Weather Update: The prevailing weather conditions remain uneventful within the market context. Discussions about the persistent cold in Russia will eventually give way to more mundane topics such as rainfall. In Australia, rainfall patterns have shifted towards the coast, indicating significant precipitation in the rear, while the focus now turns to the eastern regions, with hopes that this moisture will reach further inland.

Market Trends: The ongoing decline in market prices continues, and it appears that the risk premiums previously factored in are no longer warranted. This sentiment may be slightly premature as we approach the last quarter of the financial year.

Australian Market Outlook: The old crop market has demonstrated robust support but is now confronted with the pivotal question: what impact would two inches of rainfall across the eastern coast have on market valuations? The broader Australian landscape, however, appears to be lacking in moisture for the next fortnight according to the Global Forecast System (GFS) projections.

Offshore Market Insights

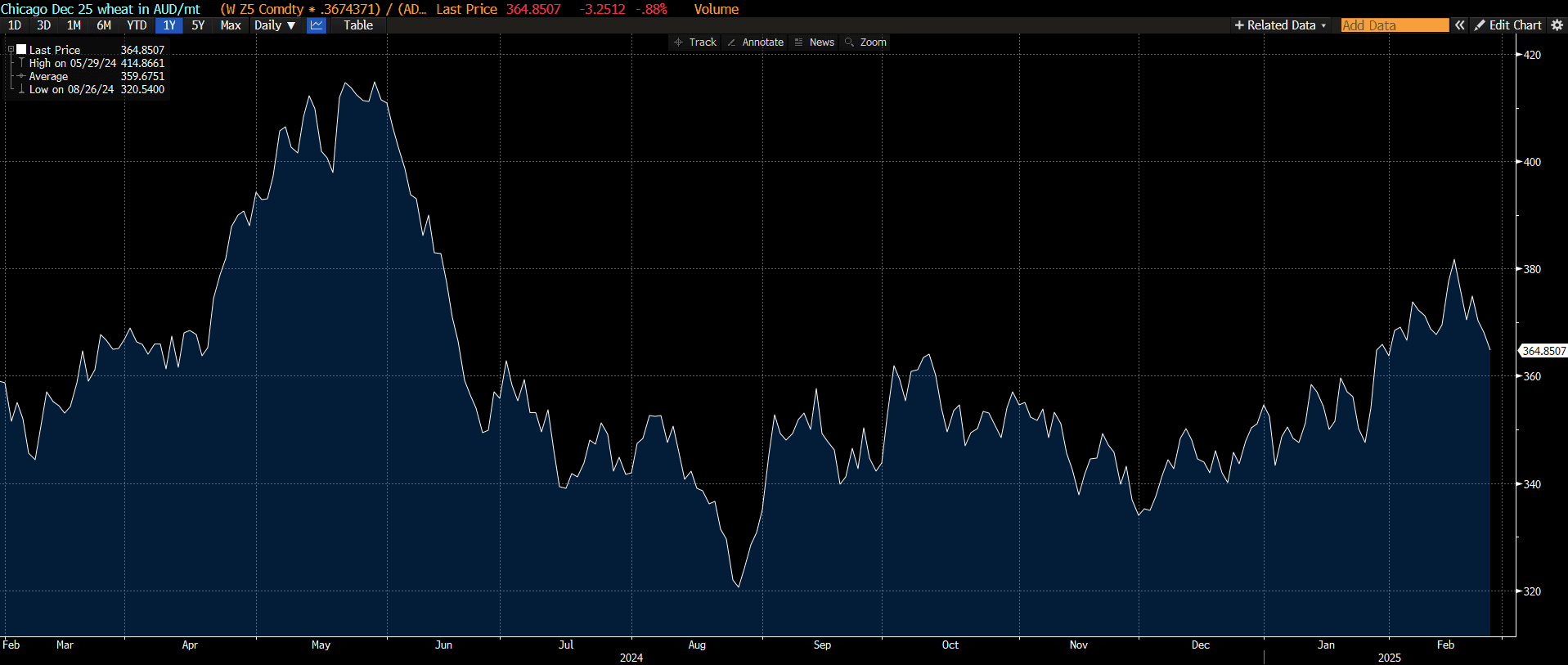

Price trends for the December 25 futures contract of Chicago SRW wheat over the past year, expressed in Australian dollars per tonne. Source: Bloomberg and Lachstock Consulting. Click to expand.

Tariff uncertainties continue to create volatility in the market, particularly following comments from President Trump regarding the potential delay of tariffs on Mexico and Canada. His contradictory statements have left market participants in a state of confusion. Personally, I remain cautiously optimistic about the prospects of avoiding tariffs for Canada, although my confidence is waning.

In the Black Sea region, wheat values in Romania remain stable, despite the downward pressure from U.S. futures markets. Limited Russian exports are alleviating some of the market tensions, although demand does not seem to be excessively aggressive at this stage, indicating a relatively balanced market situation.

Recent reports indicate a decline in Oklahoma wheat conditions from 40% rated good-to-excellent in January to just 33% as of the week ending February 23rd. Topsoil moisture levels are concerning, with 39% classified as short to very short compared to only 17% last year. Further reports from Kansas and Texas are expected next week.

In global markets, U.S. corn appears to be in a favorable position, outpricing South American competitors. Argentina is anticipating substantial rainfall, which could potentially lead to flooding, reinforcing the notion that “rain means grain.” Meanwhile, Brazilian soybean conditions are promising, with nearly 40% already harvested.

In other news, Qantas Airways has announced its first dividend payment in six years, highlighting a potential recovery in its financial health. However, there may be room for improvement in customer service, particularly regarding their help line response times.

Domestic Market Overview

In yesterday’s trading, canola bids in Western Australia saw a slight increase to around A$860 Free In Store (FIS), while wheat prices firmed to A$376, and barley remained unchanged at A$348. New crop canola bids also reflected strength, reaching A$810, with genetically modified (GM) canola at A$745, and wheat at A$392.

On the eastern front, canola bids improved to A$783, with GM canola at A$670. Wheat prices remained steady around A$347, and barley was priced at A$318. New crop canola bids in this region are currently around A$772, with GM bids at A$685 and wheat at A$368.

Despite recent downward trends in global prices, domestic grain markets in Australia have maintained stability, underscoring the country’s competitive edge in Asian markets coupled with strong domestic demand, particularly along the eastern coast. This dynamic could lead to upward price adjustments in the near future.

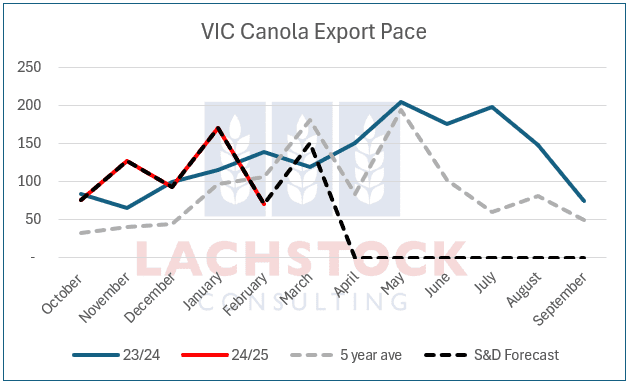

As the March tariff deadline approaches, domestic canola markets have remained resilient, defying global losses. The local balance sheet is tight, with a significant portion of this year’s production already sold and the export program well underway across most states.

Monthly canola exports from Victoria (thousand tonnes). The pace in 2024-25 (indicated by red and black dotted lines) surpasses both the previous year (blue line) and the five-year average (grey dotted line). Source: Lachstock. Click to expand.

“`

This revision maintains the essential details while presenting the information in a professional tone and structure, ensuring clarity and coherence throughout the text.

Related Analysis: View Previous Industry Report