June 9, 2026

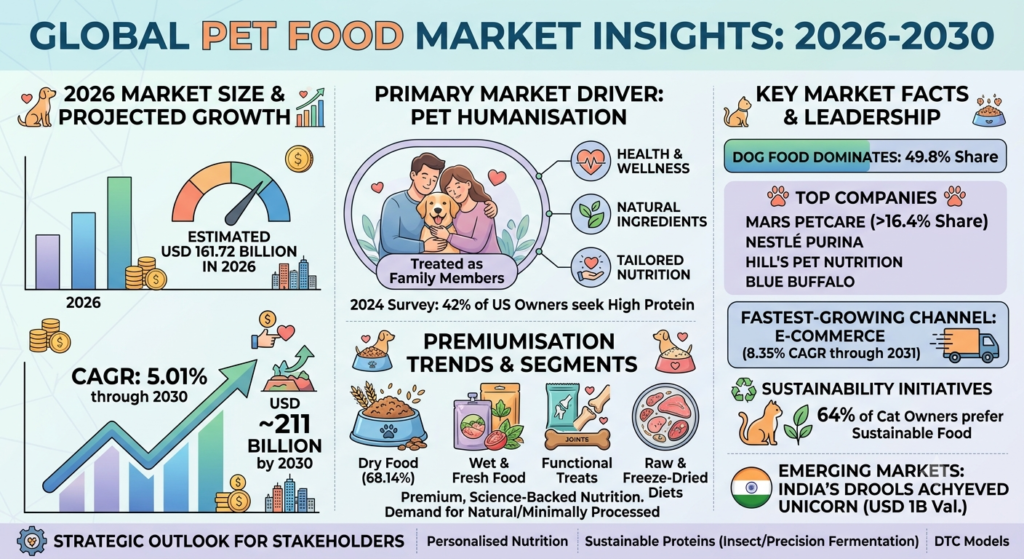

Revenue in the global pet food market amounts to USD 161.72 billion in 2026, with the market expected to grow at a CAGR of 5.01% through 2030. The global pet food industry is one of the most remarkable commercial stories in the modern food and beverage sector. It is a market defined by extraordinary consumer loyalty, consistent recession resilience, and a structural growth dynamic — the humanisation of pets — that shows no signs of abating. When a pet owner chooses between their own premium meal and their dog’s dinner, the dog frequently wins.

In 2026, the global pet food market sits at the intersection of the most powerful consumer forces in the food industry. Pet humanisation — the treatment of pets as family members with health, wellness, and dietary needs equivalent to human family members — has graduated from a cultural observation to the primary commercial driver of the industry’s most valuable growth segments. The premium trend derives from the humanisation of pets, which drives demand for products with natural or minimally processed ingredients, specific life-stage formulas and tailored nutrition. A 2024 Statista survey found that 42% of US pet owners saw high protein as a key factor when choosing a pet food brand.

The result is a market where consumer willingness to spend on pet nutrition rivals — and in many cases exceeds — their willingness to spend on their own food. Average annual spend per pet is projected to reach USD 1,445 in 2026, demonstrating a willingness to invest in premium, science-backed nutrition.

This report provides the most comprehensive publicly available analysis of the global pet food industry in 2026 — covering market scale, product categories, the humanisation and premiumisation revolution, alternative proteins, personalised nutrition, e-commerce, sustainability, regional dynamics, key challenges, strategic outlook, leading companies, FAQ, and full sources.

Executive Summary: The 2026 Pet Food Landscape

The global pet food industry in 2026 is defined by a “human-grade nutrition” imperative. Pet owners — particularly millennials and Gen Z who have adopted pets at extraordinary rates and treat them as children — are applying the same nutritional standards, ingredient scrutiny, and health consciousness to their pets’ food that they apply to their own.

Key Takeaways for Stakeholders:

The global pet food market is valued at USD 135–162 billion in 2026, growing at a CAGR of 5–6.2% toward USD 191–284 billion by 2031–2034.

Mars Petcare leads with over 16.4% global market share: Mars Petcare led the pet food market with over 16.4% market share in 2025, influencing the industry by driving demand for science-aligned, balanced nutrition and broad product accessibility across multiple retail formats.

Dog food dominates: Canine formulations account for 49.8% of the global pet food market share in 2026 due to larger daily caloric volume requirements per animal.

Dry food is the largest format: Dry pet food accounts for 68.14% of the market in 2026, remaining the most preferred option especially among dog owners for its convenience, shelf life, and health benefits including promoting oral health.

E-commerce is the fastest-growing channel: E-commerce channels are forecast to rise at an 8.35% CAGR through 2031.

India’s Drools achieves unicorn status: In May 2025, Indian pet food startup Drools achieved unicorn status with a USD 1 billion valuation following a minority investment from Nestlé.

Sustainability becomes competitive necessity: Around 64% of cat owners globally prefer sustainability when choosing cat food.

Table of Contents

1. Market Overview: Scale, Structure and Segments

Global Valuation

Market size estimates for the global pet food industry in 2026 vary across research sources, reflecting differences in category scope. The consensus range places the 2026 market value at USD 135–162 billion for core pet food, with the broader pet food and treats category reaching USD 152–162 billion. The global pet food and treats market was valued at USD 145.2 billion in 2025, projected to grow from USD 152.1 billion in 2026 to USD 259 billion by 2035, representing a 6.1% CAGR.

The global pet food market reached USD 132.4 billion in 2025. Sales are poised to cross USD 141.0 billion in 2026 and USD 263.8 billion by 2036. Dry (kibble) is anticipated to lead by product type with 42.5% share in 2026.

The industry serves pets across a broad species range — dogs and cats collectively account for approximately 85–90% of all pet food revenues — with the remainder encompassing small animals (rabbits, guinea pigs, hamsters), birds, fish, reptiles, and other companion animals.

Industry Structure

The global pet food market remains moderately consolidated. Leading companies include Mars Petcare, Nestlé Purina PetCare, Hill’s Pet Nutrition, Blue Buffalo (owned by General Mills) and Cargill. These manufacturers are increasing R&D investment in personalised nutrition, functional ingredients and sustainable protein alternatives including insect- and plant-based proteins as premium and natural segments continue to expand.

The industry structure mirrors that of the broader food and beverage industry — dominated at the top by multinational giants with global scale, extensive distribution, and deep R&D capability, but increasingly challenged by a wave of premium, DTC, and specialist challenger brands that are capturing the most valuable consumer segments.

2. The Humanisation Megatrend: Pet Food’s Defining Commercial Dynamic

What is Pet Humanisation?

Pet humanisation is the progressive cultural and psychological shift through which pet owners increasingly treat their animals as family members with equivalent health, emotional, and nutritional needs to human family members. This shift — observable across every major pet-owning market globally — manifests commercially in the willingness of pet owners to pay premium prices for pet food products that reflect their own nutritional values and health priorities.

The premium trend derives directly from the humanisation of pets, which drives demand for products with natural or minimally processed ingredients, specific life-stage formulas, and tailored nutrition. Brands must adapt quickly as consumers prioritise wellness-focused premium offerings.

The demographic driver of pet humanisation is generational — millennials and Gen Z, who are delaying parenthood or choosing not to have children, are channelling parenting instincts, emotional investment, and significant financial resources into their pets. These consumers have grown up with health consciousness and clean-label expectations as baseline requirements, and they apply the same standards to what they feed their animals.

From Commodity to Premium

Pet owners, particularly millennials and Gen Z, are extending their own dietary values — such as flexitarianism, veganism, and environmental responsibility — to their pets. The rapid expansion of plant-based and alternative protein pet food is increasingly reshaping global market demand, driven by converging trends in pet humanisation, sustainability concerns, and heightened awareness of animal protein supply-chain risks.

The commercial result of humanisation is a progressive trading-up dynamic across the pet food category. Conventional kibble — the commodity backbone of the market — is losing share to premium dry food, wet and fresh formats, raw and freeze-dried diets, and functional treats. The price points commanded by premium pet food products — and the willingness of consumers to sustain these spending levels — are extraordinary by any conventional food category standard.

3. Product Categories: Deep Dives

Dry Pet Food (Kibble): The Category Backbone

Dry pet food commands a 59.10–68.14% market share in 2026 due to its superior shelf stability, ease of handling, and economic pricing compared to wet and fresh alternatives. Dry kibble remains the foundation of the global pet food market by volume — affordable, convenient, nutritionally complete, and available in every retail channel globally. However, within the dry food segment, a pronounced premiumisation is occurring: standard commodity kibble is losing share to premium dry formulations featuring high-meat content, grain-free recipes, novel protein sources, functional ingredient inclusions, and life-stage specificity.

The grain-free movement — which saw explosive growth in the 2010s and early 2020s — has been partially moderated by FDA investigations into a potential link between grain-free diets and dilated cardiomyopathy (DCM) in dogs. However, the broader trend toward reduced carbohydrate, higher protein, minimally processed dry food formulations remains commercially strong.

Wet and Fresh Pet Food

Wet pet food — encompassing canned food, pouches, trays, and chilled/fresh formats — is growing significantly faster than dry food, driven by its appeal for palatability, hydration (particularly important for cats), and its visual similarity to “real food” that resonates with humanisation-oriented pet owners.

The fresh and refrigerated pet food segment — including brands like Nom Nom (acquired by Mars Petcare), The Farmer’s Dog, and Ollie — represents the fastest-growing premium format in the industry. These products resemble home-cooked meals, are delivered via subscription DTC models, and command retail prices of USD 8–15+ per day of feeding — multiples above conventional kibble. Companies are responding to humanisation by launching fresh, refrigerated, and gourmet-style pet foods to capture this premium segment.

Raw and Freeze-Dried Diets

The raw pet food movement — feeding dogs and cats uncooked meat, bone, and offal, either fresh-raw or in freeze-dried form — has grown from a fringe practice to a commercially significant premium segment. Proponents argue that raw feeding more closely aligns with the ancestral diet of dogs and cats, delivering benefits including improved coat quality, digestibility, and energy levels. The segment faces regulatory scrutiny and food safety concerns — the FDA-posted voluntary recall of Albright’s raw dog food increased scrutiny of raw and fresh pet food formats — but continues to grow driven by committed premium consumers.

Functional Treats and Supplements

The functional treats segment continues to grow with premium focus. After the pandemic, pet enthusiasts prioritised their pets more, resulting in a surge in pet treats. Dog and cat treats remain as popular as they were during the pandemic.

Functional treats — supplements for dental health, joint support, anxiety management, digestive health, coat and skin quality, immune function, and weight management — are one of the fastest-growing sub-categories in pet food. Pet owners are extending their own supplement habits to their animals, creating demand for products like probiotic chews, omega-3-enriched treats, CBD-infused calming products, and joint support glucosamine treats.

Therapeutic and Prescription Diets

The veterinary/therapeutic pet food segment — clinically formulated diets prescribed by veterinarians for specific health conditions including kidney disease, obesity, diabetes, digestive disorders, urinary tract health, and cancer — is growing at premium price points as the humanisation trend drives investment in pet healthcare.

In January 2024, Blue Buffalo’s General Mills brand released the first vet-prescribed food clinically proven to support dogs undergoing cancer treatment. Hill’s Science Diet and Royal Canin (Mars) are the market leaders in veterinary nutrition, leveraging their clinical credentials and veterinarian partnership networks to maintain leadership in this high-margin segment.

4. Alternative Proteins: The Sustainability Revolution in Pet Food

The Case for Alternative Protein in Pet Food

The conventional pet food industry is heavily dependent on animal-derived protein from livestock and poultry — the same supply chains that generate significant greenhouse gas emissions, land use, and water consumption. One third of pet owners are trying to reduce their own meat consumption. Amid rising flexitarianism among pet owners, alternative proteins, especially insect-based, are gaining ground in pet food.

The carbon footprint of feeding the world’s pets is substantial — a study estimated that if the world’s pets constituted a country, it would rank fifth globally for meat consumption. This creates a compelling sustainability imperative for protein diversification in pet food, and a commercial opportunity for the brands that can credibly deliver alternative protein products without compromising nutritional completeness or palatability.

Insect Protein

Major players including Mars have launched plant-based products, and Nestlé Purina entered insect-based products through Beyond Nature’s Protein pet food containing both insect and plant protein. Black soldier fly larvae (BSFL) and other insect meal sources offer a nutritional profile that matches conventional animal protein — high-quality amino acid composition, excellent digestibility, and significant micronutrient content — while requiring a fraction of the land, water, and feed inputs of conventional livestock protein and generating significantly lower greenhouse gas emissions.

In May 2026, Hill’s announced their association with Bond Pet Foods using precision fermentation. Hill’s is the only major corporate to bring insect-based protein to market among the large-scale conventional manufacturers — a first-mover position in a segment expected to grow significantly as consumer acceptance increases and production scales drive cost parity.

Precision Fermentation Pet Food

Companies are developing AI-enhanced yeast strains that provide up to 28% more protein than conventional sources. Additionally, innovative technologies such as “air protein”, which converts CO₂ into protein hydrolysate, are emerging as scalable feed options that support sustainability goals.

Bond Pet Foods’ precision fermentation technology — producing animal-identical proteins (including chicken, beef, and fish proteins) through microbial fermentation rather than animal slaughter — represents the longest-term disruption potential for the conventional pet food protein supply chain. The ability to produce complete, species-specific animal proteins with a fraction of the environmental footprint of conventional livestock, without any animal welfare concerns, is commercially compelling for a category whose consumers are increasingly aligned with sustainability and animal welfare values.

Plant-Based Pet Food

Plant-based pet food — while a smaller commercial segment than insect or fermentation protein — is growing driven by the extension of pet owners’ own dietary values to their animals. The nutritional completeness of plant-based diets for dogs (omnivores) is well-established; plant-based diets for cats (obligate carnivores) present greater nutritional challenges given cats’ specific requirements for taurine and arachidonic acid that are only found naturally in animal tissue.

5. Personalised and Precision Pet Nutrition

AI-Powered Pet Nutrition

Recent breakthroughs include AI-powered personalised diets, FDA-approved therapeutic foods, and alternative protein sources, signalling a dynamic future for pet nutrition. The personalised nutrition revolution that is reshaping the human supplement industry is simultaneously transforming the premium pet food market. AI-powered platforms assess individual pets’ breed, age, weight, health conditions, activity levels, and life stage to generate personalised feeding recommendations and custom-formulated diet plans.

Mars Petcare’s investment in Nom Nom — a DTC fresh pet food brand that uses pet health data to personalise feeding protocols — and the broader DTC subscription model adopted by The Farmer’s Dog, Ollie, and their growing roster of competitors are the commercial vanguard of this personalisation trend.

Life-Stage and Breed-Specific Nutrition

Demand rises for natural, minimally processed and tailored nutritional products. Specific life-stage formulas and tailored nutrition sit at premium price ranges. Breed-specific nutrition — recognising that a Great Dane has different jaw structure, exercise capacity, and nutritional requirements than a Chihuahua — is a well-established Royal Canin commercial strategy that is being extended by a growing number of premium brands. Life-stage specificity (puppy/kitten, adult, senior) is now standard across premium and super-premium brands, with sophisticated health condition targeting — joint health, dental, cognitive, weight management — adding further personalisation dimensions.

Veterinarian-Recommended Formulations

The veterinary channel remains the most trusted source of pet nutrition guidance for premium consumers. Brands with strong veterinary endorsement — Hill’s Science Diet, Royal Canin, Purina Pro Plan — command premium pricing and exceptional consumer loyalty through the authority signal of professional recommendation. The expanding network of corporate veterinary practices (many owned by the same multinationals that produce the pet food) creates a commercial integration between healthcare recommendation and product sales that is unique to the pet food industry.

6. E-Commerce: The Channel Transforming Pet Food

Online Dominance Among Premium Brands

E-commerce channels are forecast to rise at an 8.35% CAGR through 2031, the fastest-growing channel in the global pet food market. The subscription DTC model has proven extraordinarily well-suited to the pet food category — pets need feeding every day on a predictable schedule, creating natural recurring purchase patterns that convert easily to subscription models. The convenience of home delivery eliminates the burden of carrying heavy bags of kibble from the car, and the personalised unboxing experience creates emotional brand engagement.

Brands are aggressively acquiring DTC startups while expanding into emerging markets and functional nutrition. These players are increasingly acquiring DTC startups like Mars’ investment in Nom Nom.

The Amazon and Chewy Duopoly

In the United States — the world’s largest pet food market — Chewy and Amazon together dominate online pet food sales. Chewy’s subscription-based “Autoship” model has proven particularly effective at driving customer loyalty and predictable recurring revenue, with Autoship customers spending significantly more per year and churning at materially lower rates than one-time purchasers. Chewy’s addition of veterinary telehealth, pharmacy, and insurance services is transforming it from a pet food retailer into a comprehensive pet healthcare platform.

7. Sustainability: The Green Pet Food Imperative

Packaging Sustainability

Nearly 60% of pet owners try to reduce plastic usage, and 45% prefer sustainable packaging. Mars is implementing packaging for its Sheba brand with recycled plastic in Europe. The pet food industry generates substantial packaging waste — particularly from the single-serve wet food pouches and trays that are growing fastest in the premium segment. The transition to recyclable, compostable, and reduced-plastic packaging is accelerating under both regulatory pressure (EU packaging regulations) and consumer demand.

Protein Sustainability

The animal protein supply chain for pet food — which uses billions of kilograms of meat, poultry, and fish annually — represents the industry’s most significant sustainability challenge. The shift toward alternative proteins (insect, precision fermentation, plant-based), the use of lower-carbon animal protein by-products from human food processing, and the development of carbon-verified sustainable meat sources are all part of the industry’s response to this challenge.

Hill’s have spoken of reducing emissions by 90% by 2040, with the association with Bond Pet Foods and precision fermentation as a key pathway to achieving this ambition.

The Sustainability-Nutrition Balance

The key commercial challenge in sustainable pet food is maintaining the palatability, nutritional completeness, and health credentials that premium pet food consumers demand while reducing the environmental footprint. Alternative proteins that deliver all the above while meeting sustainability criteria — insect meal that dogs actually enjoy, precision fermentation proteins with species-identical amino acid profiles, and plant-based formulations with full nutritional completeness — represent the commercial sweet spot that the industry’s most innovative brands are racing to occupy.

8. Regional Dynamics

North America: Premium Leadership and Market Maturity

North America dominated the pet food market with a market share of 41.71% in 2025. The US market — valued at approximately USD 43 billion for pet food alone in 2026 — is the world’s most mature, most premium-oriented, and most commercially sophisticated pet food market. Pet ownership rates in the US are among the highest globally, and the cultural embedding of pet humanisation is most advanced.

The US market is characterised by fierce competition across every tier — Mars and Purina defending their mass-market positions, Hill’s and Royal Canin dominating the veterinary channel, Blue Buffalo (General Mills) leading in natural premium, and a growing ecosystem of DTC fresh and raw brands capturing the ultra-premium consumer. Private label is gaining share in the value tier, creating additional margin pressure on mid-market brands.

Asia-Pacific: The Growth Engine

China and India display peak growth momentum at anticipated 8.2% and 7.6% respective CAGRs. The Asia-Pacific region is expected to be the fastest-growing region in the pet food market at a CAGR of 8%.

China’s pet ownership boom — driven by urbanisation, delayed marriage and childbirth among younger generations, and the adoption of pets as companions in smaller urban households — is creating one of the most dynamic new pet food markets in the world. India’s pet food startup Drools achieved unicorn status with a USD 1 billion valuation following a minority investment from Nestlé in May 2025, signalling the scale of investment appetite for emerging market pet food brands as the category transitions from premium niche to mainstream consumption.

Japan and South Korea have highly sophisticated pet food markets characterised by exceptionally high average spend per pet, premium brand preference, and a strong cultural tradition of treating pets as family members that predates the Western humanisation trend.

Europe: Sustainability Leadership and Regulatory Sophistication

Europe leads globally in sustainable pet food practices, alternative protein adoption, and regulatory standards for pet food ingredients and marketing claims. The EU’s Farm to Fork strategy and associated sustainability regulations are creating the most demanding operating environment for conventional animal protein-based pet food globally, accelerating the transition to alternative proteins and sustainable sourcing at a pace that is ahead of other major markets.

9. Critical Risks and Challenges

Raw Material Cost Volatility

Meat and grain price swings of up to 25% compress margins, prompting diversification into alternative proteins and hedging strategies. The pet food industry’s heavy dependence on animal protein creates significant exposure to agricultural commodity price volatility — the same forces affecting human food production (climate events, geopolitical disruption, energy costs) directly affect pet food input costs.

Regulatory Complexity

The US maintains 25% tariffs on Chinese pet food ingredients, raising production costs, while the EU’s new carbon tax (2026) pressures non-sustainable imports. Regulatory complexity across major markets — different ingredient approvals, labelling requirements, health claim standards, and safety testing protocols — creates significant compliance costs for multinational pet food brands and creates barriers to market entry that disadvantage innovative smaller brands relative to established incumbents.

Food Safety and Recall Risk

The pet food industry is subject to significant food safety scrutiny and recall risk — contamination events (most notoriously, the 2007 melamine contamination of pet food ingredients from China that killed thousands of pets) have demonstrated the catastrophic brand and commercial consequences of food safety failures. The FDA-posted voluntary recall of Albright’s raw dog food increased scrutiny of raw and fresh pet food formats.

The Premiumisation Affordability Ceiling

While the humanisation trend is powerful, it is not unlimited in its commercial reach. Economic pressures — inflation, cost of living increases, and recessionary conditions — can moderate or partially reverse premiumisation trends as pet owners make difficult household budget decisions. The industry’s most significant risk is the point at which premium pet food pricing exceeds the willingness to pay even of strongly humanisation-oriented pet owners.

10. Strategic Outlook for Stakeholders

Actionable Recommendations

Build Fresh and Functional Capability for the Premium Segment: The fresh pet food segment is growing faster than any other format in the industry. Brands with genuine fresh feeding credentials — human-grade ingredients, short ingredient lists, refrigerated or freeze-dried formats, subscription DTC delivery — are capturing the most commercially valuable pet owner segment and building exceptional customer lifetime value through subscription loyalty.

Invest in Alternative Protein R&D Before Scale Economics Change: Manufacturers are increasing R&D investment in personalised nutrition, functional ingredients and sustainable protein alternatives including insect- and plant-based proteins. The alternative protein cost curves are moving rapidly toward parity with conventional animal protein. Brands that invest in alternative protein capability now will have first-mover advantages in formulation quality, consumer trust, and regulatory approval before the transition becomes competitively obligatory.

Build Veterinary Channel Relationships as a Premium Moat: The veterinary recommendation is the most powerful trust signal in the pet food category, enabling premium pricing that is largely immune to commodity competitive pressure. Investment in veterinary education, clinical nutrition research, and veterinary practice partnerships creates a defensible competitive advantage that cannot be replicated through marketing spending alone.

Capture Asia-Pacific Growth Through Local Brand Investment: In May 2025, Nestlé’s minority investment in Indian pet food startup Drools, which achieved unicorn status at USD 1 billion valuation, illustrates the preferred model for Asia-Pacific market entry — backing locally relevant brands with global ingredient, technology, and distribution capability rather than attempting to impose Western-developed brands on markets with distinct cultural, culinary, and consumption dynamics.

Strategic Summary: The 2026 Pet Food Business Model

| Strategic Priority | Traditional Approach | 2026 Competitive Standard |

|---|---|---|

| Product Philosophy | Nutritionally complete commodity | Human-grade, functional, personalised nutrition |

| Protein Strategy | Conventional meat and poultry | Diversified including insect, fermentation, plant-based |

| Distribution | Mass retail and pet specialty | DTC subscription + e-commerce + veterinary channel |

| Personalisation | Breed size and life-stage basic | AI + health data + individual pet profiling |

| Sustainability | Recycled packaging targets | Full protein supply chain transformation |

| Innovation | Incremental formula improvement | Precision fermentation + therapeutic + fresh formats |

11. Leading Industry Companies

| Company | Region | Strategic Focus |

|---|---|---|

| Mars Petcare | USA/Global | Market leader with 16.4%+ share. Brands include Pedigree, Whiskas, Royal Canin, Sheba, Eukanuba, Iams, Cesar, Nom Nom (DTC fresh). Emphasises science-aligned nutrition, diverse formulations, and sustainability across multiple retail formats. Plasticcontainercity |

| Nestlé Purina PetCare | Switzerland/Global | Supports industry momentum through strong research capabilities, advanced nutrient profiling, and consistent innovation in treats and meal formats. Wide distribution footprint reinforces consumer trust. Plasticcontainercity Brands include Purina ONE, Pro Plan, Felix, Friskies. Minority investment in Indian unicorn Drools. Industryresearch |

| Hill’s Pet Nutrition (Colgate-Palmolive) | USA/Global | Elevates industry focus on clinically guided, veterinarian-supported diets, setting benchmarks for therapeutic and functional nutrition trends. Plasticcontainercity Brands: Science Diet, Prescription Diet. Partnership with Bond Pet Foods for precision fermentation. |

| General Mills (Blue Buffalo) | USA/Global | Leading natural premium pet food through Blue Buffalo. Released first vet-prescribed food clinically proven to support dogs undergoing cancer treatment. Industryresearch |

| J.M. Smucker Company | USA | Capitalises on celebrity-endorsed natural brands and affordable premium segments. Industryresearch Brands include Meow Mix, Milk-Bone, Pup-Peroni, Nature’s Recipe. |

| The Farmer’s Dog | USA | Leading US DTC fresh dog food subscription brand. Human-grade ingredients, personalised portions, direct home delivery. Redefining the premium end of the market. |

| Drools | India | Achieved unicorn status at USD 1 billion valuation following Nestlé minority investment in May 2025. Leading Indian pet food brand. Industryresearch |

| Cargill | USA/Global | Major pet food ingredient supplier and contract manufacturer. Investing in sustainable protein alternatives for pet food applications. |

| ADM | USA/Global | Key pet food ingredient supplier across proteins, fibres, and functional ingredients. Alternative protein development for pet food formulations. |

| Chewy Inc. | USA | America’s leading e-commerce pet retailer. Autoship subscription model driving exceptional customer lifetime value. Expanding into veterinary telehealth and pharmacy. |

Related: As the processed food industry grapples with stricter clean-label regulations and a massive pivot toward nutrient-dense convenience, the landscape for manufacturers is rapidly evolving. We dive into the critical production, regulatory, and market trends defining the year in our Global Processed Food Industry Report 2026.

Frequently Asked Questions (FAQ)

What is the global pet food market size in 2026?

The global pet food market is valued at approximately USD 135–162 billion in 2026, depending on the scope of measurement. Statista places the market at USD 161.72 billion; Fortune Business Insights at USD 134.46 billion; Grand View Research at USD 135 billion; and Mordor Intelligence at USD 210.11 billion when including the broader pet food and treats category. The market is growing at a CAGR of 5–6.2%, projected to reach USD 191–284 billion by 2031–2034. North America leads with approximately 40–44% of global market share, and Asia-Pacific is the fastest-growing region at approximately 8% CAGR. The United States alone generates approximately USD 43–66 billion in pet food revenue in 2026, making it by far the world’s largest single country market.

What is pet humanisation and how is it driving pet food growth?

Pet humanisation is the progressive cultural and commercial trend through which pet owners increasingly treat their animals as family members with equivalent health, wellness, and nutritional needs to human family members. This shift manifests commercially in the willingness of pet owners to pay premium prices for pet food that reflects their own nutritional values — natural and minimally processed ingredients, high protein content, functional health benefits, life-stage specificity, and sustainable sourcing. Pet humanisation is being driven primarily by millennial and Gen Z pet owners who have adopted pets at extraordinary rates, often as substitutes or supplements for parenthood. Average annual spend per pet is projected to reach USD 1,445 in 2026. The commercial result is a continuous trading-up dynamic across the pet food category, from conventional kibble toward fresh, functional, and personalised premium formats.

What are the key trends in the pet food industry in 2026?

Seven trends are defining the global pet food industry in 2026. First, fresh and human-grade pet food — refrigerated subscription DTC brands like The Farmer’s Dog and Nom Nom are growing at exceptional rates as humanisation drives demand for meals that resemble human food. Second, alternative proteins — insect meal, precision fermentation proteins, and plant-based formulations are entering commercial scale as sustainability concerns and pet owner values drive protein diversification. Third, functional and therapeutic nutrition — treats and diets that deliver specific health outcomes (dental, joint, cognitive, digestive) are growing fast. Fourth, personalised AI-powered nutrition — individual pet health data driving customised diet formulations. Fifth, e-commerce and subscription DTC dominance — online channels growing at 8.35% CAGR as subscription models build exceptional loyalty. Sixth, sustainable packaging — 45% of pet owners prefer sustainable packaging, driving rapid transition away from plastic. Seventh, Asia-Pacific growth — China, India, and Southeast Asia driving the fastest volume expansion globally.

Is raw pet food safe?

Raw pet food — feeding pets uncooked meat, bone, and offal, either in fresh or freeze-dried form — is a controversial topic within the veterinary and pet nutrition communities. Proponents argue that raw feeding is more aligned with the ancestral diet of dogs and cats, delivering benefits including improved coat quality, energy, and digestive health. However, regulatory authorities including the FDA have expressed concerns about raw pet food safety — noting risks of bacterial contamination (Salmonella, Listeria, E. coli) that can affect both pets and the humans handling the food. A voluntary recall of Albright’s raw dog food in 2026 increased regulatory scrutiny of the segment. Pet owners considering raw feeding are advised to consult their veterinarian, handle raw food products with the same hygiene protocols as raw human food, and choose products from manufacturers with transparent safety testing programmes. Commercially produced freeze-dried raw products, where the freeze-drying process reduces pathogen risk while preserving nutritional content, offer a middle ground between the perceived benefits of raw feeding and the safety assurance of conventionally processed food.

What is the difference between dog food and cat food — why are they marketed separately?

Dogs and cats have fundamentally different nutritional requirements that make species-specific formulation essential. Dogs are omnivores — they can thrive on a wide range of animal and plant-based foods and can synthesise certain essential nutrients (including taurine and arachidonic acid) from precursors in their diet. Cats are obligate carnivores — they require pre-formed animal-derived taurine, arachidonic acid, and vitamin A in their diet, as they lack the metabolic enzymes to synthesise these nutrients from plant sources. Feeding a cat dog food long-term can lead to serious deficiencies and health consequences. Additionally, cats and dogs have different protein requirements, different caloric densities needed per body weight, different preferences for moisture content (cats have a lower thirst drive and benefit from wet food for hydration), and different palatability preferences. For these reasons, all reputable pet food manufacturers formulate and market their products specifically for the target species and life stage.

Who are the largest pet food companies in the world in 2026?

Mars Petcare is the world’s largest pet food company with over 16.4% global market share, operating brands including Pedigree, Whiskas, Royal Canin, Sheba, Iams, Eukanuba, Cesar, and Nom Nom. Nestlé Purina is the second-largest, operating Purina ONE, Pro Plan, Felix, Friskies, and Fancy Feast. Hill’s Pet Nutrition — owned by Colgate-Palmolive — leads the veterinary nutrition segment through Science Diet and Prescription Diet. General Mills leads the natural premium segment through Blue Buffalo. J.M. Smucker operates Meow Mix, Milk-Bone, and other mass-market brands. In the emerging DTC fresh pet food segment, The Farmer’s Dog and Ollie are the US market leaders. In Asia, India’s Drools has achieved unicorn status following a Nestlé investment.

What is the outlook for the global pet food market through 2030?

The global pet food market is projected to grow from USD 161.72 billion in 2026 to approximately USD 197–210 billion by 2030, growing at a CAGR of approximately 5–6%. The key dynamics shaping the market through 2030 include: continued premiumisation driven by pet humanisation as millennials and Gen Z age into peak earning years and sustain their pet spending; the commercialisation of alternative proteins at scale as insect meal and precision fermentation protein costs approach parity with conventional animal protein; the consolidation of DTC subscription e-commerce as the dominant channel for premium and fresh pet food; the emergence of Asia-Pacific as the primary volume growth engine as pet ownership expands in China, India, and Southeast Asia; and the increasing integration of veterinary health, nutrition, and insurance into unified pet healthcare platforms led by companies like Chewy and Mars-owned veterinary chains.

Sources and References

- Grand View Research: Pet Food Market Size, Share, Growth Report 2026–2033 — https://www.grandviewresearch.com/industry-analysis/pet-food-industry

- Fortune Business Insights: Pet Food Market Size, Share & Trends Report 2026–2034 — https://www.fortunebusinessinsights.com/industry-reports/pet-food-market-100554

- Straits Research: Pet Food Market Size, Share & Growth 2026–2034 — https://straitsresearch.com/report/pet-food-market

- Mordor Intelligence: Pet Food Market Size, Share & Industry Report 2026–2031 — https://www.mordorintelligence.com/industry-reports/global-pet-food-market-industry

- Global Market Insights: Pet Food and Treats Market Analysis & Growth Outlook 2026–2035 — https://www.gminsights.com/industry-analysis/pet-food-and-treats-market

- Future Market Insights: Pet Food Market Growth & Forecast 2026–2036 — https://www.futuremarketinsights.com/reports/pet-food-market

- Statista: Pet Food Worldwide Market Forecast 2026–2030 — https://www.statista.com/outlook/cmo/pet-animal-supplies/pet-food/worldwide

- Petfood Industry: Global Pet Food Market Projected to Reach USD 247.7B by 2035 — https://www.petfoodindustry.com/pet-food-market/news/15818322/global-pet-food-market-projected-to-reach-2477b-by-2035

- Petfood Industry: Global Pet Food Growth Expected to Continue at Lower Rates — https://www.petfoodindustry.com/blogs-columns/adventures-in-pet-food/blog/15541474/global-pet-food-growth-expected-to-continue-at-lower-rates

- Food Navigator: Pet Food in 2026 — Premiumisation and Humanisation Drives Growth — https://www.foodnavigator.com/Article/2026/01/22/pet-food-market-growth-in-2026/

- IndexBox: Pet Food Market 2026 — USD 161.72bn Value, Growth Drivers & Challenges — https://www.indexbox.io/blog/pet-food-market-hits-16172-billion-fueled-by-humanization-and-premium-demand/

- Stellar MR: Pet Food Market Size, Share & Growth Trends 2026–2032 — https://www.stellarmr.com/report/pet-food-market/2713

- Fortune Business Insights: Dog Food Market Size, Share Report 2026–2034 — https://www.fortunebusinessinsights.com/dog-food-market-115464

- Pet Age: Dog Food Market Premium Nutrition Adoption 2026 — https://www.petage.com/dog-food-market-premium-nutrition-adoption-functional-feeding-trends-pet-humanization/

- CSG Talent: Animal Nutrition Trends 2026 — Innovation, Growth and the Future of Feed — https://www.csgtalent.com/insights/blog/animal-nutrition-market-trends-2026/

- Euromonitor International: Top Five Trends in Pet Care — https://www.euromonitor.com/article/top-five-trends-in-pet-care

- Sustainable Pet Foods (Just Be Kind): Hills, Bond Pet Foods and Precision Fermentation 2026 — https://justbekind.co.uk/blogs/news/exposing-hills-royal-canin-and-nestle-purina