Rapidly falling pork prices in China raise concerns of deflation risk, as major hog farmers flood the market. Discover the economic implications and strategies amid this price drop.

Pork Price Plunge Threatens China with Deflation Crisis

Falling pork prices could potentially push China back into a deflationary situation in the near future. This is because major hog farming companies in the country are flooding the domestic market with their products, complicating Beijing’s efforts to boost confidence in the second-largest economy globally.

Live hog futures on China’s Dalian Commodity Exchange have seen a significant 15% decline since the beginning of October, reflecting a sharp downturn in expectations for pork prices nationwide. Wholesale pork prices in China have dropped by over 40% compared to the same period last year.

Economists are predicting that the declining cost of pork, which holds substantial weight in China’s official consumer price index, will likely lead to deflation when October’s data is released this Thursday.

Julian Evans-Pritchard, a senior China economist at Capital Economics, commented, “It appears that consumer inflation will turn negative again in October, mainly due to a decline in food inflation caused by the fall in pork prices.”

A return to deflation, following weak growth in August and a flat CPI reading in September, could undermine the Chinese government’s efforts to restore confidence in the country’s fragile economy. This fragility is attributed to weak consumer confidence and a liquidity crisis in China’s property sector.

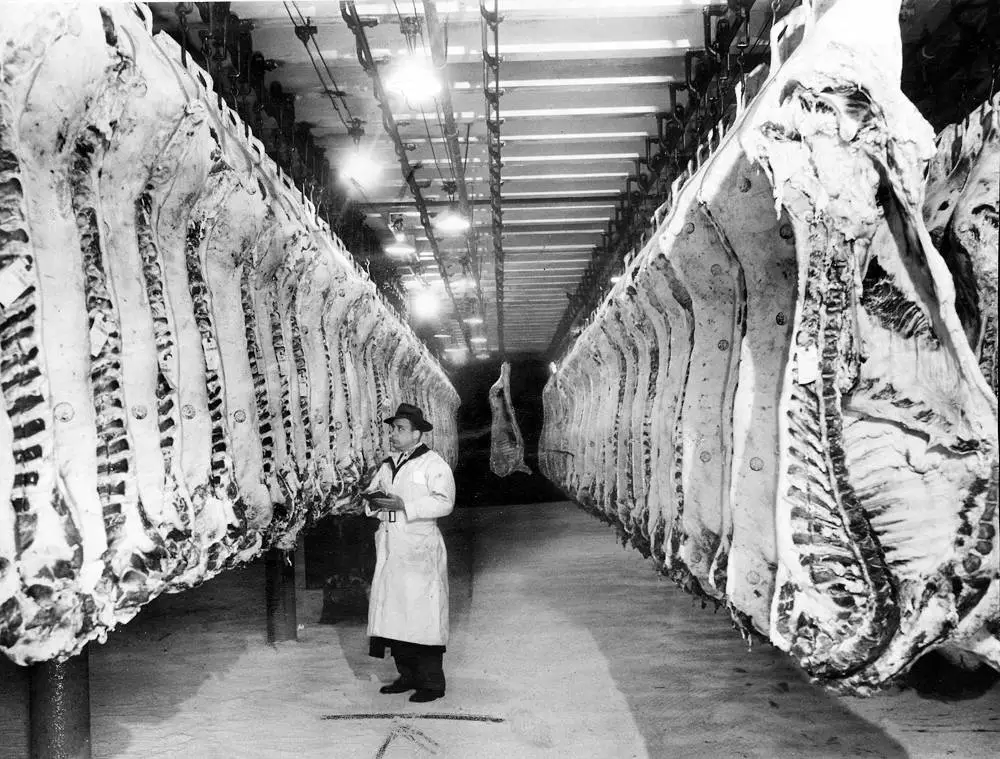

The price of pork in China, the world’s largest producer and consumer of pork, has historically followed a boom-and-bust cycle as small-scale farmers enter the market in response to rising demand, leading to oversupply and sharp price drops. Beijing has attempted to gain more control over this cycle by consolidating production among a few large-scale farming companies. However, this year, these same companies have contributed to the price decline.

Pork prices started to rebound in July, partially due to government-led purchases, but then fell again as major listed hog farmers, including Muyuan and New Hope, chose not to reduce production despite weaker demand. Typically, larger producers cut output by selling breeding sows and purchasing fewer piglets to raise until prices recover. However, Chinese piglet prices have only fallen by 10% compared to the previous year, indicating relatively strong demand for young pigs despite the significant drop in pork prices.

Analysts suggest that this strategy paid off last year when a fourth-quarter recovery in pork prices, coinciding with the easing of China’s strict COVID-19 restrictions, allowed top producers to increase revenues at the expense of smaller farmers who were forced out of the market.

Darin Friedrichs, director of market research at Sitonia Consulting in Shanghai, noted that major Chinese pork producers are following a similar strategy this year, but there are no signs of an imminent fourth-quarter rebound in demand. Some pork producers are even selling subsidiaries or having executives buy back stock, indicating increased financial pressure on them.

Muyuan, the world’s largest hog farmer, has seen its stock decline by more than 20% this year, even after announcing a share buyback worth approximately Rmb1bn ($137 million) last month. The company recently canceled a planned share sale in Zurich, citing “objective factors” in a filing to Shenzhen’s stock exchange.

Friedrichs added, “Part of the problem is that many of these major companies have, to some extent, accepted the boom-and-bust cycle and believe they are better at managing it than their competitors.”