia employs around 1,700 people and had a daily slaughter capacity of approximately 2,000 head of cattle — making it one of the largest beef plants on the entire US East Coast.

JBS described the decision as a move to “strengthen operations for the future.” But the market read it differently. Analysts at Citi, who called the closure “faster than expected,” noted that Souderton alone represents roughly 8% of JBS’s US beef processing footprint, and that “the exceptional nature of the current environment” is what’s really driving this.

That environment, to be blunt, is a US cattle herd sitting at a 75-year low. After years of drought-forced culling, record-high input costs, and ranchers choosing to cash out rather than rebuild breeding stock at elevated prices, there simply aren’t enough cattle to keep the existing processing infrastructure profitable. JBS itself warned last month of widening losses in its US beef unit, now projecting a loss of somewhere between $350 million and $500 million for 2026.

The Souderton closure follows a string of industry capacity reductions that has been building for over a year. Tyson Foods closed its Lexington, Nebraska plant earlier in 2026, removing roughly 3,200 jobs and nearly 5% of total US beef capacity in one move. Tyson also cut a shift at its Amarillo facility. JBS had already announced the closure of a California plant last year and weathered a three-week labour strike at its Greeley, Colorado facility — where a new deal was only ratified in April.

For buyers in the food and beverage supply chain, the operational implication is straightforward: US beef availability will remain tight, and what capacity remains is running hard. JBS says Souderton’s production will be absorbed by other plants in its network — but those plants are already under pressure from a smaller cattle supply. The USDA’s latest forecast puts 2026 US beef production at 25.547 billion pounds, down 243 million pounds from its prior estimate, with further declines projected into 2027.

US beef exports have already reflected this pressure. April exports came in at 64,466 metric tonnes — nearly 19% below year-ago levels — as high US beef prices pushed buyers like Japan toward more competitively priced Australian product. The value of April beef exports fell 10% to $665.9 million, even as variety meat (offal) exports surged 20% — a sign that international buyers are seeking every available avenue to source US protein at viable cost.

The Cargill Labour War Escalates

If JBS’s plant closure is the biggest headline, the Cargill situation is the most combustible. Teamsters Local 455 filed formal unfair labour practice charges against Cargill on 10 June after the company cut off pay and benefits to workers locked out of its Fort Morgan, Colorado beef plant — a facility that processes cattle for consumers across the country and employs more than 1,700 union workers.

The lockout itself began on 20 May, following months of contract negotiations that ended with workers rejecting Cargill’s offer and the company citing “continued uncertainty around the union’s threatened work stoppage.” Harvest operations at Fort Morgan had already stopped on 23 April as the dispute intensified.

The Teamsters aren’t just crying foul over the lockout — they’re escalating on multiple fronts simultaneously. The union is publicly linking the labour dispute to a separate beef price-fixing case in which Cargill agreed to pay $32.5 million to settle claims that it conspired with other processors to keep beef prices artificially high. Cargill denied wrongdoing in that case. The Teamsters Food Processing Division is now exploring whether antitrust issues extend to alleged labour rate-fixing.

The latest bargaining session between Cargill and union representatives took place on 8 June, with no resolution. Cargill says it “remains committed to reaching a sustainable agreement” and insists Fort Morgan is “an important facility” it has no plans to close permanently — it invested $90 million in automation upgrades there as recently as June 2025.

But for the broader market, the practical reality is that a major US beef processing plant has been offline since late April. Cattle that would have gone through Fort Morgan have been redirected to other Cargill facilities. In an already capacity-constrained environment, that redirection adds further stress to the system.

New World Screwworm: Confirmed in Texas

Layered on top of all this is the confirmation earlier in June of New World Screwworm (NWS) in South Texas — the first detections in the US in decades. At least five cases have now been confirmed in calves in Zavala and La Salle Counties, approximately 50 miles from the Mexican border.

The NWS fly’s larvae feed exclusively on the living tissue of warm-blooded animals, entering through wounds and rapidly causing tissue damage that can kill cattle within days if untreated. The American Farm Bureau notes this arrives at the absolute worst possible moment for a cattle industry already operating at historically thin herd levels. USDA is deploying over 100 million sterile flies weekly as part of a broad containment strategy, and Congress has a $300 million eradication authorisation bill in progress.

The market impact is already being felt: cattle futures have responded to NWS news as a fundamentally bullish force for cattle prices — higher prices, that is, driven by fear of supply disruption rather than prosperity. If NWS spreads beyond its current zone and triggers mass treatment costs or herd selloffs, it could push back herd rebuilding timelines by years. The US-Mexico border is expected to partially reopen to live cattle imports in July, which would ease some supply pressure — but only if NWS containment holds.

PORK: Benefiting from Beef’s Pain — For Now

Pork is having an unusual moment. With retail beef prices running at nearly twice the price per pound of retail pork as of April 2026 (beef averaged 1.97x pork, compared to 1.32x in March 2011), American consumers are substituting down the protein ladder more than at any point in modern memory. That substitution effect is keeping pork demand elevated even as seasonal patterns would normally drag on hog futures during summer.

US pork exports remain strong, with 2026 total exports anticipated to reach around 7.14–7.19 billion pounds — a 2–3% increase on 2025 levels driven by strong demand in Mexico, a Japan rebound, and growing shipments to South Korea, Central America, and Taiwan. For the first two months of 2026, pork exports were running 2% ahead of year-ago levels in both volume and value.

Hog prices earlier this year were tracking toward what looked like a strong summer — the futures market in early February was pricing multiple contracts above $100/cwt through summer. That optimism has been scaled back somewhat. Current lean hog futures suggest prices won’t rally convincingly above $100/cwt until July-August at the earliest, reflecting a market hog inventory only 0.6% larger than last year and ongoing uncertainty about seasonal patterns. USDA is forecasting 2026 average liveweight hog prices at approximately $68.38/cwt — broadly in line with 2025’s $68.80, which itself was the highest since 2022.

The long-running structural surplus in China’s pork market — the world’s largest — is also worth watching. Reports from earlier this spring showed Chinese live hog prices dipping into deeply compressed ranges, reflecting a supply glut that has put pressure on Chinese producers. If Beijing successfully reins in overcapacity, that normalisation could stimulate Chinese import demand and further support US and European pork export markets through the second half of 2026.

One policy development worth flagging for the longer-term outlook: bipartisan legislation — the FAIR Labels Act of 2026 — has been introduced in both the Senate and House to mandate clearer labelling of plant-based and cultivated protein products, explicitly distinguishing them from conventional meat. Backed by both the National Cattlemen’s Beef Association and the National Pork Producers Council, the bill reflects conventional protein sectors’ growing concern about market positioning as alternative proteins gain ground.

POULTRY & EGGS: HPAI Returns, Prices Stabilise — But for How Long?

Bird Flu Is Back Across 12 States

The highly pathogenic avian influenza (HPAI) outbreak that has been battering US poultry since 2022 is proving stubbornly persistent. A June 2026 USDA APHIS update confirmed fresh H5N1 detections in commercial poultry flocks across 12 states, affecting laying hens, broiler chickens, and turkeys. The cumulative toll of this ongoing outbreak cycle has now surpassed 100 million birds depopulated since the outbreak began.

For egg prices, the picture in 2026 is more nuanced than the alarming 2025 story. After retail egg prices spiked to a record ~$5.90 per dozen in early 2025 — and wholesale prices hit even more extreme levels — a combination of flock rebuilding, stronger biosecurity, and moderating HPAI detections in early 2026 brought significant relief. By April 2026, retail egg prices had fallen 39.2% compared to April 2025, and the national laying flock had expanded to around 308 million hens on the back of aggressive restocking.

But the June HPAI detections are a warning that the recovery is not locked in. The USDA’s own Economic Research Service documents that flock depopulations translate into retail egg price increases within 6 to 8 weeks of outbreak confirmation. Multiple new June detections mean pressure is likely to return heading into summer, even if this outbreak wave isn’t yet at 2025 severity levels.

From a commodity pricing perspective: as of 12 June 2026, Grade AA butter settled at $1.6675/lb with CME cheese barrels at $1.42 and 40-lb blocks at $1.4875. Those are the egg-adjacent inputs for context — egg-layer productivity metrics for June should be watched closely by food manufacturers and foodservice operators who are planning Q3 purchasing decisions.

Broiler Production Holding Firm

The broader poultry sector is in a better position than beef. USDA’s May 2026 Livestock, Dairy and Poultry Outlook revised broiler production higher, reflecting strong hatchery and placements data. Broiler prices have been adjusted slightly lower in 2026 to reflect recent trends, but the overall picture is one of adequate supply with modest profitability — a relative haven compared to the beef sector’s structural stress.

DAIRY: Mixed Signals Across the Board

Dairy in mid-June 2026 is best described as a market of diverging signals. The USDA’s mid-month Dairy Market News reports that milk output in the eastern US is tightening due to summer heat — a seasonal pattern that typically provides some support to milk prices. But the broader price picture is heading in multiple directions at once.

As of the week ending 6 June, butter prices are climbing, averaging $1.61/lb and trending higher on expectations of stronger second-half demand. USDA has actually raised its butter price forecast on this basis. Cheddar cheese prices, by contrast, have been falling — down 3.1 cents per pound from the prior week to $1.61/lb — and USDA has lowered its 2026 cheese price forecast accordingly. Nonfat dry milk saw the sharpest decline, dropping 15.2 cents per pound in a single week to $1.97/lb, reflecting weaker export demand for this product category.

The composite all-milk price forecast for 2026 now stands at approximately $20.70 per hundredweight, reduced from last month’s projection. For 2027, the all-milk forecast is being lowered slightly to $20.90/cwt as lower cheese price expectations offset higher whey prices.

On the global stage, the June Global Dairy Trade (GDT) auction showed mixed results: anhydrous milk fat posted a strong 5.3% gain to $6,668/MT, and butter edged up 1.2% to $5,734/MT. But mozzarella fell 4.6% to $3,942/MT, skim milk powder dropped 3.0% to $3,457/MT, and whole milk powder declined 2.2% to $3,706/MT. The GDT Price Index has been broadly trending up since late 2025 following a strong run of consecutive gains earlier in the year.

For food manufacturers sourcing dairy commodities, the key takeaways are:

- Butter: buy forward where possible. Price momentum is up.

- Cheese: some softening creates procurement opportunity, but monitor HPAI impacts on dairy-adjacent markets.

- NDM/SMP: under pressure globally. Spot pricing may be favourable for buyers, but export demand trends warrant monitoring.

- Dry whey: nuanced. US domestic demand for protein ingredients remains robust, but recent price slippage of 0.3 cents/lb suggests the market is finding a new equilibrium.

On production volume, USDA has raised its 2026 US milk production forecast to 234.3 billion pounds — up 300 million pounds from last month — on higher output per cow. This is a healthy underlying supply picture, even as heat stress and regional factors create pockets of tightness.

One issue worth flagging for international dairy trade: organic milk exports from the US fell sharply in April 2026, down 26.7% year-on-year, reflecting structural challenges in the premium organic segment as well as general currency and competitiveness factors.

SEAFOOD & AQUACULTURE: Peru’s Anchovy Crisis Goes Indefinite

The Fishing Ban With No End Date

This is arguably the most significant supply chain development in the seafood sector right now, and it deserves close attention from anyone sourcing fishmeal, fish oil, or aquafeeds. Peru — which in a normal year accounts for around 20% of global fishmeal and fish oil supply — has just extended its anchovy fishing ban with no announced end date.

The ban, which had been running until 10 June 2026 in the north-centre zone of the country, was extended by the Peruvian Vice-Ministry of Fisheries under ongoing Coastal El Niño conditions. Warm water temperatures have dispersed the anchovy biomass and driven a high proportion of juvenile fish — a combination that makes responsible fishing nearly impossible. IMARPE, Peru’s marine science authority, will need to update its biological assessments before any lifting of the ban, which may come fully, partially, or gradually.

IFFO — the Marine Ingredients Organisation — has framed this with appropriate directness: “Peru accounts for a large share of global fishmeal and fish oil supply, implying that disruptions quickly tighten availability.” Enrico Bachis, IFFO’s Market Director, confirmed there is no announced end to the suspension.

The numbers behind this are stark. April 2026 global fishmeal production was already down 21% year-on-year, and cumulative production through April was 26% below 2025 levels. Fish oil production fell 19% year-on-year in April, with cumulative output down 14%. Denmark/Norway and African countries recorded the sharpest monthly declines alongside Peru. Only Spain (up 36% cumulatively) and the US (benefiting from a good Gulf menhaden season) bucked the trend.

For aquafeed producers and salmon, shrimp and marine finfish farmers globally, this is a serious and worsening supply squeeze. Fishmeal and fish oil remain difficult to replace at scale in high-performance aquafeed formulations in the short term. Longer-dated forward contracts and alternative ingredient sourcing strategies are becoming urgent operational priorities across the sector.

The wider backdrop makes this even more challenging: a Rabobank study from September 2025 projected that critical fishmeal shortages could arrive as early as 2028 even without this year’s disruption, given that aquaculture already consumes around 90% of the world’s fishmeal supply. At the same time, aquaculture output of salmon, marine finfish, and crustaceans is projected to expand by 12 million metric tonnes by 2033 — increasing the demand-supply mismatch.

NOAA Launches Aquaculture Research Institute

On a more constructive note, NOAA announced on 9 June the launch of the Cooperative Institute Fostering Aquaculture Research and Markets (CIFARM), a new initiative hosted by the University of New Hampshire in partnership with other universities and researchers, designed to advance American marine aquaculture. This is a welcome policy signal for a sector that has historically been under-resourced in the US compared to Norway, Chile, and other major aquaculture nations.

Scottish Salmon Hits £1.6 Billion in Sales

On the production side, Scottish salmon sales approached GBP 1.6 billion in the 52 weeks ending 18 April 2026 — an impressive milestone for the sector. Cross-sector alliance Prosper has urged the incoming Scottish government to prioritise salmon farming in its planning and regulatory reforms during its first 100 days in office, reflecting the sector’s growing economic footprint.

Separately, LAXEY — an Icelandic land-based salmon farmer — confirmed its new facility, constructed in just 10 months, is fully operational and performing as planned. Nordic Aqua Partners, another land-based salmon operator, posted a positive operational EBIT in March — the company’s first — signalling that the land-based salmon model may finally be approaching commercial viability after years of capital-intensive development.

Squid Moving North — An El Niño Signal

In a striking illustration of ocean warming’s impact on fisheries, NOAA reported on 12 June that West Coast squid vessels have followed market squid north into Oregon as ocean waters warm — prompting Oregon to adopt its first-ever regulations for squid fishing in the state. This is a real-time demonstration of El Niño reshaping wild-catch fisheries alongside its effects on terrestrial agriculture.

ALTERNATIVE PROTEINS: Growing Quietly, Struggling Loudly

The Good Food Institute’s 2026 State of the Industry reports, published in April but still generating industry discussion, offer the most comprehensive picture available of where alternative proteins stand heading into the second half of 2026.

The headline: global plant-based food retail sales reached $28.9 billion in 2025, up 3% from 2024. Plant-based meat and seafood specifically came in at $6.6 billion, up 8% year-on-year with volume purchases growing 3%. That’s a genuine rebound from the difficult 2023-24 period for the category.

The nuance, however, matters enormously for those tracking this sector commercially. That global growth masks significant divergence. US retail sales for plant-based meat continued to decline in 2025, while growth was largely driven by markets in Europe and Asia Pacific. Non-dairy alternatives — particularly milk substitutes — remain the dominant alternative protein category at $18.2 billion, dwarfing plant-based meat.

On investment, the picture is mixed. Companies in the plant-based ecosystem raised $450 million in 2025 — actually up from $309 million in 2024, an encouraging reversal. But fermentation-focused companies saw investment fall to $357 million from $651 million, and cultivated meat and seafood companies raised just $73.9 million, down from $139 million in 2024. Seven companies globally now have regulatory clearance to sell cultivated meat, with commercial sales permitted in Singapore, the United States, and Australia.

For the conventional protein industry, the key strategic takeaway from the GFI data is that the alternative protein correction of 2022–2024 did not kill the category. Plant-based sales are growing again globally, even if the US retail picture remains challenged. The FAIR Labels Act — backed by conventional meat industry lobbying — reflects a recognition that the regulatory terrain around labelling needs to be clarified before market competition intensifies further.

One development worth watching closely: the UPF (ultra-processed food) narrative is creating a new headwind for plant-based proteins in some markets. Several GFI-tracked brands reformulated or repositioned products in 2025 specifically in response to consumer concern about ingredient complexity. Beyond Meat’s repositioning of its Beyond Ground product — emphasising high protein rather than meat similarity — is a marker of where category messaging may be heading.

The Big Picture: A Protein Supply Chain Under Simultaneous Pressure

Step back from the sector-by-sector detail and a coherent pattern emerges. Every major conventional protein category is under supply-side stress right now — and many of those stresses are compounding each other.

Beef is constrained by the smallest US cattle herd in 75 years, made worse by NWS detections and a labour war at Cargill’s Fort Morgan plant. Poultry is recovering from HPAI damage but facing renewed outbreaks across 12 states. Dairy is managing summer heat stress and a complicated global price environment. Seafood and aquaculture are facing a potential structural fishmeal shortage made worse by Peru’s indefinite anchovy ban — itself driven by El Niño warming of the Pacific.

And all of this is happening against a backdrop of consumers who, despite higher prices, are broadly maintaining or increasing their protein consumption. Retail beef is at record highs. Pork is catching substitute demand spillover. Eggs went through a historic price shock and are only partially recovered. The food and beverage value chain is being asked to deliver more protein, more reliably, at costs that are increasingly difficult to predict.

For procurement, sourcing, and commercial teams, the practical priorities that emerge from this week’s news are:

- Beef: Forward-price. Processing capacity is falling and will not recover quickly. Record-high cattle prices are forecast to push even higher in 2027.

- Pork: Opportunity for substitution plays. Export demand is strong. Watch the China surplus normalisation as a potential future import demand signal.

- Poultry/Eggs: Monitor HPAI developments weekly. June detections across 12 states suggest another price spike is possible in Q3.

- Dairy butter: Upward price trajectory. Secure forward. Cheese and NDM softer — can be spot-purchased opportunistically.

- Fishmeal/fish oil: Treat the Peru situation as a structural supply disruption, not a temporary blip. Diversify ingredient sourcing now. Monitor IFFO updates closely.

- Alternative protein: Retailer and foodservice operators should track US consumer UPF sentiment — this is the biggest near-term headwind for category growth in the US market.

Sources

- Drovers — https://www.drovers.com

- MEAT+POULTRY — https://www.meatpoultry.com

- Meatingplace — https://meatingplace.com

- Beef Magazine / Farm Progress — https://www.beefmagazine.com

- USDA ERS: Cattle & Beef Market Outlook — https://www.ers.usda.gov

- Bloomberg / Transport Topics / Rural Radio (JBS closure) — https://www.ttnews.com

- Teamsters / PRNewswire (Cargill ULP charges) — https://teamster.org

- American Farm Bureau Federation (NWS, beef market) — https://www.fb.org

- National Hog Farmer — https://www.nationalhogfarmer.com

- The Pig Site — https://www.thepigsite.com

- Medical Daily / The Cooldown (HPAI poultry 2026) — https://www.medicaldaily.com

- USDA ERS: Food Price Outlook — https://www.ers.usda.gov

- IndexBox / USDA AMS: Dairy Market News June 2026 — https://www.indexbox.io

- Cheese Reporter — https://cheesereporter.com

- USDA ERS: Livestock, Dairy & Poultry Outlook May 2026 — https://www.ers.usda.gov

- SeafoodSource — https://www.seafoodsource.com

- IFFO — The Marine Ingredients Organisation — https://www.iffo.com

- Feed & Additive Magazine (Peru fishing ban) — https://www.feedandadditive.com

- Aquafeed.com — https://www.aquafeed.com

- NOAA Fisheries — https://www.fisheries.noaa.gov

- WeAreAquaculture — https://weareaquaculture.com

- Good Food Institute / Vegconomist (GFI 2026 State of Industry) — https://gfi.org

- National Hog Farmer (FAIR Labels Act) — https://www.nationalhogfarmer.com

- The Cattle Site (weekly protein report) — https://www.thecattlesite.com

FAQ: Protein Industry — June 2026

Q: Why is the US beef industry closing so many processing plants? The US cattle herd has fallen to its smallest level in 75 years, driven by prolonged drought, high input costs, and ranchers culling herds rather than absorbing losses. With fewer cattle to process, plants that were built for larger throughput become unprofitable to operate. JBS has now closed its Souderton, Pennsylvania plant (1,700 employees, 2,000 head/day capacity) in the latest move, following Tyson’s earlier Lexington, Nebraska closure and ongoing capacity reductions across the industry.

Q: What is the Cargill-Teamsters dispute about and how does it affect beef supply? Teamsters Local 455 filed unfair labour practice charges against Cargill on 10 June 2026 after the company locked out more than 1,700 workers at its Fort Morgan, Colorado beef plant and cut off access to pay and benefits. The Fort Morgan plant has not been harvesting cattle since 23 April. The dispute centres on wages, healthcare, and workplace safety in a new contract. The labour standoff means another major US beef processing facility is effectively offline in an already constrained market.

Q: Is bird flu (HPAI) still a threat to egg and poultry prices in 2026? Yes. Fresh HPAI H5N1 detections were confirmed in commercial poultry flocks across 12 US states in June 2026. While egg prices have fallen significantly from their early-2025 peak — retail prices were 39.2% lower in April 2026 than April 2025 — the USDA’s own research shows that new flock depopulations translate to retail price increases within 6–8 weeks. The June detections mean egg price pressure could return during Q3 2026.

Q: What is happening to dairy prices in June 2026? The picture is mixed. Butter prices are rising and the USDA has raised its butter forecast, expecting stronger second-half demand. Cheddar cheese prices are falling and NDM (nonfat dry milk) has dropped sharply. The all-milk price forecast for 2026 has been lowered to $20.70/cwt. On global markets, the GDT auction showed strong gains for anhydrous milk fat and butter, but declines for mozzarella, SMP, and WMP.

Q: Why is Peru’s anchovy fishing ban such a big deal for the global food industry? Peru typically produces around 20% of the world’s fishmeal and fish oil — the two most important feed ingredients for farmed fish, shrimp, and even livestock. An extended fishing ban (currently with no announced end date) under El Niño-driven warm water conditions is tightening global supply at a time when it was already declining. Global fishmeal production was already 26% below 2025 levels through April. Aquafeed producers sourcing fishmeal and fish oil face real near-term supply constraints.

Q: Is plant-based protein making a comeback? In global terms, yes — cautiously. The GFI’s 2026 State of the Industry report found global plant-based food retail sales grew 3% to $28.9 billion in 2025, with plant-based meat up 8% to $6.6 billion. However, US retail sales for plant-based meat continued to decline, and investment in cultivated meat fell from $139 million to $73.9 million. The UPF (ultra-processed food) narrative is creating consumer headwinds in some markets, particularly the US.

Q: What does New World Screwworm mean for beef prices and supply? NWS is now confirmed in multiple Texas counties, representing the first US detections in decades. The parasite threatens cattle through flesh-eating larvae, which can kill animals rapidly. Beyond the direct herd risk, NWS adds treatment costs and management burden at the worst possible time for an industry already operating at historic lows in cattle inventory. The American Farm Bureau warns a mass selloff triggered by NWS costs could delay herd rebuilding by years and prolong tight beef supplies well beyond 2027.

Q: Where should food and beverage professionals monitor protein sector news? ESSFeed (essfeed.com) covers the full F&B value chain including proteins. Key primary sources include Drovers, MEAT+POULTRY, Meatingplace, National Hog Farmer, USDA ERS, SeafoodSource, IFFO, The Dairy Site, and the Good Food Institute. For Africa-specific protein intelligence, African Agribusiness and Farmers Weekly cover the continent’s evolving protein landscape.

© ESSFeed 2026. All rights reserved. Republication permitted with attribution and link to original.