Corn, Wheat, Soybean and Grain Trade News – 48-Hour Roundup for Food & Beverage Industry Professionals

Published: June 12, 2026 | Compiled by ESSFeed Market Intelligence

Overview: Crops and Grains News for Food & Beverage Professionals

This 48-hour briefing tracks the latest developments across global crops and grains markets – corn, wheat, soybeans, barley and sorghum – with direct relevance to food and beverage manufacturers, ingredient buyers, millers, feed producers and supply chain planners. Key themes include the June WASDE report’s impact on grain futures, record Brazilian soybean output forecasts, EU grain production downgrades, rising input costs squeezing 2026 planting decisions, and continued volatility tied to weather and trade policy. Each item below is sourced from leading agricultural and grain trade publications and is current as of June 12, 2026.

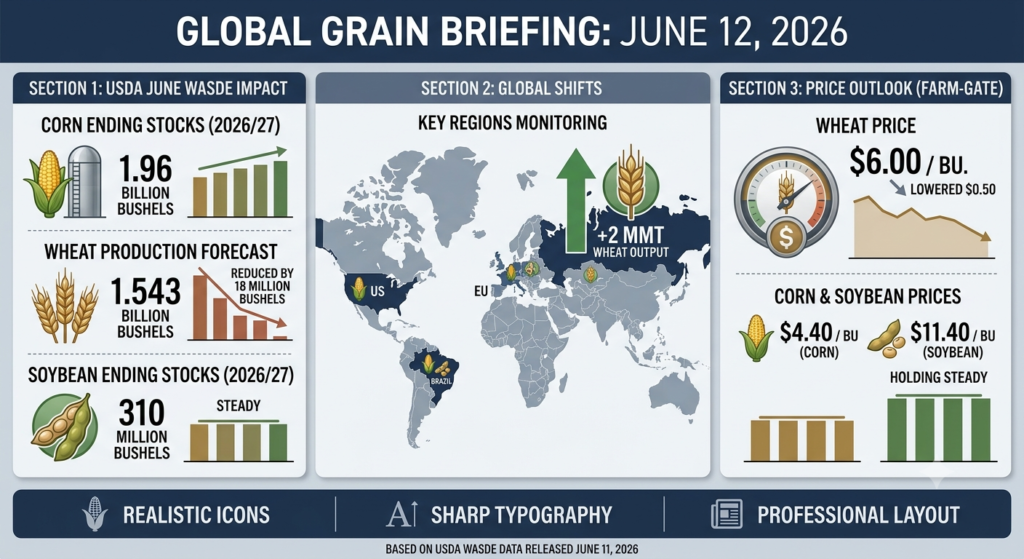

1. US Grain Markets React to June WASDE Report

The USDA’s June World Agricultural Supply and Demand Estimates (WASDE) report, released Thursday, June 11, 2026, triggered a broad selloff across US grain futures, with knock-on effects for ingredient costs across the food and beverage supply chain.

- Corn futures fell to fresh contract lows after the WASDE signalled ample US supplies, with soybeans also extending losses following further cuts to export projections.

- Winter wheat saw a modest boost after the USDA trimmed its estimate for the drought-affected crop, partially offsetting bearish pressure elsewhere in the grain complex.

- Market analysts noted that fund selling, which had been pressuring grains ahead of the report, eased only briefly before resuming on the bearish corn and soybean figures.

For F&B procurement teams, the combination of ample corn and soybean supply estimates points to continued downward pressure on feed and oil input costs in the near term, while wheat-based product costs may see modest upward pressure as the winter wheat crop estimate tightens.

2. El Niño Officially Declared – Implications for Summer Crop Weather

NOAA officially declared the onset of El Niño conditions this week, with agricultural meteorologists indicating a notable probability of the pattern reaching ‘very strong’ status by autumn 2026, a development that could influence US harvest conditions and winter weather.

- While El Niño has been confirmed, leading agricultural meteorologists caution against assuming it will be the dominant driver of summer growing-season weather across the Corn Belt.

- Crop production specialists are advising growers and grain buyers to monitor regional rainfall patterns closely rather than relying on broad El Niño-based seasonal forecasts.

Ingredient sourcing teams tracking corn, soybean and wheat input costs should treat El Niño headlines as one factor among several, with localized weather data remaining the more reliable near-term signal for crop condition risk.

3. EU Grain Output Revised Lower as Input Costs Bite

Europe’s grain outlook softened this week, with the COCERAL grain trade association revising its EU production estimates downward and industry commentary highlighting how rising fuel and fertiliser costs are reshaping farmer input decisions for the year ahead.

- COCERAL’s latest crop report points to a lower EU grains output forecast for the 2026 season, a shift likely to influence European wheat and barley availability for milling, brewing and feed manufacturers.

- Industry commentary highlights that soaring fuel and fertiliser prices are prompting many EU farmers to reduce input intensity, which could weigh on yields in the coming year and tighten supply for downstream processors.

- A new Growing Season Progress Report from Cereals Canada is providing updated detail on 2026 spring wheat seeding, crop conditions and quality – a useful benchmark for North American wheat buyers planning forward contracts.

For European and global wheat and barley buyers, the combination of a lower EU output forecast and rising input costs supports a cautious approach to forward contracting, particularly for milling wheat and malting barley.

4. Brazil Soybean Outlook Points to Record Harvest

Brazil’s soybean sector is on track for a record output season, according to the latest grain market outlook, reinforcing the country’s position as the dominant global supplier of soybeans for crush, feed and food-grade applications.

- Brazil’s soybean production forecast leads a broader record grain outlook for the country, a development that should support ample global soybean and soy oil availability into 2027.

- Continued expansion in Brazilian soybean supply is expected to keep downward pressure on global soybean meal and oil prices, benefiting feed manufacturers and food processors reliant on soy-based ingredients.

- Major trading houses are also expanding oilseed processing capacity in South America, including a new oilseeds plant being built in Argentina, signalling continued investment in regional crush capacity.

Food and beverage companies sourcing soy protein, soy oil or lecithin should view the Brazilian record-harvest outlook as a stabilising factor for soy input costs over the medium term, even as US soybean export demand softens.

5. Grain Trade, Milling and Logistics Developments

Several company-level and infrastructure developments this week are directly relevant to grain processors, millers and logistics planners across the F&B value chain.

- A major US flour milling company received its first wheat cargo shipment at a key inland port facility, supporting continued investment in US flour milling capacity for bakery and food manufacturing customers.

- A historic flour mill is reopening under new ownership after a multi-year closure, adding milling capacity back into the regional supply network for baked goods producers.

- European Flour Millers, the trade association representing EU milling interests, has elected new leadership for a two-year term, a development worth tracking for policy positions on wheat quality standards and trade.

- Equipment suppliers continue to roll out new grain handling technology, including upgraded conveyor relay systems designed to improve moisture control and throughput at grain storage and milling facilities.

- In Australia, planted winter-crop area estimates have crept higher, with forecasters now projecting what could be a record area for Western Australia’s 2026 winter grain crop – a positive signal for Southern Hemisphere wheat and barley supply later in the year.

These developments point to continued capital investment in milling and grain-handling infrastructure on both sides of the Atlantic and in the Southern Hemisphere, supporting medium-term capacity for flour, feed and malting operations.

6. Trade Policy and Tariff Developments Affecting Grain Flows

Trade policy remains a live factor for grain exporters and importers, with several reports this week touching on US trade relationships and their implications for agricultural commodity flows.

- Agricultural and food industry groups have issued a joint call for renewal of the USMCA trade pact, citing its importance to agricultural market access and economic security across North America.

- A recent study indicates that USMCA has measurably lowered food costs for US households, reinforcing the trade pact’s relevance to food and beverage cost structures.

- Commentary on the broader US trade outlook continues to flag uncertainty around tariffs despite recent court rulings, with analysts expecting continuation of trade policy volatility into the second half of 2026.

F&B companies with cross-border ingredient sourcing in North America should continue to monitor USMCA renewal discussions closely, given the direct link identified between the pact and food cost outcomes for US consumers.

7. Crop Conditions, Pest Pressures and Planting Progress

On-the-ground crop condition reports from major growing regions provide useful context for grain quality and yield expectations heading into the 2026 harvest season.

- Texas rice growers are facing a growing threat from the rice delphacid pest as rice acreage in the state declines, raising concerns about crop protection costs for remaining rice production.

- Agronomists are urging soybean growers to prioritise late-season herbicide passes, noting that delayed weed control has become one of the biggest threats to soybean yield potential this season.

- Corn growers are being cautioned against reducing nitrogen application rates as a cost-cutting measure, with agronomists warning this could undermine yield in a season already pressured by lower commodity prices.

- A new winter durum wheat crop in Kansas is nearing harvest, representing a notable diversification effort that could offer F&B buyers an additional domestic durum supply source for pasta and semolina production.

Collectively, these crop-level reports suggest yield risk is concentrated in pest pressure (rice), weed competition (soybeans) and input-cost-driven agronomic decisions (corn nitrogen rates) – all factors that ingredient buyers should factor into Q3 procurement risk assessments.

Key Takeaways for Food & Beverage Procurement Teams

- Corn and soybean prices are under pressure following the bearish June WASDE report, suggesting near-term stability or softening in feed and oil input costs.

- Winter wheat estimates were trimmed, a modestly bullish signal for wheat-based ingredient costs even as overall grain sentiment remains bearish.

- Brazil’s record soybean outlook and expanding South American crush capacity should support ample global soy supply into 2027.

- EU grain output forecasts have been revised lower amid rising input costs, warranting caution on European wheat and barley forward contracts.

- El Niño has been officially declared but should not be over-relied upon as a single predictor of Corn Belt summer weather.

- USMCA renewal remains a live policy issue with direct, measurable links to food costs – a priority watch item for North American supply chains.

Sources and Additional References

The following industry publications were reviewed for this report and provide ongoing coverage of global crops, grains and agribusiness markets:

- AgWeb – Farm Journal – https://www.agweb.com/

- World Grain (Sosland Publishing) – https://www.world-grain.com/

- Farm Progress – https://www.farmprogress.com/

- Grain Central – https://www.graincentral.com/

- FAO Newsroom – https://www.fao.org/newsroom/en

- Agriculture.com – https://www.agriculture.com/

- AgriCulture Dive – https://www.agriculturedive.com/

- African Agribusiness – https://africanagribusiness.com/

- AgDaily – https://www.agdaily.com/

- CropLife – https://www.croplife.com/

- Feed & Grain – https://www.feedandgrain.com/

- Grains Prices – https://grainsprices.com/

- Farms.com – https://www.farms.com/

- Grain Journal – https://www.grainjournal.com/

- The Western Producer – https://www.producer.com/

- Pro Farmer – https://www.profarmer.com/

- All Ag News – https://www.allagnews.com/

- USDA Foreign Agricultural Service – Data & Analysis – https://www.fas.usda.gov/data/search

Frequently Asked Questions: Crops and Grains Market News

What caused grain prices to drop this week?

The June WASDE report from the USDA, released on June 11, 2026, signalled ample US corn and soybean supplies, prompting a broad selloff in grain futures. Corn fell to contract lows while soybeans extended recent weakness.

How does the WASDE report affect food and beverage ingredient costs?

The WASDE report is a key reference point for grain and oilseed pricing globally. Bearish supply estimates, as seen in the June report, tend to ease near-term cost pressure on corn-based sweeteners, animal feed and soybean oil, while a tighter wheat estimate can support flour and bakery ingredient costs.

What is the outlook for Brazil’s soybean crop in 2026?

Brazil is forecast to produce a record soybean harvest, reinforcing its position as the world’s leading soybean supplier. This supports ample global availability of soybean meal and oil for feed and food manufacturing into 2027.

How is the EU grain outlook changing?

COCERAL has revised its EU grains output forecast lower for 2026, with rising fuel and fertiliser costs prompting farmers to reduce input intensity. This points to potentially tighter European wheat and barley supplies for millers, bakers and brewers.

What does the El Niño declaration mean for crop production?

NOAA has officially declared El Niño conditions, with a meaningful chance of reaching ‘very strong’ status by autumn. However, agricultural meteorologists caution that El Niño alone should not be treated as the primary driver of Corn Belt summer weather, and localized forecasts remain more reliable for crop risk assessment.

Why does USMCA matter for grain and food costs?

A recent study found that the USMCA trade pact has measurably lowered food costs for US households. Agricultural and food industry groups are calling for its renewal, making ongoing USMCA negotiations a key watch item for North American grain and ingredient supply chains.

What pest and crop condition risks are emerging for the 2026 season?

Key risks include rising rice delphacid pest pressure in Texas rice production, the importance of timely late-season herbicide applications for soybean yield protection, and warnings against cutting corn nitrogen rates despite lower commodity prices, which could undermine yield potential.

How often is this crops and grains report updated?

This report reflects news gathered from leading agricultural and grain trade publications within a 48-hour window as of June 12, 2026. For the latest updates, refer to the sources listed in the Sources and Additional References section above.