June 9, 2026

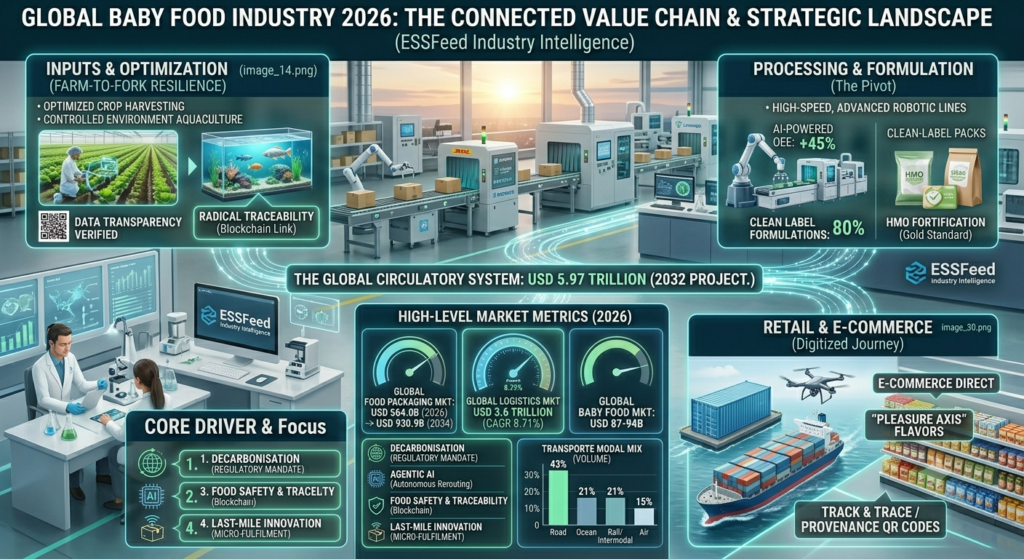

The global baby food industry is valued at approximately USD 87.55–94.29 billion in 2026, growing at a CAGR of 6.02–6.92% and projected to reach USD 139.75–162.82 billion by 2032–2034. The baby food industry occupies a uniquely important position in the global food and beverage value chain. It serves the most vulnerable consumers on earth — infants and toddlers aged 0–36 months — at the most nutritionally critical period of human development. The decisions parents make about what their child eats in the first 1,000 days of life have consequences that extend across an entire lifetime, influencing cognitive development, immune function, metabolic health, and long-term disease risk.

That clinical importance, combined with the structural growth drivers of rising maternal workforce participation, rapid urbanisation, increasing parental health consciousness, and the explosive expansion of middle-class consumer populations across Asia-Pacific and Africa, makes the global baby food industry one of the most consistently growing and commercially resilient segments in the entire food and beverage sector.

Yet in 2026, the global baby food industry is also navigating its most complex operating environment in decades. Heavy metal contamination scandals have shaken consumer trust. Declining birth rates across China, Japan, South Korea, and much of Western Europe are compressing volume in the world’s most mature markets. Regulatory scrutiny of ingredients, marketing practices, and nutritional standards has never been more intense. And a wave of clean-label, organic, and DTC challenger brands is forcing the industry’s multinational incumbents to innovate faster than their R&D cycles have historically required.

This report provides the most comprehensive publicly available analysis of the global baby food industry in 2026 — covering market scale, product category performance, regional dynamics, safety and regulation, ingredient innovation, sustainability, key challenges, strategic outlook, leading companies, FAQ, and full sources. The focus keyword — global baby food industry 2026 — is embedded throughout to support SEO ranking for this pillar post.

Executive Summary: The 2026 Global Baby Food Industry 2026 Landscape

The global baby food industry in 2026 is defined by a “premium safety” imperative. Parents — better informed, more digitally connected, and more health-conscious than any previous generation — are making infant nutrition decisions with a rigour that rivals clinical purchasing. They are reading ingredient labels, cross-referencing independent safety test results, demanding transparency about sourcing and processing methods, and switching brands in response to safety concerns faster than the industry’s traditional reputation management cycles can accommodate.

Key Takeaways for Stakeholders:

The global baby food industry is valued at approximately USD 87–94 billion in 2026, growing at a CAGR of 6–7%, with projections ranging from USD 139–163 billion by 2032–2034 depending on scope of measurement.

Infant formula dominates with 43% market share: The infant milk formula segment is estimated to contribute 43.1% of the market in 2026, driven by the rising number of working mothers, urbanisation, and the growing acceptance of formula as a nutritional supplement or primary feeding option.

Asia-Pacific leads globally: Asia Pacific recorded a market size of USD 74.49–79.52 billion in 2025–2026, capturing approximately 64% of the global baby food market share, driven by the rising women workforce, fast-paced urban lifestyles, and growing awareness of infant nutrition products.

Organic baby food is the fastest-growing sub-segment: The organic baby food market is projected to grow from USD 5.82 billion in 2025 to USD 15.17 billion by 2034, at a CAGR of 11.23%, as parents increasingly treat organic as a default expectation rather than a premium luxury.

Safety is the defining commercial battleground: Research shows that only approximately 20% of baby formulas are free of detectable heavy metals. A study analysing 651 baby food products in the US found approximately 60% failed WHO guidelines — with 44% exceeding sugar recommendations and 70% lacking adequate protein.

HMO fortification is the most significant ingredient innovation: Human milk oligosaccharide (HMO) fortification and novel digital engagement strategies are among the most notable trends in the global baby food market.

Table of Contents

1. Global Baby Food Industry 2026 Overview: Scale, Structure and Growth

Global Valuation and Growth Trajectory

The global baby food industry encompasses a broad range of nutritionally formulated products designed specifically for infants and toddlers aged 0–36 months — including infant formula, prepared purees and ready-to-eat meals, dried and powdered baby cereals, baby snacks, juices and beverages, and growing-up milks for toddlers aged 12–36 months.

The global baby food industry was valued at USD 74.33 billion in 2024 and is projected to rise to USD 103.01 billion by 2031, registering a compound annual growth rate of 4.8% during the forecast period from 2025 to 2031. This growth is fuelled by rising parental awareness of early childhood nutrition, the increasing number of working mothers globally, rapid urbanisation, and strong consumer demand for organic, clean-label, fortified, and convenient infant food products.

Estimates of market size vary across research sources depending on whether the scope includes growing-up milks and toddler nutrition products in addition to core infant formula and baby food categories. The consensus range across major research sources places the 2026 global baby food market at USD 74–94 billion for the core category, growing at a CAGR of 4.8–7% through 2031–2034.

Product Format Mix

By product format, powder accounted for 71.68% of the baby food market in 2025, and ready-to-feed leads growth at a 5.75% CAGR. By age group, infants aged 0–6 months represented 45.25% of 2025 revenue, and the 24–36 months cohort is advancing at a 6.35% CAGR.

The product format landscape reflects the intersection of consumer convenience needs and nutritional requirements across development stages. Powdered formula dominates by volume and value because of its cost efficiency, shelf stability, and ease of transportation — particularly important in emerging markets where cold chain infrastructure may be limited. Ready-to-feed formats command premium pricing due to their sterile preparation and convenience, and are growing fastest as urban, dual-income households prioritise time over cost.

The 24–36 month segment’s strong growth reflects the emerging category of toddler nutrition — “growing-up milks” and stage-3 formulas — which has become an important product innovation and revenue extension strategy for the major manufacturers as birth rate declines pressure the core 0–6 month infant formula market in developed countries.

2. Product Categories: Deep Dives

Infant Formula: The Market’s Dominant Engine

The infant milk formula segment is estimated to contribute 43.1% of the global baby food market share in 2026, driven by the rising number of working mothers globally, urbanisation trends that reduce extended family support for breastfeeding, and the growing acceptance of infant formula as both a primary feeding option and a nutritional supplement.

Infant formula is the most scientifically complex, most heavily regulated, and most commercially significant product category in the baby food industry. Its formulation attempts to approximate the nutritional profile of human breast milk — the biological gold standard for infant nutrition — while meeting the needs of parents who cannot or choose not to breastfeed exclusively.

The infant formula market size was valued at USD 47.2 billion in 2024 and is projected to grow at a CAGR of 10.4% between 2025 and 2034, driven by the rising infant population and women’s employment. Nestlé, with brands like Gerber, NAN, S-26, and Cerelac, is often cited as the largest player with an estimated 10%+ of the global baby formula market by revenue.

The formula market is bifurcating rapidly between standard commodity formula — under regulatory pricing pressure in markets like China — and premium and ultra-premium formulations incorporating HMOs, probiotics, advanced DHA/ARA sources, and next-generation ingredients that command significant price premiums and higher margins.

Organic Baby Food: The Fastest-Growing Sub-Segment

The organic baby food market is projected to grow from USD 5.82 billion in 2025 to USD 15.17 billion by 2034 at a CAGR of 11.23%. This remarkable growth reflects rising global demand for chemical-free, clean-label, and nutritionally superior infant food products. As concerns about food safety, pesticide residues, and artificial additives intensify, organic baby food is rapidly transitioning from a niche premium category to a mainstream essential.

In June 2026, Petite Palates launched savoury, high-protein baby meals designed to support early childhood nutrition, featuring organic ingredients and chef-crafted recipes, catering to evolving parental demand for nutrient-rich options.

The organic baby food category faces a significant credibility challenge despite its growth momentum. Studies, including one from the University of Leeds, reveal that many commercial organic baby foods contain excessive sugar or fall under the “ultra-processed” category, undermining the very principles parents seek. This paradox — organic certification combined with ultra-processing and high sugar content — is creating significant consumer confusion and regulatory pressure for more meaningful transparency standards.

Baby Cereals, Purees and Prepared Foods

Baby cereals and prepared purees represent the traditional core of the baby food category — iron-fortified rice cereals, fruit and vegetable purees, and multi-grain porridges remain volume staples across both developed and emerging markets. However, the category is being transformed by significant format innovation: the shift from jars to pouches has been one of the most commercially impactful packaging changes in the category’s history, enabling on-the-go consumption, reduced packaging waste, and more convenient feeding for time-pressed parents.

Baby Snacks and Finger Foods

The baby snacks segment — rice puffs, organic teething biscuits, fruit strips, and vegetable crisps designed for self-feeding infants from 6 months — is one of the most dynamically growing sub-categories in global baby food. Driven by the baby-led weaning movement, which encourages self-feeding from early stages, and by the demand from older millennial and Gen Z parents for snacking options that support developmental milestones, the category is attracting significant new product launches and DTC brand investment.

3. Key Growth Drivers

Rising Female Workforce Participation

The single most consistent structural driver of baby food market growth globally is the increasing participation of women in the workforce. Breastfeeding requires significant time investment — the WHO recommends exclusive breastfeeding for the first six months of life, followed by continued breastfeeding alongside complementary foods for up to two years — and working mothers in markets without comprehensive paid maternity leave and workplace breastfeeding support face practical barriers to exclusive breastfeeding. The increasing number of working mothers globally is one of the primary drivers of baby food market growth, driving demand for convenient, packaged infant nutrition products that save time in meal preparation.

Urbanisation and Changing Family Structures

Urbanisation is a powerful structural driver of baby food demand in emerging markets. As populations migrate from rural communities — where traditional extended family networks provide childcare support and where home-prepared foods are more accessible — to urban environments characterised by nuclear family structures, time scarcity, and greater access to modern retail, the reliance on packaged baby food increases markedly.

The shift to urbanisation resulting in higher nuclear families and working mothers relying on nutrition products is a major factor driving Asia-Pacific baby food demand. In markets like India, Vietnam, Indonesia, and parts of sub-Saharan Africa, this urbanisation-driven transition from traditional feeding to packaged baby food represents the most significant structural growth opportunity in the global baby food industry.

Parental Health Consciousness and Premium Nutrition

The millennial and Gen Z parents who are now the primary baby food consumers are the most health-informed, most research-oriented, and most willing to pay premium prices for scientifically validated infant nutrition products in the category’s history. They scrutinise ingredient labels, read clinical research on early childhood nutrition, follow paediatricians and infant nutrition experts on social media, and make brand choices based on transparency, clinical validation, and ethical sourcing rather than brand heritage and advertising alone.

The push towards premiumisation is prominent, with firms investing in organic certifications, HMO fortifications, and functional nutrition positioning, all to command higher prices and safeguard market presence.

E-Commerce and DTC Distribution

Retail development is strengthening the market. Supermarkets and pharmacies are expanding baby food shelf space, while online platforms allow parents to schedule repeat purchases, particularly for infant formula. Subscription models are increasingly used for regular consumption products. This shift is expected to accelerate further as internet access and digital payments expand across emerging markets. FTI

The subscription model is particularly powerful in baby food because infant formula and baby food are consumed on a predictable schedule — a parent who subscribes to a monthly formula delivery is converted from a single transactional purchaser to a reliable recurring revenue source for the brand, with significantly higher lifetime customer value and lower churn risk.

4. Innovation: The Science of Better Baby Nutrition

Human Milk Oligosaccharides (HMOs): The Gold Standard Ingredient

Human milk oligosaccharides are complex carbohydrates found in breast milk that serve as prebiotics — feeding the beneficial bacteria in an infant’s developing gut microbiome — and have been shown to play important roles in immune system development, brain development, and protection against infectious disease. HMO fortification is one of the most notable trends in the global baby food market, with companies competing to incorporate these functionally important ingredients into infant formula to narrow the nutritional gap between formula and breast milk.

New rules such as heavy-metal testing disclosures and HMO ingredient approvals are guiding formulations, while 2025 WHO actions on digital promotion push brands toward clinician education and clinical validation. The commercial arms race in HMO fortification is being driven by consumer demand for formulas that more closely approximate breast milk, and by the clinical evidence base supporting HMOs’ health benefits that manufacturers can use in marketing communications.

Danone’s introduction of milk droplet technology in China — replicating the fat globule structure of human breast milk — and Abbott’s FDA-approved hypoallergenic formulas represent the frontier of breast-milk approximation science that is defining the premium formula category.

Probiotics, Prebiotics and the Microbiome

The infant gut microbiome — the complex community of bacteria, viruses, and fungi that colonises a newborn’s digestive system in the first months of life — is increasingly understood as a critical determinant of long-term health outcomes, influencing immune development, metabolic health, and even cognitive function. Baby food manufacturers are investing heavily in probiotic and prebiotic formulations that support optimal microbiome development, and the scientific validation behind these claims is creating a credible functional nutrition narrative that differentiates premium formula from commodity alternatives.

Plant-Based and Alternative Protein Formulas

Nestlé introduced a new plant-based infant formula in select European markets in 2024, expanding its portfolio to meet growing demand for dairy alternatives and allergen-friendly baby nutrition. The plant-based baby formula category is at an early stage of commercial development but growing rapidly as parents of infants with dairy allergies or lactose intolerance seek alternatives, and as the broader plant-based food movement influences purchasing decisions even in the highly conservative baby food category.

The challenge of plant-based infant formula is nutritional completeness — ensuring that a non-dairy formula provides all the essential amino acids, fats, and micronutrients required for infant development without relying on the naturally balanced nutritional profile of cow’s milk. Else Nutrition, Bobbie, Kendamil, and ByHeart are often highlighted for their commitment to clean ingredients and rigorous safety standards, with Little Spoon publishing detailed heavy metal limits and testing results, reporting 2,000+ quality and safety checks per batch.

AI-Powered Nutritional Personalisation

The baby food industry is witnessing increasing adoption of AI-powered customisation, plant-based nutrition, and stage-specific formulations, transforming the market landscape. AI-driven personalisation in baby food is at an early but accelerating stage — platforms that recommend specific formula types, complementary feeding progressions, and developmental nutrition programmes based on an infant’s age, weight, feeding history, and health data are emerging as a new frontier in the category, particularly in markets with advanced digital health infrastructure.

5. Safety and Regulation: The Industry’s Defining Challenge

Heavy Metal Contamination: The Trust Crisis

No issue has more profoundly damaged consumer trust in the commercial baby food industry in recent years than the presence of toxic heavy metals — arsenic, lead, cadmium, and mercury — in commercially packaged products. Research shows that only approximately 20% of baby formulas are free of detectable heavy metals. US Congressional investigations have spotlighted the presence of toxic heavy metals in several branded products, prompting proposed safety regulations. More than 25% of certain baby products were found to contain 100 ppb or more of inorganic arsenic.

Organisations like Consumer Reports and the Clean Label Project regularly test products to check for contaminants. Their findings give parents a clearer picture of what’s inside the can. The democratisation of independent safety testing — and the ability of parents to access and share these results rapidly through social media and parenting communities — has fundamentally altered the risk calculus for baby food manufacturers. A single negative independent test result can cause measurable brand damage within days.

In October 2024, Babylife Organics introduced a range of Regenerative Organic Certified baby foods designed to reduce heavy metal contamination risks, reflecting a growing trend where brands focus not only on organic certification but also enhanced safety standards and sustainability.

WHO Guidelines and Marketing Regulations

The WHO International Code of Marketing of Breast-milk Substitutes — first adopted in 1981 and periodically updated — regulates how infant formula can be marketed globally, prohibiting advertising directly to consumers, restricting promotional activities in healthcare facilities, and requiring that all marketing materials prominently note the superiority of breastfeeding. 2025 WHO actions on digital promotion push brands toward clinician education and clinical validation, reflecting the challenge of applying marketing codes developed for traditional media to digital channels including social media, influencer marketing, and app-based parent communities.

The 60% WHO Compliance Failure

A study by The George Institute analysed 651 baby food products in the US and found approximately 60% failed WHO guidelines — with 44% exceeding sugar recommendations and 70% lacking adequate protein. This finding has significant implications for the industry’s regulatory future. Governments in multiple markets are moving toward mandatory front-of-pack warning labels for baby food products that exceed recommended sugar, salt, or fat levels — regulations that could dramatically reshape product formulations and brand positioning across the category.

US Regulatory Framework

The US Food and Drug Administration regulates baby food and infant formula tightly to guarantee safety and nutritional standards. Manufacturers must adhere to strict standards on ingredient sourcing, levels of contamination, and packaging. Recalls and fears over contaminants have made customers more vigilant, creating challenges for brands in upholding trust and credibility.

The 2022 Abbott Nutrition Similac recall — which triggered a nationwide US infant formula shortage and exposed the fragility of a supply chain dominated by a small number of manufacturers — remains a defining event in the recent history of the baby food industry. Its lessons about supply chain concentration risk, regulatory oversight adequacy, and the speed with which a single manufacturing incident can create a public health crisis have shaped both regulatory action and corporate supply chain strategy.

6. Regional Dynamics

Asia-Pacific: The World’s Baby Food Powerhouse

Asia Pacific recorded a market size of USD 74.49–79.52 billion in 2025–2026, capturing approximately 64% of the global baby food market share.

China is simultaneously the world’s largest and most complex baby food market. The country’s history of domestic formula safety scandals — culminating in the 2008 melamine scandal that killed at least six infants and sickened hundreds of thousands — has created an entrenched preference for imported premium formula among Chinese middle-class parents, who have been willing to pay extraordinary premiums for brands perceived as safe, clean, and scientifically advanced. This dynamic has been the primary growth engine for global premium infant formula brands in China for the past decade.

However, the Chinese market is undergoing significant structural changes in 2026. China’s birth rate dropped to just 6.4 births per 1,000 people in 2023, the lowest in the country’s recorded history, and the resulting decline in the infant population is compressing the volume market for infant formula even as premiumisation drives revenue per unit higher. In early 2026, Nestlé China aligned its infant and Wyeth nutrition businesses to respond to shifting category dynamics.

India represents the most significant emerging growth opportunity in Asia-Pacific baby food. Rising female workforce participation, rapid urbanisation, expanding modern retail infrastructure, and growing parental awareness of infant nutrition are combining to drive sustained, multi-decade demand growth. The transition from traditional home-prepared complementary foods to packaged baby food is still in its early stages in India, creating a vast addressable market.

North America: Premium, Clean-Label, and DTC Growth

North America generated USD 16.49 billion in 2025, contributing 14.24% to global market revenue, projected to grow to USD 17.46 billion in 2026. North America holds the second position in the infant food market, as parents are highly focused on infant nutrition.

North America remains the dominant region in the global infant formula market with an estimated 40.7% share in 2026. The premiumisation trend is prominent with consumers willing to pay higher prices for value-added formulations.

The US market is characterised by the most rapid growth in clean-label, organic, and DTC baby food brands globally. Companies like Bobbie, ByHeart, Kendamil USA, and Little Spoon are capturing significant share among premium-oriented millennial parents who prioritise ingredient transparency, safety certifications, and ethical sourcing — attributes that the legacy multinational brands have been slower to deliver credibly.

Europe: Quality Standards and Regulatory Leadership

Europe leads globally in baby food regulatory standards, ingredient quality requirements, and organic certification infrastructure. European-made formulas — particularly from Germany, the Netherlands, and the UK — command significant premium pricing in global markets including the US and Asia, where parents associate European manufacturing standards with quality and safety.

As a large number of raw material providers for baby food are present in the European region, Europe benefits from strong ingredient supply chain integration. HiPP, Holle, and Lebenswert from Germany and Austria are among the most globally recognised premium organic formula brands.

The European baby food market is facing structural challenges from declining birth rates — the EU’s birth rate has fallen to historic lows in multiple member states — creating a market characterised by volume decline offset by premiumisation in value terms.

Latin America and Middle East & Africa: Emerging Opportunities

Latin America and MEA represent the longest-term structural growth opportunity in global baby food, driven by their relatively young and growing populations, rising urbanisation rates, and expanding middle classes. Brazil, Mexico, Saudi Arabia, the UAE, and Nigeria are the key near-term growth markets. The transition from traditional feeding practices to packaged baby food in these markets will drive sustained demand growth that partially offsets the volume declines in mature Asian and Western markets.

7. Sustainability in Baby Food

Packaging Innovation

The baby food industry faces significant packaging sustainability challenges. Infant formula packaging — typically multi-layer aluminium tins with plastic scoops — generates significant waste. Pouches, while more convenient than jars, raise recyclability challenges. The industry is investing in recyclable and compostable packaging alternatives, including paper-based pouch innovations and refillable tin concepts, but the food safety requirements of infant nutrition create genuine barriers to rapid packaging material transition.

Regenerative Agriculture and Ingredient Sourcing

Babylife Organics introduced a range of Regenerative Organic Certified baby foods designed to reduce heavy metal contamination risks, reflecting a growing trend where brands focus not only on organic certification but also enhanced safety standards and sustainability.

Regenerative organic certification — which goes beyond conventional organic standards to require specific soil health, biodiversity, and farmer welfare practices — is emerging as the next frontier in baby food sustainability credentials. The linkage between soil health practices and reduced heavy metal bioavailability in crops provides a compelling narrative that connects sustainability and safety in a way that resonates powerfully with health-conscious parents.

8. Critical Risks and Challenges

Declining Birth Rates in Key Markets

China’s birth rate dropped to just 6.4 births per 1,000 people in 2023. Consequently, major companies like Nestlé, Danone, Abbott, and local brands like Yili have diversified their products, targeting adult and senior nutrition to sustain business growth. The demographic headwinds facing the baby food industry in its most developed markets — particularly China, Japan, South Korea, Germany, and Italy — are structural, not cyclical. No pricing strategy, marketing investment, or product innovation can generate volume growth in a market where the infant population is shrinking.

The strategic response has been threefold: intensify premiumisation to grow revenue per unit even as volume declines; diversify into adjacent nutritional categories (toddler nutrition, maternal nutrition, adult medical nutrition) that leverage existing brand equity and distribution; and invest in market development in emerging geographies where demographic trends remain favourable.

Safety Scandals and Brand Trust

The baby food industry operates in a uniquely unforgiving commercial environment where a single product safety incident can cause rapid, severe, and potentially irreversible brand damage. The market is highly sensitive to safety scandals and misinformation, making reputation management crucial. Companies differentiate through clinical validation, transparent sourcing, and digital engagement.

The speed with which safety-related information spreads through parenting social media communities and WhatsApp groups means that a negative test result or regulatory action can reach millions of parents within hours — long before a manufacturer’s crisis communication response can be deployed.

Regulatory Intensification

Regulatory frameworks governing baby food ingredients, marketing, labelling, and safety testing are tightening simultaneously across multiple major markets. The EU’s stricter limits on contaminants in baby food, proposed US Congressional legislation on heavy metal testing disclosures, China’s formula registration system requiring independent clinical testing, and the WHO’s updated guidance on digital marketing of breast-milk substitutes collectively represent a significant and growing compliance burden for manufacturers operating across multiple jurisdictions.

The Breastfeeding Paradox

The WHO recommends exclusive breastfeeding for the first six months of life as the optimal feeding strategy for most infants, creating a structural tension at the heart of the commercial baby food market. Brands that market infant formula aggressively risk regulatory sanction and consumer backlash; brands that undermarket their products risk losing market share to competitors. Managing the commercial imperative of brand growth against the public health imperative of breastfeeding promotion is one of the most complex and sensitive strategic challenges in the food industry.

9. Strategic Outlook for Stakeholders

Actionable Recommendations

Make Safety Transparency Your Primary Commercial Strategy: In a market where 80% of formulas contain detectable heavy metals and 60% of baby food products fail WHO guidelines, voluntary safety transparency — publishing independent test results, heavy metal limits, and quality assurance protocols — is the most powerful commercial differentiator available. The brands demonstrating the strongest growth in 2026 are those who have made radical ingredient transparency a core brand value, not a regulatory compliance minimum.

Invest Aggressively in Emerging Market Development Now: The demographic tailwinds in India, Southeast Asia, Sub-Saharan Africa, and Latin America represent the most significant long-term structural opportunity in global baby food. Building distribution infrastructure, clinical education networks for healthcare providers, and locally relevant product formulations in these markets now will create competitive advantages that compound over decades as these markets develop.

Innovate in Functional Ingredients to Defend Premium Margins: HMO fortification, advanced probiotic strains, breast-milk-fat-structure replication, and personalised nutrition platforms are the ingredients of premium formula differentiation. The R&D investment required to substantiate these functional claims is significant, but the margin differential between commodity and premium formula justifies it — premium formula can command prices 3–5× higher than standard formula in markets where safety and nutrition credentials are credible.

Build DTC Capability as a Strategic Complement to Retail: The DTC baby food brands that are capturing disproportionate share among premium consumers — Bobbie, ByHeart, Little Spoon, and their global equivalents — are doing so by combining subscription convenience, radical transparency, and community building in ways that traditional retail cannot replicate. Even large multinational brands can benefit from DTC capability as a first-party data acquisition and consumer relationship building tool.

Strategic Summary: The 2026 Baby Food Business Model

| Strategic Priority | Traditional Approach | 2026 Competitive Standard |

|---|---|---|

| Safety | Regulatory compliance minimum | Radical transparency and voluntary disclosure |

| Innovation | Formula improvement cycles | HMO, probiotic, personalised nutrition |

| Distribution | Retail and pharmacy dominance | Omnichannel including DTC subscription |

| Growth Markets | China and developed West | India, SE Asia, Africa, Latin America |

| Brand Differentiation | Heritage and advertising | Clinical validation and ingredient transparency |

| Sustainability | ESG reporting | Regenerative sourcing and safe ingredient supply |

10. Leading Industry Companies

| Company | Region | Strategic Focus |

|---|---|---|

| Nestlé S.A. | Switzerland/Global | Largest global baby food company, focusing on higher-priced products including Sinergity, NAN, and Illuma, targeting 2–3% CAGR in its nutrition division. In early 2026, aligned infant and Wyeth nutrition businesses in China to respond to shifting dynamics. Supply Chain Digital Brands include Gerber, Cerelac, NAN, S-26. |

| Danone S.A. | France/Global | Introduced infant formula containing milk droplets that closely mimic the structure of mother’s milk. Opened a new infant formula production facility in Normandy to support export growth to Asia and the Middle East. Sustainability Magazine Brands include Aptamil, Nutrilon, Cow & Gate, Karicare. |

| Abbott Laboratories | USA/Global | Received FDA approval for its new hypoallergenic infant formula designed for infants with severe allergies, marking a significant addition to its Similac product line. Sustainability Magazine Brands include Similac and Eleva. |

| Reckitt Benckiser (Mead Johnson) | UK/Global | Identified Mead Johnson Nutrition as non-core in 2025 while committing to preserve the Enfamil brand’s clinical and professional equity. Supply Chain Digital Enfamil is the market leader in North America. |

| China Feihe | China | China’s leading domestic infant formula brand, capitalising on post-2008 domestic safety reforms and “national brand” positioning in the Chinese market. |

| HiPP GmbH & Co. | Germany | Europe’s leading organic infant formula and baby food brand. Premium, biodynamic credentials widely respected across European and global premium markets. |

| Bobbie | USA | The leading US clean-label, premium DTC baby formula brand. USDA Organic certified, transparent heavy metal testing, and subscription-first business model. |

| Kendamil | UK/Global | Highlighted for commitment to clean ingredients and rigorous safety standards. Maersk Made in the UK from whole milk, without palm oil. Strong premium positioning globally. |

| ByHeart | USA | US-made, whole milk-based formula with HMO fortification. Positioned as the first new US formula manufacturer in decades, built around clinical validation and ingredient integrity. |

| Little Spoon | USA | Leading US DTC fresh baby food platform. Publishes detailed heavy metal limits and testing results, reports 2,000+ quality and safety checks per batch. Maersk |

Related: As the processed food industry grapples with stricter clean-label regulations and a massive pivot toward nutrient-dense convenience, the landscape for manufacturers is rapidly evolving. We dive into the critical production, regulatory, and market trends defining the year in our Global Processed Food Industry Report 2026.

Frequently Asked Questions (FAQ)

What is the global baby food market size in 2026?

The global baby food industry market size in 2026 is estimated at approximately USD 74–94 billion, with estimates varying depending on whether the scope includes growing-up milks and toddler nutrition products alongside core infant formula and baby food. The most frequently cited figures from major research organisations range from USD 74.57 billion (Mordor Intelligence) to USD 94.29 billion (360iResearch). The market is projected to grow at a CAGR of 4.8–7% through 2031–2034, reaching USD 103–163 billion depending on the research scope. Growth is driven by rising maternal workforce participation, urbanisation in emerging markets, parental health consciousness, and ingredient innovation including HMO fortification and organic formulations.

What are the biggest trends in the baby food industry in 2026?

Six trends are defining the global baby food industry in 2026. First, safety transparency — in response to heavy metal contamination scandals, brands are competing on voluntary disclosure of independent test results and contaminant limits as a primary commercial differentiator. Second, HMO fortification — human milk oligosaccharides are the most significant ingredient innovation in the category, added to premium formulas to replicate the gut health and immune benefits of breast milk. Third, organic and clean-label mainstreaming — the organic baby food market is growing at 11.23% CAGR, transitioning from niche premium to mainstream expectation. Fourth, DTC subscription models — brands like Bobbie, ByHeart, and Little Spoon are capturing premium consumers through subscription-first digital channels. Fifth, emerging market expansion — India, Southeast Asia, and Africa are replacing China as the primary volume growth engines as Chinese birth rates decline. Sixth, AI-powered personalisation — platforms recommending personalised feeding programmes based on infant developmental data are emerging as a new frontier.

Is baby formula safe? What are heavy metals in baby food?

Heavy metals — including lead, arsenic, cadmium, and mercury — are naturally occurring elements found in soil and water that can be absorbed by agricultural crops used as ingredients in baby food and infant formula. Research shows that only approximately 20% of commercially available baby formulas are completely free of detectable heavy metals. However, it is important to note that the presence of trace heavy metals does not automatically mean a product is unsafe — regulatory bodies including the FDA and EFSA set maximum limits for heavy metal content in baby food, and products meeting these limits are considered safe for infant consumption. Parents concerned about heavy metal exposure should look for brands that voluntarily publish independent third-party test results, use ingredients sourced from low-contamination agricultural environments, and hold Regenerative Organic Certification, which has been associated with reduced heavy metal bioavailability.

Which region leads the global baby food market?

Asia-Pacific leads the global baby food market with approximately 64% of total market share, primarily driven by China, India, Japan, and Southeast Asia. China is the single largest country market, accounting for a major portion of the global infant formula market, though its declining birth rate is creating structural volume headwinds that are pushing manufacturers toward premiumisation and geographic diversification. India is the fastest-growing major baby food market — with 1.4 billion people, rising female workforce participation, and organised retail infrastructure still in early development, India is on a trajectory to become the world’s second-largest baby food market before 2030. North America holds the second-largest regional share at approximately 14%, and is the leading market for premium formula innovation, DTC brands, and clean-label baby food.

What is HMO in baby formula and why does it matter?

Human milk oligosaccharides (HMOs) are complex carbohydrates — prebiotics — naturally present in breast milk that serve critical functions in infant development. They feed beneficial gut bacteria, support the development of the infant’s immune system, may protect against respiratory and gastrointestinal infections, and have been associated with positive neurodevelopmental outcomes. HMOs are absent from or present in very low concentrations in conventional cow’s milk, making their addition to infant formula a significant nutritional advancement toward replicating breast milk. In 2026, HMO fortification is one of the most commercially significant ingredients in premium infant formula, with both 2′-FL (the most abundant HMO in human milk) and more complex multi-HMO blends now commercially available at scale. Brands including Nestlé, Danone, and Similac have incorporated HMOs into their premium formula lines, and clinical evidence supporting HMOs’ health benefits continues to strengthen.

What is the difference between standard, premium, and ultra-premium baby formula?

Baby formula is increasingly marketed in distinct tiers that reflect differences in ingredient quality, functional fortification, and manufacturing standards. Standard formula meets the minimum regulatory nutritional requirements for infant formula and is produced from commodity dairy ingredients. Premium formula typically incorporates additional functional ingredients such as DHA/ARA fatty acids, standard probiotic strains, and basic prebiotic fibres, commanding price premiums of 30–60% above standard. Ultra-premium formula — the fastest-growing tier in developed markets — incorporates HMOs, advanced probiotic strains, breast-milk-fat-structure replication technology, organic certified ingredients, and comprehensive third-party safety testing, commanding prices 2–5× above standard formula. For parents, the decision between tiers involves balancing evidence-based functional benefits, safety credentials, affordability, and the recommendations of their paediatrician.

Who are the leading baby food companies globally in 2026?

The global baby food market is moderately consolidated at the top, with four multinational companies — Nestlé (brands: Gerber, NAN, S-26, Cerelac), Danone (Aptamil, Nutrilon, Cow & Gate), Abbott (Similac, Eleva), and Reckitt Benckiser/Mead Johnson (Enfamil) — collectively accounting for a significant share of global infant formula revenue. Nestlé is the largest, with an estimated 10%+ of the global baby formula market by revenue. In China, domestic brands like China Feihe, Yili, and Junlebao have gained significant market share following domestic formula safety reforms. Among premium and organic specialists, Germany’s HiPP, UK-based Kendamil, and US DTC brands Bobbie and ByHeart are the most commercially significant challengers. The DTC segment is the fastest-growing competitive frontier, with brands that combine subscription convenience, radical transparency, and clean-label credentials capturing disproportionate share among premium millennial parents.

What is the outlook for the global baby food market through 2030?

The global baby food market is projected to reach USD 103–163 billion by 2031–2034, growing at a CAGR of 4.8–7% depending on the research scope. The key dynamics shaping the market through 2030 include: continued volume growth driven by emerging markets — particularly India, Southeast Asia, and Sub-Saharan Africa — offsetting volume declines in developed markets with falling birth rates; accelerating premiumisation as HMO fortification, functional nutrition credentials, and clean-label safety standards become mainstream expectations rather than premium differentiators; the maturing of the DTC subscription channel as a structural distribution model for baby food, particularly in North America and Europe; intensifying regulatory scrutiny of heavy metal contamination, sugar content, and marketing practices across all major markets; and the likely entry of AI-powered personalised nutrition platforms that will create entirely new product and service categories within the broader infant nutrition market.

Sources and References

- Market Data Forecast: Global Baby Food Market Size, Share, Trends & Growth Forecast 2026–2034 — https://www.marketdataforecast.com/market-reports/baby-food-market

- Mordor Intelligence: Baby Food Market Size, Trends & Industry Analysis 2026–2031 — https://www.mordorintelligence.com/industry-reports/baby-food-market

- Mordor Intelligence: Infant Nutrition Market Analysis 2026–2031 — https://www.mordorintelligence.com/industry-reports/infant-nutrition-market

- Precedence Research: Baby Food Market Size and Trends 2026–2035 — https://www.precedenceresearch.com/baby-food-market

- Coherent Market Insights: Baby Food Market Size, Share and Opportunities 2026–2033 — https://www.coherentmarketinsights.com/market-insight/baby-food-market-1043

- Coherent Market Insights: Organic Baby Food Market Size & Share 2026–2033 — https://www.coherentmarketinsights.com/market-insight/organic-baby-food-market-557

- Coherent Market Insights: Infant Formula Market Size & Share 2026–2033 — https://www.coherentmarketinsights.com/market-insight/infant-formula-market-2330

- PR Newswire / Maximize Market Research: Baby Food Market to Reach USD 162.82 Billion by 2032 — https://www.prnewswire.com/news-releases/baby-food-market-to-reach-usd-162-82-billion-by-2032–expanding-at-6-7-cagr-says-maximize-market-research-302692765.html

- Straits Research: Baby Food Market Size, Share and Growth 2026–2034 — https://straitsresearch.com/report/baby-food-market

- 360iResearch: Baby Food Market Size & Share 2026–2032 — https://www.360iresearch.com/library/intelligence/baby-food

- Globe Newswire / The Insight Partners: Baby Food Market to Surpass US$103.01 Billion by 2031 — https://www.globenewswire.com/news-release/2026/05/14/3294690/0/en/Baby-Food-Market-to-Surpass-US-103-01-Billion-by-2031-Global-Industry-Research-by-The-Insight-Partners.html

- Fortune Business Insights: Baby Food Market Size, Share & Trends Report 2026–2034 — https://www.fortunebusinessinsights.com/baby-food-market-103849

- Market Research Future: Baby Food and Infant Formula Market Size & Forecast 2035 — https://www.marketresearchfuture.com/reports/baby-food-infant-formula-market-1349

- Market.us: Baby Food and Infant Formula Market Size, Share & Growth Analysis 2025–2034 — https://market.us/report/baby-food-and-infant-formula-market/

- Allied Market Research: Asia-Pacific Baby Infant Formula Market 2026 — https://www.alliedmarketresearch.com/asia-pacific-baby-infant-formula-market

- Grand View Research / GMI: Infant Formula Market Size & Share Growth Analysis 2025–2034 — https://www.gminsights.com/industry-analysis/infant-formula-market

- Renub Research / Vocal: Organic Baby Food Market Size and Forecast 2026–2034 — https://vocal.media/trader/organic-baby-food-market-size-and-forecast-2026-2034

- Renub Research: United States Baby Food and Infant Formula Market Trends 2025–2033 — https://www.renub.com/united-states-baby-food-infant-formula-market-p.php

- IMARC Group: Baby Food and Infant Formula Market Size, Share & Forecast — https://www.imarcgroup.com/baby-food-infant-formula-market

- Else Nutrition: 10 of the Cleanest Baby Formulas for 2026 — https://elsenutrition.com/blogs/news/cleanest-baby-formula-list

- Mommyhood101: Best Organic Baby Formulas 2026 — https://mommyhood101.com/best-organic-baby-formula